Concept explainers

Videos

Problem 2-37A Effect of

CHECK FIGURES

d. Adjustment amount: $4,000

Required

Each of the following independent events requires a year-end adjusting entry. Show how each event and its related adjusting entry affect the accounting equation. Assume a December 31 closing date. The first event is shown as an example.

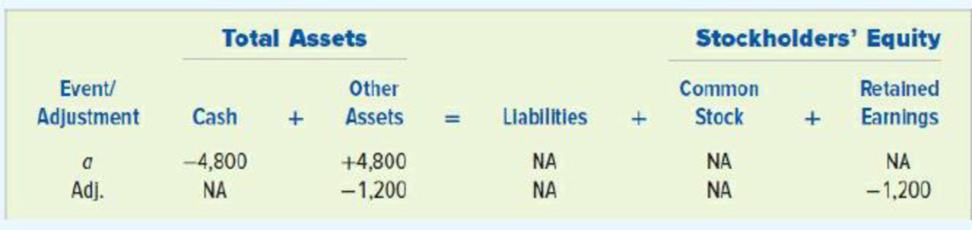

- a. Paid $4,800 cash in advance on October 1 for a one-year insurance policy.

- b. Received a $3,600 cash advance for a contract to provide services in the future. The contract required a one-year commitment, starting April 1.

- c. Purchased $1,200 of supplies on account. At year’s end, $175 of supplies remained on hand.

- d. Paid $9,600 cash in advance on August 1 for a one-year lease on office space.

Show the manner in which the events and its related adjusting entries would affect the accounting equation.

Answer to Problem 33P

Prepare a table exhibiting the events and the adjusting entries that would affect the accounting equation are as follows:

| Company | ||||||||

| Accounting equation | ||||||||

| Event / Adjustment | Total Assets | = | Liabilities | + | Stockholder's Equity | |||

| Cash | Other assets | Common Stock | Retained Earnings | |||||

| a. (Given) | ($4,800) | + | $4,800 | = | NA | + | NA | NA |

| Adjustment (1) | NA | + | ($1,200) | = | NA | + | NA | ($1,200) |

| b. | $3,600 | + | NA | = | $3,600 | + | NA | NA |

| Adjustment (2) | NA | + | NA | = | ($2,700) | + | NA | $2,700 |

| c. | NA | + | $1,200 | = | $1,200 | + | NA | NA |

| Adjustment (3) | NA | + | ($1,025) | = | NA | + | NA | ($1,025) |

| d. | ($9,600) | + | $9,600 | = | NA | + | NA | NA |

| Adjustment (4) | NA | + | ($4,000) | = | NA | + | NA | ($4,000) |

Table (1)

Explanation of Solution

Accounting equation: Accounting equation is an accounting tool expressed in the form of equation, by creating a relationship between the resources or assets of a company, and claims on the resources by the creditors and the owners. Accounting equation is expressed as shown below.

The effects of the events and adjustments can be explained as follows:

a. Paid $4,800 cash in advance on October 1 for a one-year insurance policy.

The cash account (asset) is decreased by $4,800 and the prepaid insurance (asset) account is increased by $4,800. When the insurance expense is recognized for 3 months at the end of the year, the prepaid insurance (asset) account is decreased by $1,200 (1) and amount of insurance expense (expense account) is increased by $1,200. Increase in insurance expense account decreases the retained earnings by the same amount.

b. Received a $3,600 cash advance for a contract to provide services in the future. The contract required a one-year commitment, starting April 1.

The cash account (asset) is increased by $3,600 and the unearned revenue account (liability) is increased by $3,600. The revenue would be recognized when the services are provided to the client. After providing the service for 9 months from April 1 to December 31, revenue should be recognized for 9 months at the end of the year. While recognizing the earned unearned revenue, the unearned revenue (liability) is decreased by $2,700 (2) and the revenue account is increased by $2,700. Increase in revenue account increases the retained earnings by the same amount.

c. Purchased $1,200 of supplies on account. At year’s end, $175 of supplies remained on hand.

The supplies account (asset) is increased by $1,200 and the accounts payable (liability) account is increased by $1,200. When the supplies expenses are recognized, the supplies account (asset) is decreased by $1,025 (3) and the expense account is increased by $1,025. Increase in the expense account decreases the retained earnings by the same amount.

d. Paid $9,600 cash in advance on August 1 for a one-year lease on office space.

The cash account (asset) is decreased by $9,600 and the prepaid rent (asset) account is increased by $9,600. When the rent expense is recognized at the end of the year for 3 months, the prepaid rent (asset) account is decreased by $4,000 (4) and amount of insurance expense (expense account) is increased by $4,000. Increase in insurance expense account decreases the retained earnings by the same amount.

Working Note:

Determine the amount of prepaid insurance recognized at the end of year.

Determine the amount of revenue recognized at the end of year.

Determine the amount of supplies used at the end of year.

Determine the amount of prepaid rent recognized at the end of year.

Want to see more full solutions like this?

Chapter 2 Solutions

Survey Of Accounting

- Year 1 General Journal tab - Prepare the Year 2 journal entries related to the notes and accounts receivable of Clark Co. Calculation of interest tab - Use the interest formula (P x R x T) to verify the amount of interest recorded in your entries. Verify that total interest revenue agrees with the trial balance. Dec. 16 Accepted a $14,400, 60-day, 8% note in granting Hao Lee a time extension on his past-due account receivable. 31 Made an adjusting entry to record the accrued interest on the Lee note. Year 2 Feb. 14 Received Lee’s payment of principal and interest on the note dated December 16. Mar. 2 Accepted a $9,000, 8%, 90-day note in granting a time extension on the past-due account receivable from Taylor Co. 17 Accepted a $4,200, 30-day, 10% note in granting Susan Allen a time extension on her past-due account receivable. Apr. 16 Allen dishonored her note. May 31 Taylor Co. dishonored its note. Aug. 7…arrow_forwardJOURNAL ENTRIES (ACCRUED INTEREST RECEIVABLE) At the end of the year, the following interest is earned, but not yet received. Record the adjusting entry in a general journal. Interest on 6,000, 60-day, 5.5% note (for 24 days) 22.00 Interest on 9,000, 90-day, 6% note (for 12 days) 18.00 40.00arrow_forwardUNCOLLECTIBLE ACCOUNTSALLOWANCE METHOD Lewis Warehouse used the allowance method to record the following transactions, adjusting entries, and closing entries during the year ended December 31, 20--: Selected accounts and beginning balances on January 1, 20--, are as follows: REQUIRED 1. Open the three selected general ledger accounts. 2. Enter the transactions and the adjusting and closing entries in a general journal (page 6). After each entry, post to the appropriate selected accounts. 3. Determine the net realizable value as of December 31, 20--.arrow_forward

- UNCOLLECTIBLE ACCOUNTSALLOWANCE METHOD Pyle Nurseries used the allowance method to record the following transactions, adjusting entries, and closing entries during the year ended December 31, 20--. REQUIRED 1. Open the three selected general ledger accounts. 2. Enter the transactions and the adjusting and closing entries in a general journal (page 6). After each entry, post to the appropriate selected accounts. 3. Determine the net realizable value as of December 31.arrow_forwardSALES RETURNS AND ALLOWANCES ADJUSTMENT At the end of year 1, MCs estimates that 2,400 of the current years sales will be returned in year 2. Prepare the adjusting entry at the end of year 1 to record the estimated sales returns and allowances and customer refunds payable for this 2,400. Use accounts as illustrated in the chapter.arrow_forwardPrepaid Rent—Quarterly Adjustments On September 1, Northhampton Industries signed a six-month lease for office space, which is effective September 1. Northhampton agreed to prepay the rent and mailed a check for $12,000 to the landlord on September 1. Assume that Northhampton prepares adjusting entries only four times a year: on March 31, June 30, September 30, and December 31. Required Compute the rental cost for each full month. Prepare the journal entry to record the payment of rent on September 1. Prepare the adjusting entry on September 30. Assume that the accountant prepares the adjusting entry on September 30 but forgets to record an adjusting entry on December 31. Will net income for the year be understated or overstated? by what amount?arrow_forward

- Interest Payable—Quarterly Adjustments Glendive takes out a 12%, 90-day, $100,000 loan with Second State Bank on March 1, 2016. Assume that Glendive prepares adjusting entries only four times a year: on March 31, June 30, September 30, and December 31. Required Prepare the journal entry on March 1, 2016. Prepare the adjusting entry on March 31, 2016. Prepare the entry on May 30, 2016, when Glendive repays the principal and interest to Second State Bank.arrow_forwardBrief Exercise 11-02 Sheridan Company borrows $53,400 on July 1 from the bank by signing a $53,400, 8%, one-year note payable. (a) Prepare the journal entry to record the proceeds of the note. (b) Prepare the journal entry to record accrued interest at December 31, assuming adjusting entries are made only at the end of the year. (Credit account titles are automatically indented when amount is entered. Do not indent manually. Record journal entries in the order presented in the problem.) No. Date Account Titles and Explanation Debit Credit (a) July 1Dec. 31 (b) July 1Dec. 31arrow_forwardQuestion Content Area Analysis of receivables method At the end of the current year, Accounts Receivable has a balance of $880,000; Allowance for Doubtful Accounts has a credit balance of $8,000; and sales for the year total $3,960,000. Using the aging method, the balance of Allowance for Doubtful Accounts is estimated as $36,800. a. Determine the amount of the adjusting entry for uncollectible accounts.fill in the blank 1 of 1$ b. Determine the adjusted balances of Accounts Receivable, Allowance for Doubtful Accounts, and Bad Debt Expense. Line Item Description Amount Accounts Receivable $fill in the blank 2 Allowance for Doubtful Accounts $fill in the blank 3 Bad Debt Expense $fill in the blank 4 c. Determine the net realizable value of accounts receivable.fill in the blank 1 of 1$arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

- Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage