Concept explainers

Videos

Activity-Based Costing of Suppliers

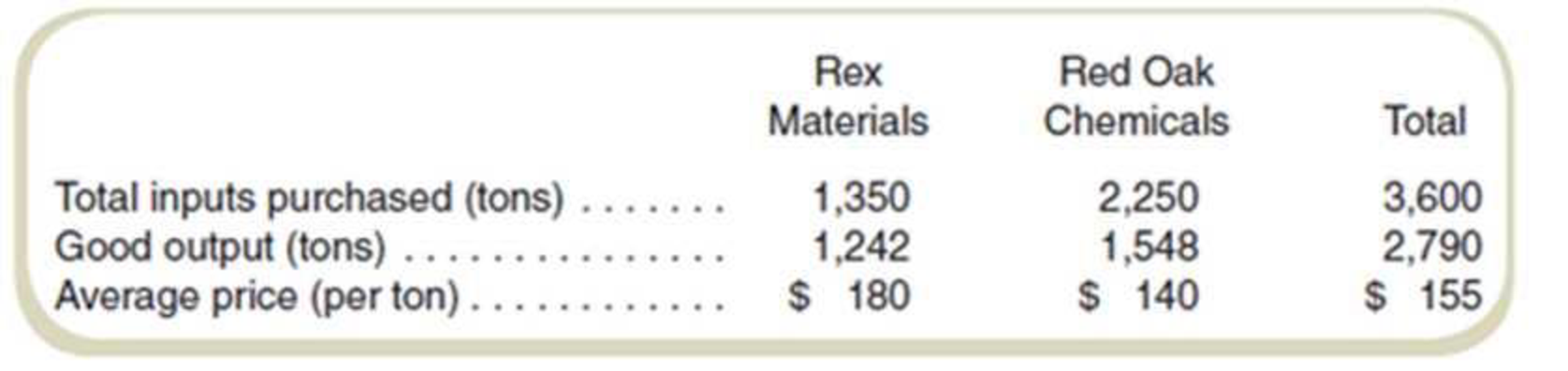

JFI Foods produces processed foods. Its basic ingredient is a feedstock that is mixed with other ingredients to produce the final packaged product. JFI purchases the feedstock from two suppliers, Rex Materials and Red Oak Chemicals. The quality of the final product depends directly on the quality of the feedstock. If the feedstock is not correct, JFI has to dispose of the entire batch. All feedstock in this business is occasionally “bad.” so JFI measures what it calls the “yield,” which is measured as

Yield = Good output ÷ Input

where the output and inputs are both measured in tons. As a benchmark. JFI expects to get 8 tons of good output for every 10 tons of feedstock purchased for a yield of 80 percent (= 8 tons of output ÷ 10 tons of feedstock).

Data on the two suppliers for the past year follow:

Required

Assume that the average quality, measured by the yield, and prices from the two companies will continue as in the past. What is the effective price for feedstock from the two companies when quality is considered?

Want to see the full answer?

Check out a sample textbook solution

Chapter 10 Solutions

GEN COMBO FUNDAMENTALS OF COST ACCOUNTING; CONNECT 1S ACCESS CARD

- Activity-Based Supplier Costing Clear sound uses Alpha Electronics and La Paz Company to buy two electronic components used in the manufacture of its cell phones: Component 125X and Component 30Y. Consider two activities: testing components and reordering components. After the two components are inserted, testing is done to ensure that the two components in the phones are working properly. Reordering occurs because one or both of the components have failed the test and it is necessary to replenish component inventories. Activity cost information and other data needed for supplier costing are as follows: I. Activity Costs Caused by Suppliers (testing failures and reordering as a result) Activity Costs Testing components $1,200,000 Reordering components 300,000 II. Supplier Data Alpha Electronics La Paz Company 125X 30Y 125X 30Y Unit purchase price $10 $26 $12 $28 Units purchased 120,000 68,100 15,000 15,000 Failed…arrow_forwardProducts versus Services, Cost Assignment Holmes Company produces wooden playhouses. When a customer orders a playhouse, it is delivered in pieces with detailed instructions on how to put it together. Some customers prefer that Holmes put the playhouse together. Therefore, these customers purchase the playhouse, as well as pay an additional fee for Holmes to install the playhouse. Holmes then pulls two workers off the production line and sends them to construct the playhouse on site. Required: 1. What two products does Holmes sell? Classify each one as a product or a service. 2. CONCEPTUAL CONNECTION Do you think Holmes assigns costs individually to each product or service? Why or why not? 3. CONCEPTUAL CONNECTION Describe the opportunity cost of the installation process.arrow_forwardThe Chocolate Baker specializes in chocolate baked goods. The firm has long assessed the profitability of a product line by comparing revenues to the cost of goods sold. However, Barry White, the firms new accountant, wants to use an activity-based costing system that takes into consideration the cost of the delivery person. Following are activity and cost information relating to two of Chocolate Bakers major products: Using activity-based costing, which of the following statements is correct? a. The muffins are 2,000 more profitable. b. The cheesecakes are 75 more profitable. c. The muffins are 1,925 more profitable. d. The muffins have a higher profitability as a percentage of sales and, therefore, are more advantageous.arrow_forward

- Southward Company has implemented a JIT flexible manufacturing system. John Richins, controller of the company, has decided to reduce the accounting requirements given the expectation of lower inventories. For one thing, he has decided to treat direct labor cost as a part of overhead and to discontinue the detailed direct labor accounting of the past. The company has created two manufacturing cells, each capable of producing a family of products: the radiator cell and the water pump cell. The output of both cells is sold to a sister division and to customers who use the radiators and water pumps for repair activity. Product-level overhead costs outside the cells are assigned to each cell using appropriate drivers. Facility-level costs are allocated to each cell on the basis of square footage. The budgeted direct labor and overhead costs are as follows: The predetermined conversion cost rate is based on available production hours in each cell. The radiator cell has 45,000 hours available for production, and the water pump cell has 27,000 hours. Conversion costs are applied to the units produced by multiplying the conversion rate by the actual time required to produce the units. The radiator cell produced 81,000 units, taking 0.5 hour to produce one unit of product (on average). The water pump cell produced 90,000 units, taking 0.25 hour to produce one unit of product (on average). Other actual results for the year are as follows: All units produced were sold. Any conversion cost variance is closed to Cost of Goods Sold. Required: 1. Calculate the predetermined conversion cost rates for each cell. 2. Prepare journal entries using backflush accounting. Assume two trigger points, with completion of goods as the second trigger point. 3. Repeat Requirement 2, assuming that the second trigger point is the sale of the goods. 4. Explain why there is no need to have a work-in-process inventory account. 5. Two variants of backflush costing were presented in which each used two trigger points, with the second trigger point differing. Suppose that the only trigger point for recognizing manufacturing costs occurs when the goods are sold. How would the entries be listed here? When would this backflush variant be considered appropriate?arrow_forwardActivity-Based Supplier Costing Clearsound uses Alpha Electronics and La Paz Company to buy two electronic components used in the manufacture of its cell phones: Component 125X and Component 30Y. Consider two activities: testing components and reordering components. After the two components are inserted, testing is done to ensure that the two components in the phones are working properly. Reordering occurs because one or both of the components have failed the test and it is necessary to replenish component inventories. Activity cost information and other data needed for supplier costing are as follows: I. Activity Costs Caused by Suppliers (testing failures and reordering as a result) Activity Costs Testing components $1,200,000 Reordering components 300,000 II. Supplier Data Alpha Electronics La Paz Company 125X 30Y 125X 30Y Unit purchase price $10 $26 $12 $28 Units purchased 120,000 80,300 15,000 15,000 Failed tests 1,300 780 10 10 Number of reorders 60 40 Required: Determine the…arrow_forwardActivity-Based Supplier Costing Clearsound uses Alpha Electronics and La Paz Company to buy two electronic components used in the manufacture of its cell phones: Component 125X and Component 30Y. Consider two activities: testing components and reordering components. After the two components are inserted, testing is done to ensure that the two components in the phones are working properly. Reordering occurs because one or both of the components have failed the test and it is necessary to replenish component inventories. Activity cost information and other data needed for supplier costing are as follows: I. Activity Costs Caused by Suppliers (testing failures and reordering as a result) Activity Costs Testing components $1,200,000 Reordering components 300,000 II. Supplier Data Alpha Electronics La Paz Company 125X 30Y 125X 30Y Unit purchase price $10 $26 $12 $28 Units purchased 120,000 60,000 15,000 15,000 Failed…arrow_forward

- Activity-Based Supplier Costing Clearsound uses Alpha Electronics and La Paz company to buy two electronic components used in the manufacture of its cell phones: Component 125X and component 30Y. Consider two activities: Testing components and reordering components. After the two components are inserted, Testing is done to ensure that the two components in the phones are working properly. Reordering occurs because one or both of the components have failed the test and it is necessary to replenish component inventories. Acitivity cost information and other data needed for supplier costing are as follows: 1. Activity costs caused by suppliers(testing failures and reordering as a result) Required : Determine the cost of each supplier by using ABC. Round Unit costs to two decimal places.arrow_forwardActivity-Based Supplier Costing Clearsound uses Alpha Electronics and La Paz Company to buy two electronic components used in the manufacture of its cell phones: Component 125X and Component 30Y. Consider two activities: testing components and reordering components. After the two components are inserted, testing is done to ensure that the two components in the phones are working properly. Reordering occurs because one or both of the components have failed the test and it is necessary to replenish component inventories. Activity cost information and other data needed for supplier costing are as follows: I. Activity Costs Caused by Suppliers (testing failures and reordering as a result) Activity Costs Testing components $1,200,000 Reordering components 300,000 II. Supplier Data Alpha Electronics La Paz Company 125X 30Y 125X 30Y Unit purchase price $10 $26 $12 $28 Units purchased 120,000 77,800 15,000 15,000 Failed tests…arrow_forwardRedwood Company sells craft kits and supplies to retail outlets and through its catalog. Some of the items are manufactured by Redwood, while others are purchased for resale. For the products it manufactures, the company currently bases its selling prices on a product-costing system that accounts for direct material, direct labor, and the associated overhead costs. In addition to these product costs, Redwood incurs substantial selling costs, and Roger Jackson, controller, has suggested that these selling costs should be included in the product pricing structure.After studying the costs incurred over the past two years for one of its products, skeins of knitting yarn, Jackson has selected four categories of selling costs and chosen cost drivers for each of these costs. The selling costs actually incurred during the past year and the cost drivers are as follows: Cost Category Amount Cost Driver Sales commissions $ 829,500 Boxes of yarn sold to retail stores Catalogs 313,000…arrow_forward

- Redwood Company sells craft kits and supplies to retail outlets and through its catalog. Some of the items are manufactured by Redwood, while others are purchased for resale. For the products it manufactures,the company currently bases its selling prices on a product-costing system that accounts for direct material, direct labor, and the associated overhead costs. In addition to these product costs, Redwood incurs substantial selling costs, and Roger Jackson, controller, has suggested that these selling costs should be included in the product pricing structure. Required:1. Prepare a schedule showing Redwood Company’s total selling cost for each order size and the perskein selling cost within each order size.2. Explain how the analysis of the selling costs for skeins of knitting yarn is likely to impact future pricing and product decisions at Redwood Company.arrow_forwardDetermining cost relationships Midstate Containers Inc. manufactures cans for the canned food industry. The operations manager of a can manufacturing operation wants to conduct a cost study investigating the relationship of tin content in the material (can stock) to the energy cost for enameling the cans. The enameling was necessary to prepare the cans for labeling. A higher percentage of tin content in the can stock increases the cost of material. The operations manager believed that a higher tin content in the can stock would reduce the amount of energy used in enameling. During the analysis period, the amount of tin content in the steel can stock was increased for every month, from April to September. The following operating reports were available from the controller: April May June July August September Materials $14,000 $34,800 $33,000 $21,700 $28,800 $33,000 Energy 13,000 28,800 24,200 14,000 17,100 16,000…arrow_forwardHomework i s w Asbury Coffee Enterprises (ACE) manufactures two models of coffee grinders: Personal and Commercial. The Personal grinders have a smaller capacity and are less durable than the Commercial grinders. ACE only recently began producing the Commercial model. Since the introduction of the new product, profits have been steadily declining, although sales have been increasing. The management at ACE believes that the problem might be in how the accounting system allocates costs to products. Direct materials. Direct labor The current system at ACE allocates manufacturing overhead to products based on direct labor costs. For the most recent year, which is representative, manufacturing overhead totaled $2,023,500 based on production of 30,000 Personal grinders and 10,000 Commercial grinders. Direct costs were as follows: Cost Driver Number of production runs Quality tests performed Shipping orders processed Total overhead here to search CINNAMON Management has determined that…arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning