Concept explainers

(1)

Trading securities:

These are short-term investments in debt and equity securities with an intention of trading and earning profits due to changes in market prices.

Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in

stockholders’ equity accounts. - Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

To journalize: The stock investment transactions in the books of Company SF.

(1)

Explanation of Solution

Prepare journal entry for the purchase of 5,000 shares of Company W, at $40 per share, and a brokerage commission of $500.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| March | 14 | Investments–Company W Stock | 200,500 | ||

| Cash | 200,500 | ||||

| (To record purchase of shares for cash) | |||||

Table (1)

- Investments–Company W Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company W’s stock.

Prepare journal entry for the purchase of 1,800 shares of Company M, at $50 per share, and a brokerage commission of $198.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| April | 24 | Investments–Company M Stock | 90,198 | ||

| Cash | 90,198 | ||||

| (To record purchase of shares for cash) | |||||

Table (2)

- Investments–Company M Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company M’s stock.

Prepare journal entry for sale of 2,600 shares of Company W, at $38, with a brokerage of $100.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| June | 1 | Cash | 98,700 | ||

| Loss on Sale of Investments | 5,560 | ||||

| Investments–Company W Stock | 104,260 | ||||

| (To record sale of shares) | |||||

Table (3)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Loss on Sale of Investments is a loss or expense account. Since losses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Investments–Company W Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

Prepare journal entry for the dividend received from Company W shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2016 | |||||

| June | 30 | Cash | 840 | ||

| Dividend Revenue | 840 | ||||

| (To record receipt of dividend revenue) | |||||

Table (4)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company W’s stock.

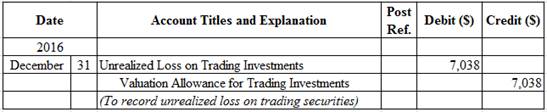

Prepare

Figure (1)

- Unrealized Loss on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since loss has occurred and losses reduce stockholders’ equity value, and a decrease in stockholders’ equity value is debited.

- Valuation Allowance for Trading Investments is a contra-asset account. The account is credited because the market price was decreased (loss) to $179,400 from the cost of $136,438.

Working Notes:

Compute the unrealized gain (loss) as on December 31, 2016.

Step 1: Compute the fair value of the portfolio of the trading investment.

| Security | Number of Shares | Fair Market Value | = | Fair Market Value of Investment | |

| Company W | 2,400 shares | $38 | = | $91,200 | |

| Company M | 1,800 shares | 49 | = | 88,200 | |

| Total | $179,400 | ||||

Table (5)

Step 2: Compute the cost per share of Company W.

Step 3: Compute the cost per share of Company M.

Step 4: Compute the cost of the portfolio of the trading investment, as on December 31.

| Security | Number of Shares | Cost per Share | = | Cost of Investment | |

| Company W | 2,400 shares | $40.10 | = | $96,240 | |

| Company M | 1,800 shares | 50.11 | = | 90,198 | |

| Total | $186,438 | ||||

Table (6)

Note: Refer to Steps 3 and 4 for cost per share of Company W and Company M.

Step 5: Compute the unrealized gain (loss) as on December 31, 2016.

| Details | Amount ($) |

| Trading investments at fair value, December 31 (From Table-5) | $179,400 |

| Less: Trading investments at cost, December 31 (From Table-6) | (186,438) |

| Unrealized loss on trading investments | $(7,038) |

Table (7)

Prepare journal entry for the purchase of 3,500 shares of Company D, at $30 per share, and a brokerage commission of $175.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| April | 4 | Investments–Company D Stock | 105,715 | ||

| Cash | 105,715 | ||||

| (To record purchase of shares for cash) | |||||

Table (8)

- Investments–Company D Stock is an asset account. Since stock investments are purchased, asset value increased, and an increase in asset is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Working Notes:

Compute amount of cash paid to purchase Company D’s stock.

Prepare journal entry for the dividend received from Company W shares.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| June | 28 | Cash | 960 | ||

| Dividend Revenue | 960 | ||||

| (To record receipt of dividend revenue) | |||||

Table (9)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Dividend Revenue is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

Working Notes:

Compute amount of dividend received on Company W’s stock.

Prepare journal entry for sale of 700 shares of Company D at $32, with a brokerage of $50.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | |

| 2017 | |||||

| September | 9 | Cash | 22,350 | ||

| Gain on Sale of Investments | 1,315 | ||||

| Investments–Company D Stock | 21,035 | ||||

| (To record sale of shares) | |||||

Table (10)

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Gain on Sale of Investments is a revenue account. Since revenues increase equity, equity value is increased, and an increase in equity is credited.

- Investments–Company D Stock is an asset account. Since stock investments are sold, asset value decreased, and a decrease in asset is credited.

Working Notes:

Calculate the realized gain (loss) on sale of stock.

Step 1: Compute cash received from sale proceeds.

Step 2: Compute cost of stock investment sold.

Step 3: Compute realized gain (loss) on sale of stock.

Note: Refer to Steps 1 and 2 for value and computation of cash received and cost of stock investment sold.

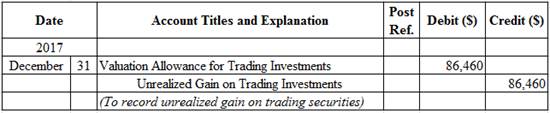

Prepare adjusting entry for valuation of trading securities transaction.

Figure (2)

- Valuation Allowance for Trading Investments is a contra-asset account. The account is debited because the market price was increased (gain).

- Unrealized Gain on Trading Investments is an adjustment account used to report gain or loss on adjusting cost of investment at fair market value. Since gain has occurred and gains increase stockholders’ equity value, and an increase in stockholders’ equity value is credited.

Working Notes:

Compute the unrealized gain (loss) as on December 31, 2017.

| Details | Amount ($) |

| Unrealized gain as on December 31, 2017 | $79,422 |

| Add: Unrealized loss as on December 31, 2016 (From Table-8) | 7,038 |

| Unrealized gain on trading investments | $86,460 |

Table (11)

(2)

To indicate: The presentation of trading investments on the current assets section of the balance sheet

(2)

Explanation of Solution

Balance sheet presentation:

| Company S | ||

| Balance Sheet (Partial) | ||

| December 31, 2017 | ||

| Assets | ||

| Current assets: | ||

| Trading investments (at cost) | $270,578 | |

| Add valuation allowance for trading investments | 79,422 | |

| Trading investments (at fair value) | $350,000 | |

Table (12)

(3)

To discuss: The reporting of trading investments on the financial statements

(3)

Explanation of Solution

Unrealized gain or loss is the result of change in trading investments cost and fair values, and reported as Other Revenues (Losses) on the income statement. The unrealized gain will be added to the net income and unrealized loss will be deducted from the net income. In 2016, Company S would report $7,038 of unrealized loss as Other Losses on the income statement. In 2017, Company S would report $86,460 of unrealized gain as Other Income on the income statement

Want to see more full solutions like this?

Chapter 13 Solutions

CENGAGENOWV2 FOR WARREN'S FINANCIAL & M

- Trading Securities Pear Investments began operations in 2020 and invests in securities classified as trading securities. During 2020, it entered into the following trading security transactions: Purchased 20,000 shares of ABC common stock at $38 per share Purchased 32,000 shares of XYZ common stock at $17 per share At December 31, 2020, ABC common stock was trading at $39.50 per share and XYZ common stock was trading at $16.50 per share. Required: 1. Prepare the necessary adjusting entry to value the trading securities at fair market value. 2. CONCEPTUAL CONNECTION What is the income statement effect of this adjusting entry?arrow_forwardJournalizing equity investment transactions; fair value method Seamus Industries Inc. buys and sells investments as part of its ongoing cash management. The following investment transactions were completed during the year: Feb. 24. Purchased 1,000 shares of Tett Co.'s common stock for $85 per share. May 16. Purchased 2,500 shares of Isaacson Co.'s common stock for $35. July 14. Sold 400 shares of Tett Co. stock for $102 per share. Aug. 12. Sold 750 shares of Isaacson Co. stock for $32 per share. Oct. 31. Received dividends of $0.40 per share on Tett Co. stock. Dec. 31. At the end of the accounting period, the fair value of the remaining 600 shares of Tett Co.'s stock was $110 per share. The fair value of the remaining 1,750 shares of Isaacson Co.'s stock was $30 per share. Journalize the entries for these transactions. If an amount box does not require an entry, leave it blank. Feb. 24 May 16 July 14 Aug. 12 Oct. 31 Dec. 31arrow_forwardQuestion Content Area On April 1, 2017 the Reba Company purchased 10%, $800,000 bonds of the Trading Up Company at par plus accrued interest. These bonds were classified as an investment in trading securities. The bonds pay interest on June 30 and December 31 each year. The entry by Reba on April 1, 2017, would include a debit to Investment in Trading Securities of $820,000 debit to Interest Expense of $20,000 credit to Interest Income of $20,000 credit to Cash of $820,000arrow_forward

- Classifying Investments in Securities Match each security listed below with its usual classification: (1) trading securities, (2) available-for-sale securities, (3) equity method securities, (4) held-to-maturity securities, or (5) equity securities measured at FV-NI. a. Abbot common stock, no-par; acquired to use temporarily idle cash with intent to sell next month. b. 30% interest in Packaging Inc.; acquired to drive costs down through vertical integration. c. Mack stock held in trading account. d. Hasten Inc.'s 10-year bonds acquired. Hasten intends to hold to maturity, but may need to sell the bonds earlier for cash. e. Staufer common stock, par $5; acquired to gain a significant influence, but not control. f. Frazer bonds, 9% mature at the end of 10 years; acquired with the intent and ability to hold for 10 years. g. Foreign Corp. common stock; a 30% interest acquired, but difficulties encountered in an attempt to obtain representation on the Foreign…arrow_forwardStock investment transactions, equity method and available-for-sale securitiesForte Inc. produces and sells theater set designs and costumes. The company beganoperations on January 1, Year 1. The following transactions relate to securitiesacquired by Forte Inc., which has a fiscal year ending on December 31:Year1Jan.22.Purchased 22,000 shares of Sankal Inc. as an available-for-sale security at $18per share, including the brokerage commission.Mar.8.Received a cash dividend of $0.22 per share on Sankal Inc. stock.Sept.8.A cash dividend of $0.25 per share was received on the Sankal stock.Oct.17.Sold 3,000 shares of Sankal Inc. stock at $16 per share less a brokeragecommission of $75.Dec.31.Sankal Inc. is classified as an available-for-sale investment and is adjusted toa fair value of $25 per share. Use the valuation allowance for available-forsale investments account in making the adjustment.Year2Jan.10.Purchased an influential interest in Imboden Inc. for $720,000 by purchasing96,000…arrow_forwardAssessing Financial Statement Effects of Trading and Available-for-Sale Securities Use the financial statement effects template to record the following four transactions involving investments in marketable securities. Purchased 6,000 common shares of Liu, Inc., at $12.25 cash per share. Received a cash dividend of $1.50 per common share from Liu. Year-end market price of Liu common stock is $11.25 per share. Sold all 6,000 common shares of Liu for $66,300. Use negative signs with answers, when appropriate. Balance Sheet Transaction Cash Asset + Noncash Assets = Liabilities + Contributed Capital + Earned Capital (1) Answer Answer Answer Answer Answer (2) Answer Answer Answer Answer Answer (3) Answer Answer Answer Answer Answer (4) Answer Answer Answer Answer Answer Income Statement Revenue - Expenses = Net Income Answer Answer Answer Answer Answer Answerarrow_forward

- Problem 1 about Trading Securities Bank National investment manager invests some of its financial resources in securities trading. During the last quarter of 2018, the following transactions took place in connection with trading securities. Nov. 5. Buy 200 shares of M Company's ordinary shares for $ 86 per share.Nov 19. Buy 300 shares of Company P preferred stock at $ 63 per share.Dec 29 Sold 100 shares of Company M's ordinary shares for $ 89 per share.Dec. 15. Buy 400 shares of T Company common stock for $ 37 per shareDec 17 Company P shares are sold at preference shares at $ 62 per share As of December 31, 2010, the stock market value was as follows:M, $ 87 per share;P, $ 61 per share; andT, $ 37.25 per share.The bank did not have any trading effects at the beginning of the last quarter of 2010. Requested:1. Prepare a journal entry to record the information.2. Show what the bank reported in the 2010 fourth quarter profit and loss statement for these trading securities.3. Show how the…arrow_forwardJournal entries for trading investments Gruden Bancorp Inc. purchased a portfolio of trading securities during 20Y3, its first year of operations. The cost and fair value of this portfolio on December 31, 20Y3, are as follows: Issuing Company Cost Fair Value Griffin Inc. $14,070 $13,230 Luck Company 22,960 21,350 Wilson Company 9,300 9,490 Total $46,330 $44,070 On May 10, 20Y4, Gruden Bancorp Inc. purchased trading securities of Carroll Inc. for $15,610. Journalize the entries to record the following: If an amount box does not require an entry, leave it blank. a. The adjusting entry for the portfolio of trading securities on December 31, 20Y3. 20Y3, Dec. 31 b. The May 10, 20Y4, purchase of Carroll Inc. securities. 20Y4, May 10 c. The adjusting entry for the portfolio of trading securities on December 31, 20Y4. Assume that except for the purchase of Carroll Inc. securities there were no other transactions involving trading securities in 20Y4. In addition, assume that the fair value of…arrow_forwardRecording Stock Issue Costs Stellar Inc. issued 48,000 shares of common stock, $0.01 par value, for $28 per share on March 28, 2020. Related to this transaction, Stellar incurred legal and administrative costs totaling $9,600, paid in cash. Required Prepare the journal entry on March 28, 2020, for the issuance of common shares. Note: List multiple debits (when applicable) in alphabetical order and list multiple credits (when applicable) in alphabetical order. Date Account Name Dr. Cr. March 28, 2020arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning