Corporate Finance

12th Edition

ISBN: 9781259918940

Author: Ross, Stephen A.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 11, Problem 23QAP

Analyzing a Portfolio You want to create a portfolio equally as risky as the market and you have

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

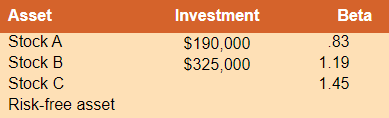

You want to create a portfolio equally as risky as the market, and you have $5M to invest. Given the

information below, what is your investment in the risk-free asset?

Asset

Stock A

Stock B

Stock C

Risk-free Asset

$0.8M

$0.7M

$0.9M

$1.1M

Investment

$1M

$2M

Beta

0.7

1.25

1.5

You are going to invest $50,000 in a portfolio consisting of assets X, Y, and Z, as follows;

What is the expected return of this portfolio?

Calculate the beta coefficient of the portfolio

You want your portfolio beta to be 1.30. Currently, your portfolio consists of $100 invested in stock A with a beta of 1.4 and $300 in stock B with a beta of .6. You have another $400 to invest and want to divide it between an asset with a beta of 1.8 and a risk-free asset. How much should you invest in the risk-free asset?

Chapter 11 Solutions

Corporate Finance

Ch. 11 - Diversifiable and Nondiversifiable Risks In broad...Ch. 11 - Systematic versus Unsystematic Risk Classify the...Ch. 11 - Expected Portfolio Returns If a portfolio has a...Ch. 11 - Diversification True or false: The most important...Ch. 11 - Portfolio Risk If a portfolio has a positive...Ch. 11 - Beta and CAPM Is it possible that a risky asset...Ch. 11 - Covariance Briefly explain why the covariance of a...Ch. 11 - Prob. 8CQCh. 11 - Prob. 9CQCh. 11 - Prob. 10CQ

Ch. 11 - Determining Portfolio Weights What are the...Ch. 11 - Portfolio Expected Return You own a portfolio that...Ch. 11 - Prob. 3QAPCh. 11 - Portfolio Expected Return You have 10,000 to...Ch. 11 - Prob. 5QAPCh. 11 - Prob. 6QAPCh. 11 - Calculating Expected Returns A portfolio is...Ch. 11 - Returns and Standard Deviations Consider the...Ch. 11 - Returns and Standard Deviations Consider the...Ch. 11 - Calculating Portfolio Betas You own a stock...Ch. 11 - Calculating Portfolio Betas You own a portfolio...Ch. 11 - Using CAPM A stock has a beta of 1.15, the...Ch. 11 - Prob. 13QAPCh. 11 - Prob. 14QAPCh. 11 - Prob. 15QAPCh. 11 - Using CAPM A stock has a beta of 1.08 and an...Ch. 11 - Prob. 17QAPCh. 11 - Reward-to-Risk Ratios Stock Y has a beta of 1.15...Ch. 11 - Prob. 19QAPCh. 11 - Portfolio Returns Using information from the...Ch. 11 - Prob. 21QAPCh. 11 - Prob. 22QAPCh. 11 - Analyzing a Portfolio You want to create a...Ch. 11 - Prob. 24QAPCh. 11 - Prob. 25QAPCh. 11 - Prob. 26QAPCh. 11 - Prob. 27QAPCh. 11 - Prob. 28QAPCh. 11 - Prob. 29QAPCh. 11 - Prob. 30QAPCh. 11 - Prob. 31QAPCh. 11 - Prob. 32QAPCh. 11 - Prob. 33QAPCh. 11 - Prob. 34QAPCh. 11 - Prob. 35QAPCh. 11 - Prob. 36QAPCh. 11 - Prob. 37QAPCh. 11 - Prob. 38QAPCh. 11 - Prob. 1MCCh. 11 - Prob. 2MC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Write out the equation for the Capital Market Line (CML), and draw it on the graph. Interpret the plotted CML. Now add a set of indifference curves and illustrate how an investors optimal portfolio is some combination of the risky portfolio and the risk-free asset. What is the composition of the risky portfolio?arrow_forwardYou want to create a portfolio equally as risky as the market, and you have $1,200,000 to invest. Consider the following information: Asset Stock A Stock B Stock C Risk-free asset What is the investment in Stock C? Investment Investment $300,000 $ 240,000 Investment Beta 0.70 1.10 1.50 What is the investment in risk-free asset?arrow_forwardYou want to create a portfolio equally as risky as the market, and you have $250,000 to invest. Given this information, fill in the three missing pieces of information in the following table. Show your calculations: Investment Betal 0.90 Asset Stock A $50,000 Stock B $70,000 Stock C Risk-Free Asset 1.25 1.60arrow_forward

- You can invest in a portfolio of two assets: the riskfree asset with rate of return 6%, and a risky portfolio with expcected return 16% and stdev 30%. You optimally choose to invest equal amount in both assets. What is your risk aversion (keep 2 decimal places)? A=arrow_forwardYou want to create a portfolio equally as risky as the market, and you have $500,000 to invest. Information about the possible investments is given below: Asset Investment Beta Stock A $ 147,000 .92 Stock B $ 133,000 1.37 Stock C 1.52 Risk - free asset How much will you invest in Stock C? How much will you invest in the risk - free asset? Note: Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16.arrow_forwardYou are evaluating various investment opportunities currently available and you have the fol-lowing information about five different well-diversified portfolios of risky assets. Interest raterf = 3% a) Calculate the Sharpe ratio for each portfolio. (b) Explain which of these five portfolios is most likely to be the optimal risky portfolio. (c) Suppose you are willing to invest with an expected return of 6%. What would be theinvestment proportions in the riskless asset and the optimal risky portfolio? What is thestandard deviation of the return for this investment?arrow_forward

- You have just invested in a portfolio of three stocks. The amount of money that you invested in each stock and its net are summarized below. Calculate the beta of the portfolio and use the capital asset pricing model (CAPM) to compute the expected rate of return for the portfolio. Assume that the expected rate of return on the market is 18% and that the risk-free rate is 6%. Stock A, Investment = $188,000, Beta=1.50, Stock B, Investment = $282,000, Beta =0.50, Stock C, Investment = $470,000, Beta = 1.30 Beta of the portfolio ? Expected rat of return ? %arrow_forwardConsider the following information about a risky portfolio that youmanage, and a risk-free asset: E(rP ) = 11%, σP = 15%, rf = 5%.a) Your client wants to invest a proportion of her total investment budget in your riskyfund to provide an expected rate of return on her overall or complete portfolio equal to8%. What proportion should she invest in the risky portfolio, P, and what proportionin the risk-free asset? b) What will be the standard deviation of the rate of return on her portfolio? c) Another client wants the highest return possible subject to the constraint that you limithis standard deviation to be no more than 12%. Which client is more risk averse?arrow_forwardYou are going to invest $20,000 in a portfolio consisting of assets X, Y, and Z, as follows: Asset Annual Return Probability Beta Proportion X 10% 0.50 1.2 0.333 Y 8% 0.25 1.6 0.333 Z 16% 0.25 2.0 0.333 Given the information in Table 5.2, The beta of the portfolio in Table 8.2, containing assets X, Y, and Z is ________. Select one: a. 1.6 b. 2.0 c. 1.5 d. 2.4arrow_forward

- Assuming you are an investor with GHS100 available. If you invest GHS60 and GHS40 in Allos Inc. and Orangus Inc. respectively, what will be your portfolio returns? 4.Calculate the Standard deviation of the portfolio.arrow_forwardAssume the betas for securities A, B, and C are as shown here. (Click on the icon here in order to copy its contents of the data table below into a spreadsheet.) Security Beta A 1.58 B 0.65 C −0.23 If you have a portfolio with $30,000 invested in each of Investment A, B, and C, what is your portfolio beta?arrow_forwardYou want to create a portfolio equally as risky as the market, and you have $500,000 to invest. Information about the possible investments is given below: Asset Stock A Stock B Stock C Risk-free asset Investment, $ 141,000 $ 139,000 Beta .86 1.31 1.46 How much will you invest in Stock C? How much will you invest in the risk-free asset? Note: Do not round intermediate calculations and round your answers to 2 decimal places, e.g., 32.16. Investment in Stock C Investment in risk-free assetarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

Investing For Beginners (Stock Market); Author: Daniel Pronk;https://www.youtube.com/watch?v=6Jkdpgc407M;License: Standard Youtube License