Concept explainers

Videos

FIFO method (continuation of 17-41).

- 1. Complete Problem 17-41 using the FIFO method of

process costing .

Required

- 2. If you did Problem 17-41, explain any difference between the cost of work completed and transferred out and the cost of ending work in process in the assembly department under the weighted-average method and the FIFO method. Should McKnight’s managers choose the weighted-average method or the FIFO method? Explain briefly.

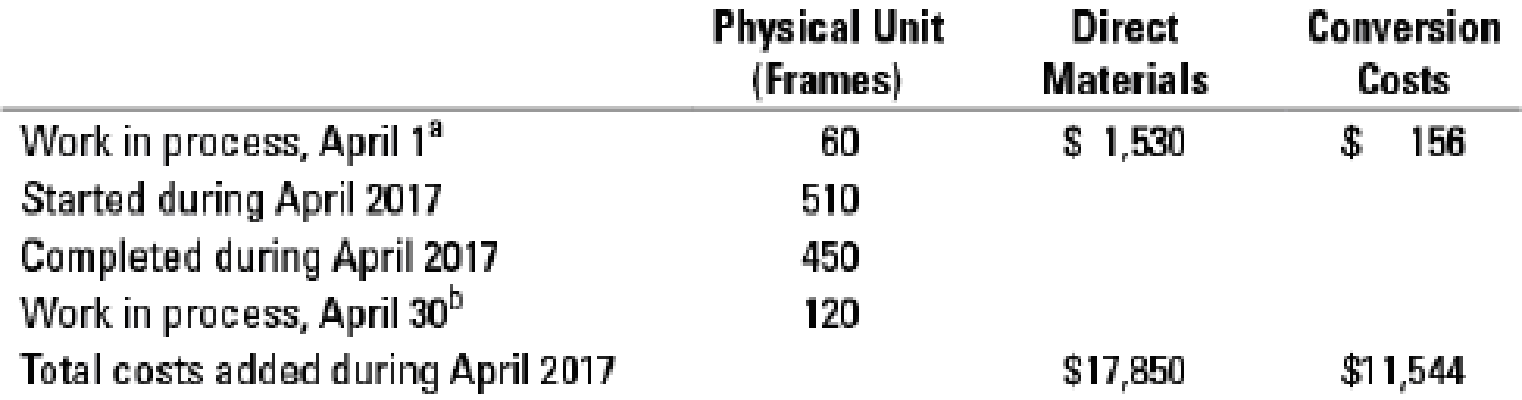

17-41 Weighted-average method. McKnight Handcraft is a manufacturer of picture frames for large retailers. Every picture frame passes through two departments: the assembly department and the finishing department. This problem focuses on the assembly department. The process-costing system at McKnight has a single direct-cost category (direct materials) and a single indirect-cost category (conversion costs). Direct materials are added when the assembly department process is 10% complete. Conversion costs are added evenly during the assembly department’s process.

McKnight uses the weighted-average method of process costing. Consider the following data for the assembly department in April 2017:

a Degree of completion: direct materials, 100%; conversion costs, 40%.

b Degree of completion: direct materials, 100%; conversion costs, 15%.

- 1. Summarize the total assembly department costs for April 2017, and assign them to units completed (and transferred out) and to units in ending work in process.

Required

- 2. What issues should a manager focus on when reviewing the equivalent units calculation?

Want to see the full answer?

Check out a sample textbook solution

Chapter 17 Solutions

Horngren's Cost Accounting: A Managerial Emphasis (16th Edition)

- Which of the following product situations is better suited to job order costing than to process costing? A. Each product batch is exactly the same as the prior batch. B. The costs are easily traced to a specific product. C. Costs are accumulated by department. D. The value of work in process is based on assigning standard costs.arrow_forwardA company has traditionally allocated its overhead based on machine hours but collected this information to change to activity based costing: A. How much overhead would be assigned to each unit under the traditional allocation method? B. How much overhead would be assigned to each unit under activity-based costing?arrow_forwardFields Company has two manufacturing departments, forming and painting. The company uses the weighted average method and it reports the following unit data for the Forming department. Units completed in the forming department are transferred to the painting department. Beginning work in process inventory Units started this period Completed and transferred out Ending work in process inventory Production cost information for the forming department follows. Beginning work in process Direct materials Units 34,500 490,000 494,500 30,000 Conversion Costs added this period Direct materials Conversion Total costs to account for $ 56,200 22,900 1,800, 200 1, 179,000 Direct Materials Percent Complete 80% 85% $79,100 2,979,200 $ 3,058, 300 Conversion Percent Complete 20% 35%arrow_forward

- A 1.Describe the differences between process costing and job 5.4 costing.2. Distinguish between normal and abnormal losses and explain.3. Provide examples of industries that use process costing. 4. Why is cost accumulation easier with a process costing system compared with a job costing system? 5. What are equivalent units? Why are they needed with a process costing system?arrow_forwardTwo years ago, company scientists developed an alloy with all of the properties of the raw materials used in XL-D that generates no wastewater. Some prototype components using the new material were produced and tested and found to be indistinguishable from the old components in every way relating to their fitness for use. The only difference is that the new alloy is more expensive than the old raw material. The company has been test-marketing the newer version of the component, referred to as XL-C, and is currently trying to decide its fate. Manufacturing of both components begins in the Production Department and is completed in the Assembly Department. No other products are produced in the plant. The following information relates to the two components: Units produced Raw material costs per unit Direct labor-hours per unit-Production Direct labor-hours per unit-Assembly Direct labor rate per hour-all labor Machine-hours per unit-Production Machine-hours per unit-Assembly Testing hours…arrow_forwardPrecision Manufacturing Inc. (PMI) makes two types of industrial component parts-the EX300 and the TX500. It annually produces 69,000 units of EX300 and 13,400 units of TX500. The company's conventional cost system allocates manufacturing overhead to products using a plantwide overhead rate and direct labor dollars as the allocation base. Additional information relating to the company's two product lines is shown below: EX300 $375,325 $129,000 Total $546,875 $176,000 TX500 Direct materials Direct labor $171,550 $ 47,000 The company is considering implementing an activity-based costing system that distributes all of its manufacturing overhead to four activities as shown below: Activity Manufacturing Overhead $182,600 249,900 187,070 84,460 $704,000 Activity Cost Pool (and Activity Measure) Machining (machine-hours) Setups (setup hours) Product-level (number of products) General factory (direct labor dollars) EX300 99,000 120 1 TX500 67,000 390 1 Total 166,000 510 2 $129,000 $47,000…arrow_forward

- ! Required information [The following information applies to the questions displayed below.] For many years, Thomson Company manufactured a single product called LEC 40. Then three years ago, the company automated a portion of its plant and at the same time introduced a second product called LEC 90 that has become increasingly popular. The LEC 90 is a more complex product, requiring 0.60 hours of direct labor time per unit to manufacture and extensive machining in the automated portion of the plant. The LEC 40 requires only 0.20 hours of direct labor time per unit and only a small amount of machining. Manufacturing overhead costs are currently assigned to products on the basis of direct labor-hours. Despite the growing popularity of the company's new LEC 90, profits have been declining steadily. Management is beginning to believe that there may be a problem with the company's costing system. Direct material and direct labor costs per unit are as follows: Direct materials Direct labor…arrow_forwardTime left Activity-based costing: O a. provides the same results as the departmental overhead costing O b. typically applies overhead costs using direct labor-hours O c. None of the given answer. O d. does not assign any non-manufacturing overhead costs to product costs. O e. uses a pool rate for all costs incurred by the same activity which can reduce the number of cost assignments required. CLEAR MY CHOICE In Al-Waha Water Bottling Company, costs incurred for research and developments would be classified as a: O a. none of the given answers. O b. Unit level activity. of O c. Batch level activity. O d. Organization- sustaining level activity. O e. Product- sustaining level activity. CLEAR MY CHOICE NEXT PAGE MacBook Air FB F7 吕口 F3 F5 F1 F2 * % $ 4 @ 7 8 A9 6 一 W E R Y *** ق DSF G K S ش X, C V BiN M %#3arrow_forward[AICPAJ In a process cost system, the application of factory overhead usually would 1. Which of the following statement is not a feature of process costing system? The cost of completed units of one production process becomes the raw material input of the next production process. a. b. Incomplete units at each stage of production process are converted into equivalent units based on the degree of incompleteness. Because the manufacturing process is continuous, the production cost is allocated between the completed and uncompleted units at the end of the accounting period. C. d. None of the above 2. Which of the following statement is correct with respect to job order costing and process costing? The selection between job order costing and process costing depends on the nature of the products and the methods of processing them. a. In job order costing, costs are accumulated for each job while in process costing, costs are accumulated for each process. b. In process costing, production is…arrow_forward

- Carrie's Limited has two departments, the assembly department and the testing department in its brake-pad manufacturing plant, where each brake-pad is conveyed through each department. Carrie's process-costing system consist of two cost categories: Single direct cost (direct materials) and a single indirect-cost category (conversion costs). Direct materials are added at the beginning of the process. Conversion costs are added evenly during the process. When the assembly department finishes work on each brake-pad, it is immediately transferred to testing. Carrie's uses the weighted-average method of process costing. Data for the assembly department for October 2019 are as follows: Physical Units (Brake Pads) Work in process, October 1* Started during October 2019 21,000 Completed during October 2019 23,500 6,000 Direct Materials $1,200,000 Work in process, October 31¹ 3,500 Total costs added during October 2019 $4,600,000 x Degree of completion: direct materials, 100%; conversion costs,…arrow_forwardOriole Stairs Co. designs and builds factory-made premium wooden stairways for homes. The manufactured stairway components (spindles, risers, hangers, hand rails) permit installation of stairways of varying lengths and widths. All are of white oak wood. Budgeted manufacturing overhead costs for the year 2025 are as follows. Overhead Cost Pools Purchasing Handling materials Production (cutting, milling, finishing) Setting up machines Inspecting Inventory control (raw materials and finished goods) Utilities Total budgeted overhead costs Purchasing Handling materials Production (cutting, milling, finishing) Setting up machines For the last 4 years, Oriole Stairs Co. has been charging overhead to products on the basis of machine hours. For the year 2025, 100,000 machine hours are budgeted. Activity Cost Pools Inspecting Inventory control (raw materials and finished goods) Utilities Jeremy Nolan, owner-manager of Oriole Stairs Co., recently directed his accountant, Bill Seagren, to…arrow_forwardThe current cost accounting system charges overhead to products based on machine-hours. What unit product costs will be reported for the two products if the current cost system continues to be used? (Round intermediate calculations and "Per unit cost" answers to 2 decimal places.) 308 510 Total cost Per unit cost A consulting firm has recommended using an activity-based costing system, with the activities based on the cost pools identified by the cost accountant. What are the cost driver rates for the four cost pools identified by the cost accountant? (Round your answers to 2 decimal places.) Incoming inspection % of material dollars Production per machine-hour Machine setup per setup Shipping per unit What unit product costs will be reported for the two products if the ABC system suggested by the cost accountant’s classification of…arrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College