ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

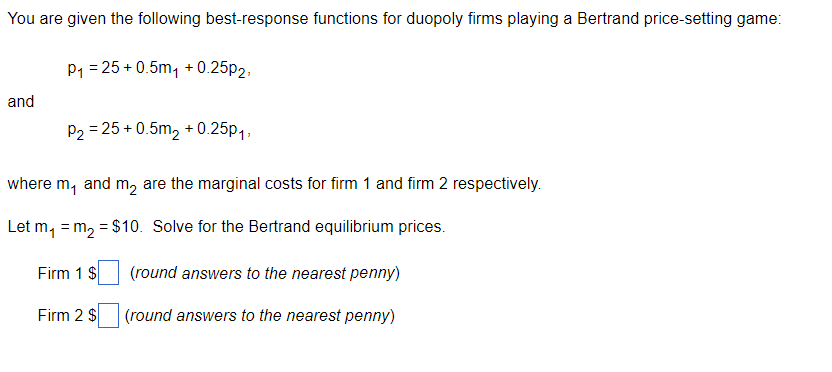

Transcribed Image Text:You are given the following best-response functions for duopoly firms playing a Bertrand price-setting game:

and

P₁ =25+0.5m₁ +0.25p2,

P₂ =25 +0.5m₂ +0.25p₁,

where m, and m₂ are the marginal costs for firm 1 and firm 2 respectively.

Let m₁ = m₂ = $10. Solve for the Bertrand equilibrium prices.

(round answers to the nearest penny)

(round answers to the nearest penny)

Firm 1 $

Firm 2 $

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- A market has the following demand function: 1 P = 120 where Q, Σ0 a) Assuming Cournot-Nash market, fill in the table below when firm one has MC, = 10, firm two has MC, = 20 and firm three has MC, = 20. Additionally, there is no Fixed cost for none of the firms. b) Using data from the table below, explain the merger paradox when firms 2 and 3 merge. How the merged firm (firm 2 and 3) will be worse off? c) How would this outcome differ if all three firms merged? Industry level Output Number of Firm level Firms Price Profits Output Profits 1 3arrow_forwardSuppose two firms, A and B, have a cost function of ?(??) = 30??, for ? = ?, ?. The inverse demand for the market is given by ? = 120 − ?, where Q represents the total quantity in the market, ? = ?? + ??. 1. Solve for the firms’ outputs in a Nash Equilibrium of the Cournot Model. 2. Let Firm A be the first mover, and Firm B be the second mover. Solve for the firms’ outputs in a SPNE of the Stackelberg Model.arrow_forward1. Consider the following Cournot model. The inverse demand function is given by p = 30 –Q, where Q = qi + q2. Firm 1's marginal cost is $6 (c1 = 6). Firm 2 uses a new technology so that its marginal cost is $3 (c2 = 3). There is no fixed cost. The two firms choose their quantities simultaneously and compete only once. (So it’s a one-shot simultaneous game.) Answer the following questions. а. Derive Firm 1 and Firm 2's reaction functions, respectively. b. Solve the Nash equilibrium (qı", q2"). What is the equilibrium price and what is the profit level с. for each firm?arrow_forward

- Two firms produce Bliffs. They compete by simultaneously choosing prices in a single period. The demand for Bliffs is given by P(Q) = 100-2Q where Q is market quantity and P is market price. Firm 1 has costs C1(q1) = 20q1 and Firm 2 has costs C2(q2) = 10q2. Which statement is true? In the Nash equilibrium to the game, both firms play dominated strategies None of the other answers are correct O In the Nash equilibrium to the game, both firms play dominant strategies In the Nash equilibrium to the game, both firms slowly lower prices towards marginal costs O In the Nash equilibrium to the game, both firms set price equal to marginal costarrow_forwardSuppose that identical duopoly firms have constant marginal costs of $20 per unit. Firm 1 faces a 110-2p1 + P2, where q1 is Firm 1's output, p1 is Firm 1's price, and p2 is Firm 2's price. Similarly, the demand Firm 2 faces is 92 110-2p2 + p1. What is Firm 1's profit demand function of 9₁ under the Nash-Bertrand equilibrium, assuming no fixed costs? = =arrow_forwardConsider the following static game with two firms as the players. Each firm must decide either to upgrade (U) an existing good to a new version; or not upgrade it (N). The decisions are simultaneous. If a firm chooses to upgrade, they have to pay a fixed cost of 7. If they don’t upgrade, there is no fixed cost. The marginal cost is always equal to 3. The demand side of the market is as follows: If neither firm upgrades, each firm sells 2 units at price 4. If both firms upgrade, each firm sells 3 units at price 5. If only one firm upgrades, the one who upgrades sells 5 units at price 5, and the other firm does not sell anything.arrow_forward

- There are two firms in a market and they compete in a Nash-Cournot manner. Firm 1 faces the demand function p1(g1,92) = 200 - 91 - 92, and has a total cost function TC1 = (91)2. Firm 2 faces the demand function p2(91,92) = 160 - 92 - 91, and has a total %3D cost function TC2 = (92)2. Answer each of the following questions. a. Find the Nash-Cournot equilibrim output and price v for firm 1. b. Find the Nash-Cournot equilibrim output v and price v for firm 2.arrow_forward2. Four firms (A, B, C, and D) play a pricing game (i.e. Bertrand). Each firm (i) may choose any price Pi from 0 to ¥, with the goal of maximizing its own profit. Firms A and B have MC = 10, while firms C and D have MC = 20. The firms serve a market with the demand curve Q = 100 – P. All firms produce exactly the same product, so consumers purchase only from the firm with the lowest price. If multiple firms have the same low price, consumers divide their quantities evenly among the low-priced firms. Assume the firms choose price simultaneously. a. There are many equilibria in this simultaneous-move pricing game. Provide one equilibrium combination of prices, and argue that no firm has a unilateral incentive to deviate from these prices. Now assume firm A chooses price first. Firm B observes this choice and then chooses its own price second. Firm C chooses price third, and firm D chooses price last. b. Again, there are many equilibria in this sequential-move pricing game.…arrow_forwardI have constructed a Bertrand game (competition in prices) and presented you with the reaction functions of each firm. p1 = 12.5 + p2/4 p2 = 5/2 + p1/2 a) Use excel to draw the reaction functions. b) Solve for the Nash equilibriumarrow_forward

- Consider a Cournot duopoly. The inverse demand function of the market is given by p = 10-Q, where p is the market price, and Q = 91 +92 is the aggregate output. The marginal costs of the two firms are C₁ 1 and C₂ = 4. = (a) Solve for the Nash equilibrium of the game including firm out- puts, market price, aggregate output, and firm profits. (b) Now suppose these two firms play a 2-stage game. In stage 1, they produce capacities 9₁ and 92, which are equal to the Nash equilibrium quantities of the Cournot game characterised by part (a). In stage 2, they simultaneously decide on their prices p₁ and P2. The marginal cost for each firm to sell up to capacity is 0. It is impossible to sell more than capacity. The residual demand for 10 Piāj if Pi > Pj firm ij, is Di (Pi, Pj) = 10-Pi 2 = if pipi. (Note, if Pi < Pj 10 - Pi here we assume that the efficient/parallel rationing applies). Prove that it is a Nash equilibrium of the second stage subgame that each firm charges the market clearing…arrow_forwardConsider a duopoly market, where two firms sell differentiated products, which are imperfect substitutes. The market can be modelled as a static price competition game, similar to a linear city model. The two firms choose prices p, and p2 simultaneously. The derived demand functions for the two firms are: D1 (P1, P2) = SG+P1)and D2 (P1, P2)= S(;+-P2), where S > 0 and the parameter t > 0 measures the 2t 2t degree of product differentiation. Both firms have constant marginal cost c> 0 for production. (a) Derive the Nash equilibrium of this game, including the prices, outputs and profit of the two firms. (b) From the demand functions, qi= D¡ (p; , p¡ )= SG+P), derive the residual inverse demand functions: p; = P; (qi , p¡) (work out: P; (qi , P;)). Show that for t > 0, P;(qi , P;) is downward 2t aPi (qi ,Pj) . sloping, i.e., c, i.e., firm į has market power. %3D (c) Calculate the limits of the equilibrium prices and profit as t → 0 ? What is P; (qi , p;) as t → 0? Is it downward sloping?…arrow_forwardQUESTION 13 Consider a market where two firms (1 and 2) produce differentiated goods and compete in prices. The demand for firm 1 is given by D₁(P₁, P2) = 140 - 2p1 + P2 and demand for firm 2's product is D2 (P1, P2) 140 - 2p2 + P1 Both firms have a constant marginal cost of 20. What is the Nash equilibrium price of firm 1? (Only give a full number; if necessary, round to the lower integer; no dollar sign.)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education