The correct option for given situation.

Answer to Problem 15MCQ

Option a is correct.

Explanation of Solution

Explanation for correct option:

a.

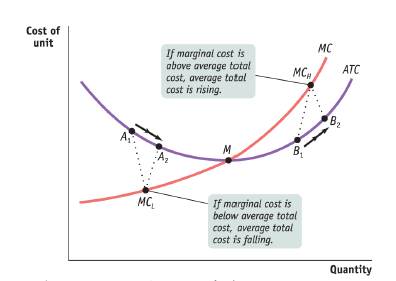

There is an inverse relationship between the marginal cost and the marginal product. This is because as the production level increases per unit cost of product reduces. If labor is utilized up to its maximum specialization level then the marginal cost is reduced. At this point marginal product is maximum. If there is only one variable input than the cost of producing an additional unit will be less as compared to increase in the output level. Therefore, option a is correct.

Explanation for incorrect options:

b.

If marginal product is maximum then it is not necessary that the average product will be maximum at minimum marginal cost. Therefore, option b is incorrect.

c.

As explained in the correct option, there is an inverse relationship between the marginal cost and marginal product. When marginal cost is minimum then marginal product is not minimum instead it is at its maximum level. Therefore, option c is incorrect.

d.

When marginal cost reaches its minimum level then average cost is declining and there is an inverse relationship between average cost and average product. It means that at minimum marginal cost, average product does not reach its maximum level. Therefore, option d is incorrect.

e.

When marginal cost reaches its minimum level then average cost is declining and there is an inverse relationship between average cost and average product. Therefore, option e is incorrect.

Marginal cost: Marginal cost refers to the cost of production which is incurred by the firm if one additional unit is produced. In other words, marginal cost is the cost incurred by the firm for producing an additional unit.

Chapter 10R Solutions

Krugman's Economics For The Ap® Course

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education