Videos

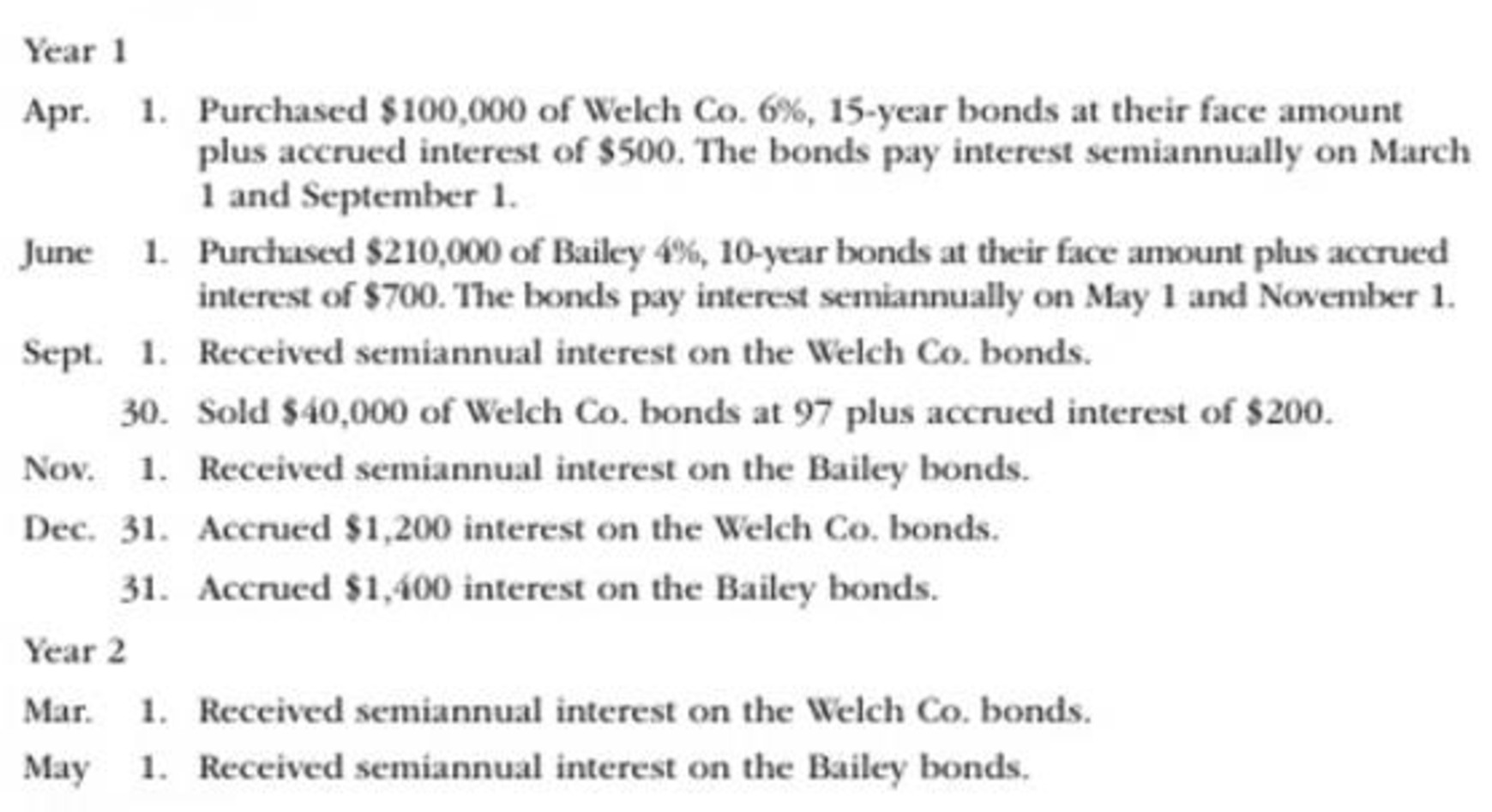

Soto Industries Inc. is an athletic footware company that began operations on January 1, Year 1. The following transactions relate to debt investments acquired by Soto Industries Inc., which has a fiscal year ending on December 31:

Instructions

- 1.

Journalize the entries to record these transactions. - 2. If the bond portfolio is classified as available for sale, what impact would this have on financial statement disclosure?

(1)

Journalize the bond investment transactions in the books of Company G.

Explanation of Solution

Bond investment: Bond investments are debt securities which pay a fixed interest revenue to the investor.

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for purchase of $100,000 bonds of Company W, at face amount with an accrued interest of $500.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| April | 1 | Investments–Company W Bonds | 100,000 | ||

| Interest Receivable | 500 | ||||

| Cash | 100,500 | ||||

| (To record purchase of Company W bonds for cash) | |||||

Table (1)

- Investments–Company W Bonds is an asset account. Since bonds investments are purchased, asset value increased, and an increase in asset is debited.

- Interest Receivable is an asset account. Since interest to be received has increased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Prepare journal entry for purchase of $210,000 bonds of Company B, at face amount with an accrued interest of $700.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| June | 1 | Investments–Company B Bonds | 210,000 | ||

| Interest Receivable | 700 | ||||

| Cash | 210,700 | ||||

| (To record purchase of Company B bonds for cash) | |||||

Table (2)

- Investments–Company B Bonds is an asset account. Since bonds investments are purchased, asset value increased, and an increase in asset is debited.

- Interest Receivable is an asset account. Since interest to be received has increased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Prepare journal entry to record the interest revenue received from Company W bonds.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| September | 1 | Cash | 3,000 | ||

| Interest Receivable | 500 | ||||

| Interest Revenue | 2,500 | ||||

| (To record receipt of interest revenue) | |||||

Table (3)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Interest Receivable is an asset account. Since interest to be received is received, asset value decreased, and a decrease in asset is credited.

- Interest Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of interest received from Company W.

Prepare journal entry for $40,000 bonds of Company W sold at 97%, with an accrued interest of $200.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| September | 30 | Cash | 39,000 | ||

| Loss on Sale of Investments | 1,200 | ||||

| Interest Revenue | 200 | ||||

| Investments–Company W Bonds | 40,000 | ||||

| (To record sale of M City bonds) | |||||

Table (3)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Loss on Sale of Investments is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Interest Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

- Investments–Company W Bonds is an asset account. Since bond investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the cash received from the sale of bonds.

| Particulars | Amount ($) |

| Cash proceeds from sale of $40,000 bonds | 38,800 |

| Add: Accrued interest revenue | 200 |

| Cash received | $39,000 |

Table (4)

Calculate the realized gain (loss) on sale of $40,000 bonds.

| Particulars | Amount ($) |

| Cash proceeds from sale of $40,000 bonds | 38,800 |

| Cost of bonds sold | (40,000) |

| Gain (loss) on sale of bonds | $(1,200) |

Table (5)

Prepare journal entry to record the interest revenue received from Company B bonds.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| November | 1 | Cash | 4,200 | ||

| Interest Receivable | 700 | ||||

| Interest Revenue | 3,500 | ||||

| (To record receipt of interest revenue) | |||||

Table (6)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Interest Receivable is an asset account. Since interest to be received is received, asset value decreased, and a decrease in asset is credited.

- Interest Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of interest received from Company B.

Prepare journal entry for accrued interest.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| December | 31 | Interest Receivable | 1,200 | ||

| Interest Revenue | 1,200 | ||||

| (To record interest accrued) | |||||

Table (7)

- Interest Receivable is an asset account. Since interest to be received has increased, asset value increased, and an increase in asset is debited.

- Interest Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Prepare journal entry for accrued interest.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 1 | |||||

| December | 31 | Interest Receivable | 1,400 | ||

| Interest Revenue | 1,400 | ||||

| (To record interest accrued) | |||||

Table (8)

- Interest Receivable is an asset account. Since interest to be received has increased, asset value increased, and an increase in asset is debited.

- Interest Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Prepare journal entry to record the interest revenue received from Company W bonds.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 2 | |||||

| May | 1 | Cash | 1,800 | ||

| Interest Receivable | 1,200 | ||||

| Interest Revenue | 600 | ||||

| (To record receipt of interest revenue) | |||||

Table (9)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Interest Receivable is an asset account. Since interest to be received is received, asset value decreased, and a decrease in asset is credited.

- Interest Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of interest received from Company W.

Prepare journal entry to record the interest revenue received from Company B bonds.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| Year 2 | |||||

| May | 1 | Cash | 4,200 | ||

| Interest Receivable | 1,400 | ||||

| Interest Revenue | 1,800 | ||||

| (To record receipt of interest revenue) | |||||

Table (10)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Interest Receivable is an asset account. Since interest to be received is received, asset value decreased, and a decrease in asset is credited.

- Interest Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of interest received from Company B.

(2)

Explain the impact of bonds, if the portfolio is classified as available-for-sale investment.

Explanation of Solution

Available-for-sale investments are reported at fair value. If the bond portfolio is classified as available-for-sale investment, the bond portfolio should be reported at fair value. The changes in the cost and fair value would be adjusted using the valuation account and unrealized gain (loss) account.

Want to see more full solutions like this?

Chapter 15 Solutions

Financial Accounting

- Rekya Mart Inc. is a general merchandise retail company that began operations on January 1, Year 1. The following transactions relate to debt investments acquired by Rekya Mart Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. If the bond portfolio is classified as available for sale, what impact would this have on financial statement disclosure?arrow_forwardRios Financial Co. is a regional insurance company that began operations on January 1, Year 1. The following transactions relate to trading securities acquired by Rios Financial Co., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. Prepare the investment-related current asset balance sheet presentation for Rios Financial Co. on December 31, Year 2. 3. How are unrealized gains or losses on trading investments presented in the financial statements of Rios Financial Co.?arrow_forwardGlacier Products Inc. is a wholesaler of rock climbing gear. The company began operations on January 1, Year 1. The following transactions relate to securities acquired by Glacier Products Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record the preceding transactions. 2. Prepare the investment-related asset and stockholders equity balance sheet presentation for Glacier Products Inc. on December 31, Year 2, assuming that the Retained Earnings balance on December 31, Year 2, is 700,000.arrow_forward

- Forte Inc. produces and sells theater set designs and costumes. The company began operations on January 1, Year 1. The following transactions relate to securities acquired by Forte Inc., which has a fiscal year ending on December 31: Instructions 1. Journalize the entries to record these transactions. 2. Prepare the investment-related asset and stockholders equity balance sheet presentation for Forte Inc. on December 31, Year 2, assuming that the Retained Earnings balance on December 31, Year 2, is 389,000.arrow_forwardRefer to the information in RE13-5. Assume that on December 31, 2019, the investment in Smith Corporation bonds has a market value of 12,500. Prepare the year-end journal entry to record the unrealized gain or loss.arrow_forwardAmalgamated General Corporation is a consulting firm that also offers financial services through its credit division. From time to time the company buys and sells securities. The following selected transactions relate to Amalgamated’s investment activities during the last quarter of 2021 and the first month of 2022. The only securities held by Amalgamated at October 1, 2021 were $40 million of 10% bonds of Kansas Abstractors, Inc., purchased on May 1, 2021 at face value and held in Amalgamated’s trading securities portfolio. The company’s fiscal year ends on December 31. 2021 Oct. 18 Purchased 2 million shares of Millwork Ventures Company common stock for $58 million. Millwork has a total of 34 million shares issued. 31 Received semiannual interest of $1.6 million from the Kansas Abstractors bonds. Nov. 1 Sold the Kansas Abstractors bonds for $36 million because rising interest rates are expected to cause their fair…arrow_forward

- Prepare Natura Company’s journal entries to record the following transactions involving its short-term investments in held-to-maturity debt securities, all of which occurred during the current year. On June 15, paid $254,000 cash to purchase Remed’s 90-day short-term debt securities ($254,000 principal), dated June 15, that pay 9% interest. On September 16, received a check from Remed in payment of the principal and 90 days' interest on the debt securities purchased in transaction a. Note: Use 360 days in a year. Do not round your intermediate calculations.arrow_forwardPrepare Natura Company’s journal entries to record the following transactions involving its short-term investments in held-to-maturity debt securities, all of which occurred during the current year. On June 15, paid $210,000 cash to purchase Remed’s 90-day short-term debt securities ($210,000 principal), dated June 15, that pay 7% interest. On September 16, received a check from Remed in payment of the principal and 90 days' interest on the debt securities purchased in transaction a. Note: Use 360 days in a year. Do not round your intermediate calculations. On June 15, paid $210,000 cash to purchase Remed's 90-day short-term debt securities ($210,000 principal), dated June 15, that pay 7% interest. 2 On September 16, received a check from Remed in payment of the principal and 90 days’ interest on the debt securities purchased in transaction a.arrow_forwardDebt investment transactions, available-for-sale valuationSoto Industries Inc. in an athletic foot ware company that beganoperations on January 1, Year 1. The following transactions relate to debtinvestments acquired by Solo Industries Inc., which has a fiscal yearending on December 31: Instructions1. Journalize the entries to record these transactions.2. If the bond portfolio is classified as available for sale, what impactwould this have on financial statement disclosure?arrow_forward

- You are in charge of auditing PLM (PopoyLangMalakas) Company's investment accounts for the year ended December 31, 2021, which was incorporated last March 3, 2020. During the course of the audit, you have obtained the balances and the related journal entries of its investment related transactions and have revealed the following information: Investment in Bonds P101,258 Investment in Stocks 62,400 Total P163,658 Journal Entries: Investment in bonds - 10% treasury bonds from the Banko Sentral ng Pilipinas. The investment is in a portfolio which has the objective of collecting contractual cash flows. Date Account Debit Credit July 1, 2020 Investment in BSP bonds 105, 242 Cash 105, 242 To record the acquisition of P100,000 face value BSP bonds December 31, 2020 Unrealized Gain / (Loss) on market changes 2,242 Investment in BSP bonds…arrow_forwardYou are in charge of auditing PLM (PopoyLangMalakas) Company's investment accounts for the year ended December 31, 2021, which was incorporated last March 3, 2020. During the course of the audit, you have obtained the balances and the related journal entries of its investment related transactions and have revealed the following information: Investment in Bonds P101,258 Investment in Stocks 62,400 Total P163,658 Journal Entries: Investment in bonds - 10% treasury bonds from the Banko Sentral ng Pilipinas. The investment is in a portfolio which has the objective of collecting contractual cash flows. Date Account Debit Credit July 1, 2020 Investment in BSP bonds 105, 242 Cash 105, 242 To record the acquisition of P100,000 face value BSP bonds December 31, 2020 Unrealized Gain / (Loss) on market changes 2,242 Investment in BSP bonds…arrow_forwardHusky Corporation is a general contractor which occasionally invests excess cash in debt securities. The following transactions took place in the fourth quarter of 2021. On October 1, 2021, purchased $6 million of 3% Microsoft bonds at par value. These bonds pay interest on June 30 and December 31 of each year, and were classified as Held to Maturity (“HTM”). On November 1, 2021, purchased $3 million of 4% Amazon bonds at par value. These bonds pay interest on September 30 and March 31 of each year, and were classified as Available for Sale (“AFS”) On December 1, 2021, purchased $2 million of 3% US Treasury Bonds at par value, hoping to earn profits on short-term price increases driven by a decline in interest rates. These bonds were classified as Trading Securities. (“TS”) On December 31, 2021, received the interest payment ($45,000) on the Microsoft bonds purchased on October 1. Requirements: Prepare journal entries for the transactions in a. through d. above. Prepare journal…arrow_forward

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning