Concept explainers

Videos

Problem 23-3B

Flexible budget preparation; computation of materials, labor, and

P1P2P3

Suncoast Company set the following standard costs for one unit of its product.

Direct materials (6 lbs. @ $5 per lb.) …………………. $ 27

Direct labor (2 hrs. @ $17 per hr.) ……………………... 18

Overhead (2 hrs. @ $ 18.50 per hr.) ……………………. 24

Total

The predetermined overhead rate ($ 16.00 per direct labor hour) is based on an expected volume of 75% of the factory’s capacity of 20,000 units per month. Following are the company’s budgeted overhead costs per month at the 75% capacity level.

Overhead Budget (75% Capacity)

Variable overhead costs

Indirect materials ……………………………………… $ 22,000

Indirect labor …………………………………………… 90,000

Power …………………………………………………… 22,500

Repairs and maintenance ……………………………….. 45,000

Total variable overhead costs …………………………… $180,000

Fixed overhead costs

Depreciation- Machinery ………………………………… 72,000

Taxes and insurance ……………………………………… 18,000

Supervision ………………………………………………... 66,000

Total fixed overhead costs …………………………………180,000

Total overhead costs ………………………………………………$ 360,000

The company incurred the following actual costs when it operated at 75% of capacity in October.

Direct materials (91,000 lbs. @ $5.10 per lb) …………………… $ 420,900

Direct labor (30,500 hrs. @ $ 17.25 per hr.) ……………………… 280,440

Overhead costs

Indirect materials …………………………………………. $ 21,600

Indirect labor ………………………………………………. 82,260

Power ………………………………………………………. 23,100

Repairs and maintenance …………………………………… 46,800

Depreciation-Building ……………………………………… 24,000

Depreciation-Machinery …………………………………….. 75,000

Taxes and insurance …………………………………………. 16,500

Supervision …………………………………………………… 66,000

355,260

Total costs ……………………………………………………………_____

$1,056,600 _______

Required

- Examine the monthly overhead budget to (a) determine the costs per unit for each variable overhead item and its total per unit costs and (b) identity the total fixed costs per month.

- Prepare flexible overhead budgets (as in Exhibit 23.12) for October showing the amounts of each variable and fixed cost at the 65%, 75%, and 85% capacity levels.

- Compute the direct materials cost variance, including its price and quantity variances.

- Compute the direct labor cost variance, including its rate and efficiency variances.

- Prepare a detailed overhead variance report (as in Exhibit 23.16) that shows the variances for individual items of overhead.

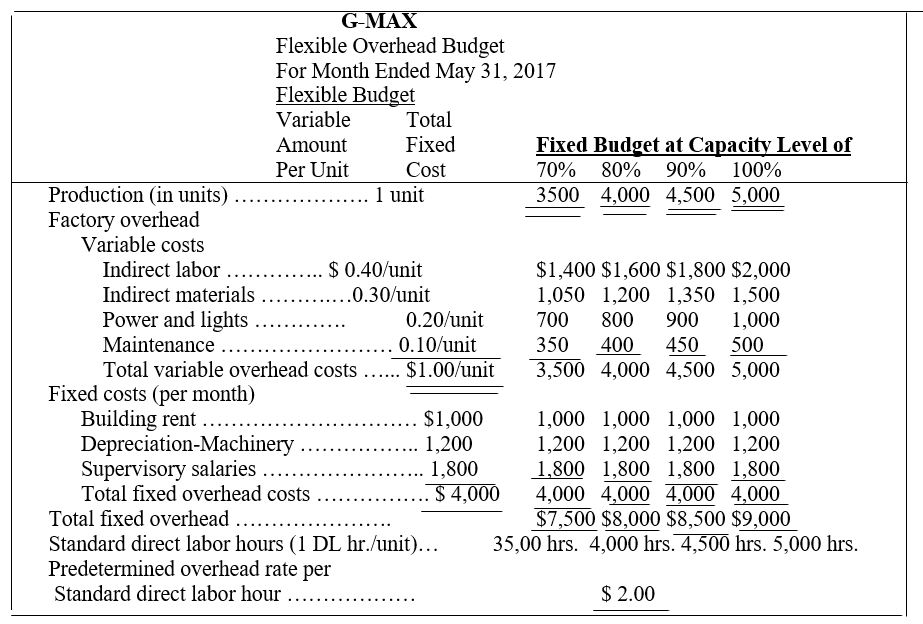

EXHIBIT 23.12 Flexible Overhead Budgets

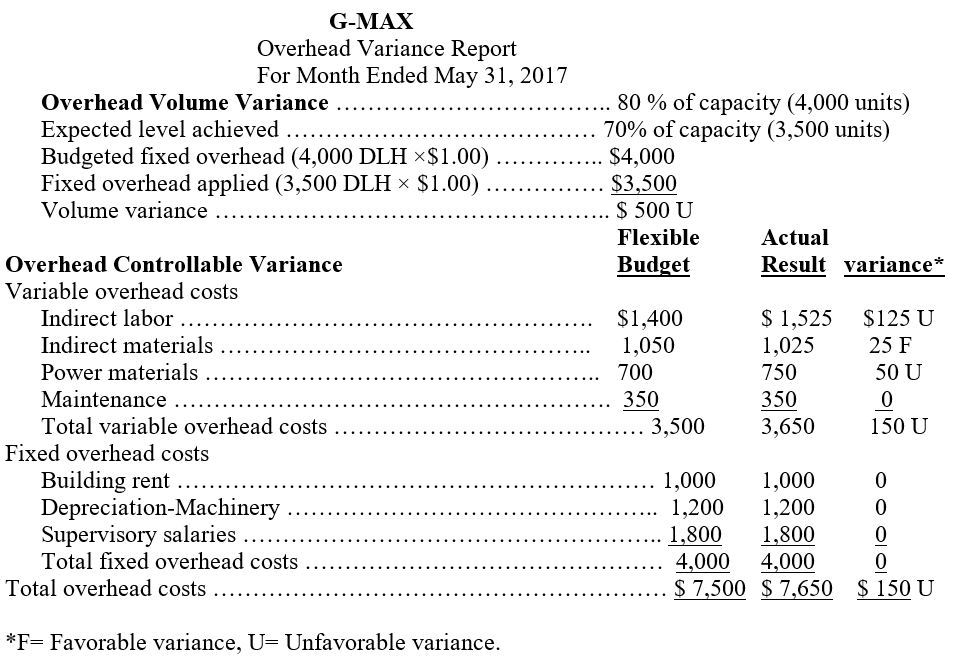

EXHIBIT 23.16 Overhead Variance Report

Flexible Budget:

A flexible budget is prepared for more than one level of production and it is flexible in nature. Flexible budget can vary according to the actual level of production. It eliminates the volume variance between the budgeted values and actual result of production.

Material Price Variance:

At the actual quantity, the difference between the actual cost and standard cost is known as material price variance.

Material Quantity Variance:

The material quantity variance measures the efficiency of a production in terms of material utilization. It is computed by determining the difference between the standard quantity to used and actual quantity of material used in the production at the standard rate.

Labor Rate Variance:

At the actual direct labor hours, the variance between the actual direct labor cost based on actual rate incurred and the budgeted direct labor cost based on standard rate is called direct labor cost variance.

Direct Labor Efficiency Variance:

Direct labor efficiency variance measures the efficiency in utilization of direct labor costs by determining the difference between the actual labor hours and the direct labor hours allowed at the standard rate.

To determine:

1. Determine the cost per unit of each variable overhead item and its total per unit costs and identify the total fixed costs per month.

2. Preparing flexible budgets showing the amounts of each variable and fixed cost at the 65%, 75% and 85% capacity levels.

3. Computation of direct materials cost variance, showing price and quantity variances.

4. Computation of direct labor cost variance, showing rate and efficiency variances.

5. Preparation of overhead variance report that shows the variances for individual items of overhead.

Explanation of Solution

Explanation:

1. The total per unit costs is $12 and the total fixed cost per month is $180,000.

2. The total overhead cost at 65%, 75%, and 85% is $336,000, $360,000, and $384,000 respectively.

3. The direct material cost variance is $15,900 (U) with unfavorable price variance of $6,900 and quantity variance of $9,000.

4. Direct labor cost variance is $10,440 (U) with unfavorable rate variance of $6,840 and efficiency variance of $3,600.

5. Suncoast Company has favorable overhead volume variance of $48,000 and unfavorable controllable variance of $4,740.

1.

| Overhead items | Variable cost per unit | Fixed cost per month |

| Variable overhead costs | ||

| Indirect materials | $1.50 | |

| Indirect labor | $6.00 | |

| Power | $1.50 | |

| Repairs and maintenance | $3.00 | |

| Total variable overhead costs | $12.00 | |

| Fixed overhead costs | ||

| Depreciation – Building | $24,000 | |

| Depreciation – Machinery | $72,000 | |

| Taxes and insurance | $18,000 | |

| Supervision | $66,000 | |

| Total fixed overhead costs | $180,000 |

2.

| SUNCOAST COMPANY Flexible Overhead Budgets For the Month Ended December 31. |

|||||

| Flexible Budget | Flexible Budget at Capacity Level of | ||||

| Variable cost per unit | Fixed cost per month | 65% | 75% | 85% | |

| Production (in units) | 1 unit | 13,000 | 15,000 | 17,000 | |

| Variable overhead costs | |||||

| Indirect materials | $1.50 | $19,500 | $22,500 | $25,500 | |

| Indirect labor | $6.00 | $78,000 | $90,000 | $102,000 | |

| Power | $1.50 | $19,500 | $22,500 | $25,500 | |

| Repairs and maintenance | $3.00 | $39,000 | $45,000 | $51,000 | |

| Total variable overhead costs | $12.00 | $156,000 | $180,000 | $204,000 | |

| Fixed overhead costs | |||||

| Depreciation – Building | $24,000 | $24,000 | $24,000 | $24,000 | |

| Depreciation – Machinery | $72,000 | $72,000 | $72,000 | $72,000 | |

| Taxes and insurance | $18,000 | $18,000 | $18,000 | $18,000 | |

| Supervision | $66,000 | $66,000 | $66,000 | $66,000 | |

| Total fixed overhead costs | $180,000 | $180,000 | $180,000 | $180,000 | |

| Total Overhead Costs | $336,000 | $360,000 | $384,000 | ||

| Predetermined overhead rate per standard direct labor hour | $16.00 | ||||

3.

Computation of direct materials cost variance, including its price and quantity variances

4.

Computation of direct labor cost variance, including its rate and efficiency variances

5.

| SUNCOAST COMPANY Overhead Variance Report For the Month Ended December 31. |

||||

| Overhead Volume Variance | ||||

| Expected production level | 75% of capacity 15,000 units | |||

| Production level achieved | 85% of capacity 17,000 units | |||

| Budgeted fixed overhead (22,500 hrs. X $16.00) | $360,000 | |||

| Fixed overhead applied (25,500 hrs. X $16.00) | $408,000 | |||

| Volume Variance | $48,000 F | |||

| Overhead Controllable Variance | Flexible Budget | Actual Results |

Variances | |

| Variable overhead costs | ||||

| Indirect materials | $22,500 | $21,600 | $900 F | |

| Indirect labor | $90,000 | $82,260 | $7,740 F | |

| Power | $22,500 | $23,100 | $600 U | |

| Repairs and maintenance | $45,000 | $46,800 | $1,800 U | |

| Total variable overhead costs | $180,000 | $173,760 | $6,240 F | |

| Fixed overhead costs | ||||

| Depreciation – Building | $24,000 | $24,000 | 0 | |

| Depreciation – Machinery | $72,000 | $75,000 | $3,000 U | |

| Taxes and insurance | $18,000 | $16,500 | $1,500 F | |

| Supervision | $66,000 | $66,000 | 0 | |

| Total fixed overhead costs | $180,000 | $181,500 | $1,500 U | |

| Total Overhead costs | $360,000 | $355,260 | $4,740 U | |

Conclusion:

The direct material pro=ice variance is $6,900 Unfavorable

The direct material quantity variance is $9,000 Unfavorable

The direct material cost variance is $15,900 Unfavorable

Want to see more full solutions like this?

Chapter 23 Solutions

Fundamental Accounting Principles

- Variance Problem Standard Quantity Standard Cost Standard price $1.75 per hr $11.50 per hr $5.00 per hr per unit $7.00 $13.80 $6.00 per unit Direct Materials Direct Labor Variable Overhead 4 1.2 1.2 Manufacturing overhead is applied using direct labor hours as the base. During the month of July, XYZ company had the following information available about production: a. 9,000 units were produced b. 37,000 lbs of raw materials were purchased at a cost of $62,900 c. There was no beginning inventory and no ending iInventory of raw materials d. 10,500 hours of direct labor were used during the month at a cost of $119,175 e. Variable overhead cost in July totaled $57,750 Compute the following and verify the total variance for each component of product cost: 1. Material price variance, Material quantity variance, and Total material variance 2. Labor rate variance, Labor efficiency variance, and Total labor variance 3. Variable Overhead spending variance, Variable Overhead efficiency variance,…arrow_forwardQuestion Two Apex Ltd manufactures three products X, Y and Z in two product ion departments; P1 and Pz. The company also has two service departments: Sı and Sz. The company's budgeted product ion data and manufacturing costs for the year 2021 were as f ollows: Product Product ion (units) Direct materials (Shs. per unit) Direct labour: P: (Shs. per unit) 4,200 6,900 1,700 11 14 17 6 4 2 P2 (shs. Per unit) 12 3 21 Machine hours per unit 6 3 4 Additional information 1. Absorpt ion rates in depart ments Pı and Pz are based on machine hours and labour wages respectively. 2. Budgeted overheads for rent, heating and lighting amounted to shs.17,000 while depreciation and ins urance amount ed to shs.25,000, 3. The costs of service department Szare apportioned to production departments Pi and P2 at the ratio of 7:3 while the costs of Si are apportioned to depart ments Pi Pz and Sz based on the number of employees. 4. Other information includes: P1 Pz S. Sz 27,660 19,47o 16,600 26,650 Budgeted…arrow_forwardQuestion Content Area The following data relate to direct labor costs for the current period: Line Item Description Value Standard costs 7,000 hours at $11.80 Actual costs 6,300 hours at $10.80 The direct labor rate variance is a. $14,560 unfavorable b. $6,300 favorable c. $14,560 favorable d. $8,260 favorablearrow_forward

- Budget Standard per unit Actual production 50 units 30 units Direc material usage 4 Ibs. @ $ 0.5 per Ib 140 Ibs @ $ 1 per Ib. Direct labour usage 2hrs. @ $ 1 per hour 72 hrs @ $ 0.75 per hr. Compute a) Material price variance b)Material quantity variance c)Total material variance d)Labor rate variance e) Labor efficiency variance f) Total pabor variancearrow_forwardQuestion Content Area Myers Corporation has the following data related to direct materials costs for November: actual cost for 4, 690 pounds of material at $5.30 and standard cost for 4, 410 pounds of material at $6.30 per pound. The direct materials price variance is a. $1,764 favorable b. $4,690 favorable c. $1,764 unfavorable d. $4,690 unfavorablearrow_forwardExercise 5: Computation for Overhead Variance and Journal Entries Golden Manufacturers, Inc. applies factory overhead at P8 per direct labor hour. Actual factory overhead and actual labor hours for 19F were P470,500 and 58,000 hours, respectively. Normal capacity is 60,000 hours.arrow_forward

- Question # 1 Standard and the actual costs for direct materials and direct labor are given as under: Standard costs Direct materials 8,000 units at total direct material costs Rs. 40,000 Direct labor: 7,000 hours at Rs. 6 per hour Actual costs Direct materials 8,500 units at Rs. 4.5 per unit Direct labor: 6,500 hours at Rs. 6.25 per hour Required a. Material Price Variance and Material Quantity Variance b. Labor Rate Variance and Labor Efficiency Variancearrow_forwardTotal actual overhead incurred -12,600 Fixed overhead budgeted Total - 3,300 Total tandard overhead rate per DLH -4 Variable overhead rate per DLH -3 Standard hours allowed for actual production -3,500 IT Company uses a standard cost system. Overhead cost information for Product CO for the month of October is as follows: What is the overall or net overhead variance? A.P1,200 F B.P1,200 U C.P1,400 F D.P1,200 Uarrow_forward#3 Required information [The following information applies to the questions displayed below.] A manufactured product has the following information for June. Direct materials Direct labor Overhead Units manufactured Standard Quantity and Cost 6 pounds @ $9 per pound 2 DLH @ $17 per DLH 2 DLH @ $12 per DLH Total budgeted (standard) cost Actual Results (1) Prepare the standard cost card showing standard cost per unit. (2) Compute total budgeted cost for June production. (3) Compute total actual cost for June production. (4) Compute total cost variance for June.arrow_forward

- Problem 8 Material and Labor Variance Journal Entries Clyette Corporation uses a standard cost system and has the following standard costs for direct materials and direct labor. Direct materials: Direct labor 2.5 meters @ P14 per meter 1.6 hours @ P8 per hour P35.00 P12.80 During the month of February, 15,000 units were produced. The costs related to the production of the product were as follows: • 50,000 meters of materials were purchased at a cost of P13.80 per meter. 40,000 meters of materials were used. 25,000 direct labor hours were used at a cost of P8.60 per hour. Required: Prepare the journal entries to record the purchased of materials, used of materials and labor incurrence.arrow_forwardRefer to the data in Exercise 9.15. Required: 1. Compute overhead variances using a two-variance analysis. 2. Compute overhead variances using a three-variance analysis. 3. Illustrate how the two- and three-variance analyses are related to the four-variance analysis. Oerstman, Inc., uses a standard costing system and develops its overhead rates from the current annual budget. The budget is based on an expected annual output of 120,000 units requiring 480,000 direct labor hours. (Practical capacity is 500,000 hours.) Annual budgeted overhead costs total 787,200, of which 556,800 is fixed overhead. A total of 119,400 units using 478,000 direct labor hours were produced during the year. Actual variable overhead costs for the year were 230,600, and actual fixed overhead costs were 556,250. Required: 1. Compute the fixed overhead spending and volume variances. How would you interpret the spending variance? Discuss the possible interpretations of the volume variance. Which is most appropriate for this example? 2. Compute the variable overhead spending and efficiency variances. How is the variable overhead spending variance like the price variances of direct labor and direct materials? How is it different? How is the variable overhead efficiency variance related to the direct labor efficiency variance?arrow_forwardActivity-based department rate product costing and product cost distortions Big Sound Inc. manufactures two products: receivers and loud-speakers. The factory overhead incurred is as follows: Indirect labor 400,400 Cutting Department 198,800 Finishing Department 114,800 Total 714,000 The activity base associated with the two production departments is direct labor hours. The indirect labor can be assigned to two different activities as follows: Activity Budgeted Activity Cost Activity Base Setup 138,600 Number of setup Quality Control 261,800 Number of inspections Total 400,400 The activity-base usage quantities and units produced for the two products follow: Number o Setup Number of Inspections Direct Labor HoursSubassembly Direct Labor HoursFinal Assembly Units Produced Snowboards 430 5,000 4,000 2,000 6,000 Skis _70 2,500 2,000 4,000 6,000 Total 500 7,500 6,000 6,000 12,000 Instructions 1. Determine the factory overhead rates under the multiple production department rate method. Assume that indirect labor is associated with the production departments, so that the total factory overhead is 5420,000 and 294,000 for the Subassembly and Final Assembly departments, respectively. 2. Determine the total and per-unit factory overhead costs allocated to each product, using the multiple production department overhead rates in (1). 3. Determine the activity rates, assuming that the indirect labor is associated with activities rather than with the production departments. 4. Determine the total and per-unit cost assigned to each product under activity-based costing. 5. Explain the difference in the per-unit overhead allocated to each product under the multiple production department factory overhead rate and activity-based costing methods.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning