Videos

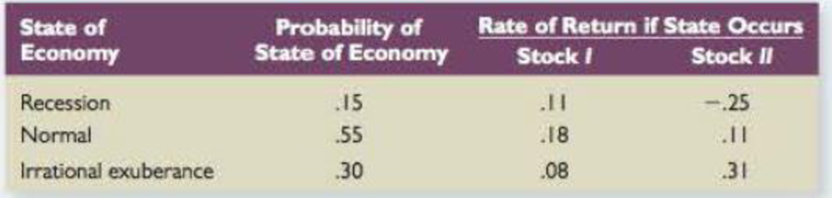

Systematic versus Unsystematic Risk Consider the following information about Stocks I and II:

The market risk premium is 7.5 percent, and the risk-free rate is 4 percent. Which stock has the most systematic risk? Which one has the most unsystematic risk? Which stock is “riskier”? Explain.

To determine: The Stock which has more systematic risk, unsystematic risk and stock which is riskier.

Introduction: Systematic Risk is acknowledged as non diversifiable risks or market risk. Such category of risk is not intended to be separated by distinguishing assets. Systematic risk leads on how a particular investment in a distinguished portfolio that support financially to the total or aggregate risk of a business's financial funding.

Unsystematic Risk is acknowledged as diversifiable or residual or particular risk. The proportion of a corporation’s total or aggregate risk which can be barred by holding such risks in a distinguished or as diversified asset portfolio.

Answer to Problem 33QP

Stock I have more systematic risk, Stock II has more unsystematic risk and Stock I is riskier.

Explanation of Solution

Determine the Expected Return for Stock I

Therefore the Expected Return for Stock I is 13.95%

Determine the Beta for Stock I

Using CAPM formula we calculate the beta for Stock I as,

Therefore the Beta for Stock I is 1.33

Determine the Variance for Stock I

Therefore the Variance for Stock I is 0.002095

Determine the Standard Deviation for Stock I

Therefore the Standard Deviation for Stock I is 4.58%

Determine the Expected Return for Stock II

Therefore the Expected Return for Stock II is 11.60%

Determine the Beta for Stock II

Using CAPM formula we calculate the beta for Stock II as,

Therefore the Beta for Stock II is 1.01

Determine the Variance for Stock II

Therefore the Variance for Stock II is 0.031404

Determine the Standard Deviation for Stock II

Therefore the Standard Deviation for Stock II is 17.72%

- Stock I have less systematic risk than Stock II since the beta of Stock II is lesser than Stock I and Stock II is said to have more total risk.

- Hence Stock I have more systematic risk and Stock II have more unsystematic risk and greater total risk.

- Stock I is riskier because unsystematic risk can be diversified due to lack of volatility in the stock return.

- Additionally Stock I have higher expected return and higher risk premium.

Want to see more full solutions like this?

Chapter 11 Solutions

UPENN: LOOSE LEAF CORP.FIN W/CONNECT

- 1. Calculate the Expected Return, Standard Deviation, and Beta for each stock. 2. Which stock has more systematic risk and which one has more unsystematic risk? Which stock is "riskier"? Explain your answer completely. Use excel to show formulas and calculationsarrow_forwardWhich of the following stocks have the highest systematic risk? A. A stock with a high correlation to the market and a low return volatility. B. A stock with a low correlation to the market and a high return volatility. C. A stock with a high correlation to the market and high return volatility. D. A stock with a low correlation to the market and a low return volatility.arrow_forwardThe standard deviation of a stock’s return is a measure of its? Multiple Choice systematic risk correlation expected future return total riskarrow_forward

- The table below contains the covariance matrix of stock returns and the market. Assume that the assumptions of CAPM hold. 1. Find the market risk. 2. Find the systematic risk of BlueChip.arrow_forwardA stock's risk premium is equal to the: expected market risk premium times beta. expected market risk premium multiplied by beta plus the risk-free return. Risk-free return plus expected market return. expected market return times beta.arrow_forward: What is risk and how is it measured? How is risk measured in a portfolio compared to risk in a stand-alone stock? How do you measure the relevant risk in a portfolio?arrow_forward

- When working with the CAPM, which of the following factors can be determined with the most precision? a. The beta coefficient of "the market," which is the same as the beta of an average stock. b. The beta coefficient, bi, of a relatively safe stock. c. The market risk premium (RPM). d. The most appropriate risk-free rate, rRF. e. The expected rate of return on the market, rM.arrow_forwardThe additional return over the risk-free rate needed to compensate investors for assuming an average amount of risk. a. Market Risk Premium b. Risk-free rate С. Stock's beta O d. Security Market Line e. Required Return on Stockarrow_forwarda) The covariance between stocks A and B is 0.0014, standard deviation of stock A is 0.032, and standard deviation of stock B is 0.044. Which of the following is the most appropriate to depict the risk- return characteristics of a portfolio consisting of only stocks A and B, and explain why? E(R) E(R) E(R) A A A (A) (B) (C) b) found to be half of the required return (Rs) on stock B. The risk-free rate (R) is one-fourth of the required Assume that using the Security Market Line (SML) the required rate of return (RA) on stock A is return on A. Return on market portfolio is denoted by RM. Find the ratio of beta of A (DA) to beta of B (OB). c) Assume that the short-term risk-free rate is 3%, the market index S&P500 is expected to pay returns of 15% with the standard deviation equal to 20%. Asset A pays on average 5%, has standard deviation equal to 20% and is NOT correlated with the S&P500. Asset B pays on average 8%, also has standard deviation equal to 20% and has correlation of 0.5 with…arrow_forward

- Fundamental analysis is a method of______________________________to determine intrinsic value of the stock.a. Measuring the intrinsic value of a security using the market indexb. Using qualitative and quantitative factorsc. Using statistical analysis such as standard deviation, coefficients and probabilitiesd. Using historical price movementse. B and C onlyarrow_forwardExercises: a. The standard deviation of returns is 0.30 for Stock A and 0.20 for Stock B. The covariance between the returns of A and B is 0.006. The correlation of returns between A and B is: b. Explain the differences between systemic risk and unsystematic risk, give additional examples c. Compare and contrast the Capital Market Line and Security Market Line d. The covariance of the market's returns with the stock's returns is 0.008. The standard deviation of the market's returns is 0.08, and the standard deviation of the stock's returns is 0. 11. What is the correlation coefficient of the returns of the stock and the returns of the market? e. According to the CAPM, what is the required rate of return for a stock with a beta of 0.7, when the risk-free rate is 7% and the expected market rate of return is 14%arrow_forwardWhen working with the CAPM, which of the following factors can be determined with the most precision? a. The most appropriate risk-free rate, rRF. b. The market risk premium (RPM). c. The beta coefficient, bi, of a relatively safe stock. d. The expected rate of return on the market, rM. e. The beta coefficient of "the market," which is the same as the beta of an average stock.arrow_forward

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning