ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

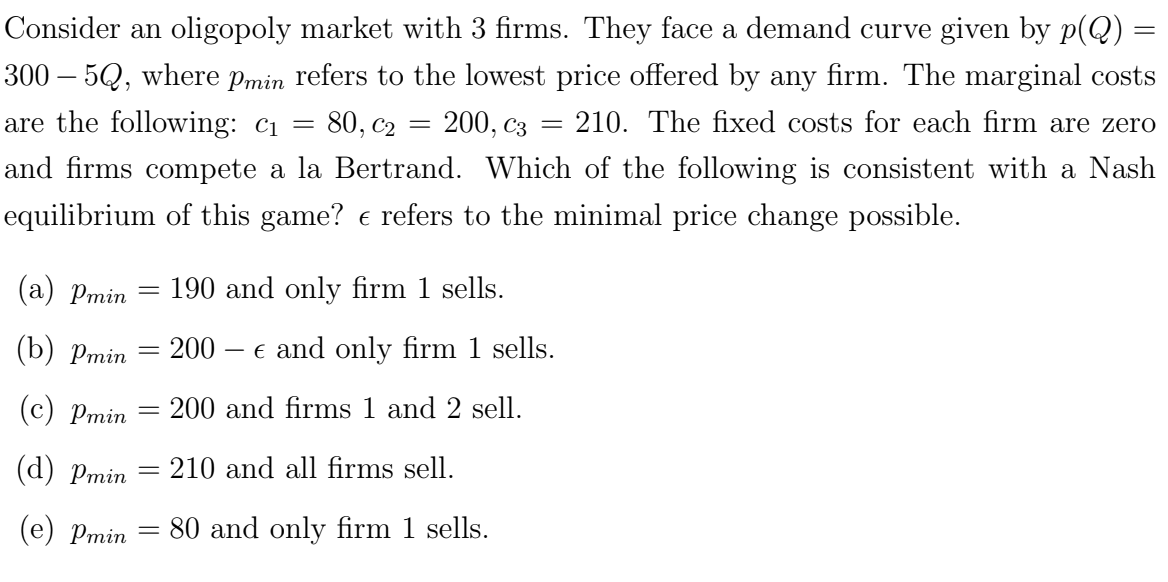

Transcribed Image Text:Consider an oligopoly market with 3 firms. They face a demand curve given by p(Q) =

300 – 5Q, where Pmin refers to the lowest price offered by any firm. The marginal costs

are the following: C₁ = : 80, C₂

210. The fixed costs for each firm are zero

and firms compete a la Bertrand. Which of the following is consistent with a Nash

equilibrium of this game? € refers to the minimal price change possible.

=

(a) Pmin

(b) Pmin

(c) Pmin

(d) Pmin

(e) Pmin = 80 and only firm 1 sells.

200, C3

-

190 and only firm 1 sells.

=

= 200 - € and only firm 1 sells.

200 and firms 1 and 2 sell.

-

=

= 210 and all firms sell.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider the Bertrand pricing game from class. If both firms have identical marginal cost of $10 and consumers will purchase from whichever firm is cheapest as long as the price is under $50, what will be the Nash equilibrium? A B C D 50, 50 50, 10 10, 10 10,50arrow_forwardthe question is in the image attached.arrow_forwardSuppose that there are two firms in a market, firm 1 and firm 2. The marketis declining in size. The game starts in period 0, and the firms can compete in periods 0, 1,2, 3, ... (i.e., indefinitely) if they so choose. Duopoly profits in period t for firm 1 are equalto 105 −10t, and they are 10.5 −t for firm 2. Monopoly profits (those if a firm is the onlyone left in the market) are 510 −25t for firm 1 and 51 −2t for firm 2. At the start of eachperiod, each firm must decide either to “stay in” or “exit” if it is still active (they do sosimultaneously if both are still active). Once a firm exits, it is out of the market forever andearns zero in each period thereafter. Firms maximize their (undiscounted) sum of profits.What is this game’s subgame perfect Nash equilibrium?arrow_forward

- (J)arrow_forwardProblem 3. Consider the following game with three firms. First, firms 1 and 2 si- multancously choose quantities q1 and q2 respectively. After observing firm 1 and 2's quantities, firm 3 chooses its quantity q3. There is no production cost and the inverse demand function is p= 12 – (91 +2 + 93). (a) Compute the SPNE of this game. (b) Give an example of Nash equilibrium s* with s = 4 and s, = 6 , that is not subgame perfect. game theory questionarrow_forward1. Two firms (A and B) play a competition game (i.e. Cournot) in which they can choose any Qi from 0 to ¥. The firms have the same cost functions C(Qi) = 10Qi + 0.5Qi2, and thus MCi = 10 + Qi. They face a market demand curve of P = 220 – (QA + QB). a. Assume firm A chooses quantity first. Frim B observes this choice and then chooses its own quantity. What is Frim B's profit as a function of QA and QB? b. Firm B has MRB = 220 – 2QB – QA. What is firm B’s best response to an arbitrary QA selected by firm A? c. Given that firm A expects firm B’s best response, what is firm A’s profit as a function of QA? (Hint: the only unknown variable in the profit function should be QA) d. Firm A has MRA = 150 – 4QA/3. What are the equilibrium QA and QB selected in this game? e. What is the equilibrium price, and how much profit does each firm collect?arrow_forward

- Space 1 options: less than or equal to, equal to, greater than or equal to Space 2 options: 0 0.5 1 8 16arrow_forwardwhere is the nash equilibrium? find out the dominant strategy. it was discovered that two domestic manufacturing companies were fixing prices. if each company is silent, there is no penalty, but production and business are disrupted due to continuous investigation by the Fair Trade Commission. The penalty for revealing the estimated loss due to the investigation and collusion is as follows: Firm 2 Silence Disclosure Silence -200, -200 -590, 0 Firm 1 Disclosure 0, -590 -450, -450 fine( a hundred million won)arrow_forwardLet ci be the constant marginal and average cost for firm i (so that firms may have different marginal costs). Suppose demand is given by P=1-Q. Calculate the Nash equilibrium quantities assuming there are two firms in a Cournot market. Also compute market output, market price, firm profits, industry prof- its, consumer surplus, and total welfare. Represent the Nash equilibrium on a best-response function diagram. Show how a reduction in firm 1’s cost would change the equilibrium. Draw a representative isoprofit for firm 1.arrow_forward

- Little Kona is a small coffee company that is considering entering a market dominated by Big Brew. Each company's profit depends on whether Little Kona enters and whether Big Brew sets a high price or a low price: True or False: Only Little Kona has a dominant strategy in this game. True or False Which of the following outcomes represent a Nash equilibrium in this case? Check all that apply. Big Brew maintains a high price and Little Kona enters. a.Big Brew maintains a low price and Little Kona enters. b.Big Brew maintains a high price and Little Kona does not enter. c.Big Brew maintains a low price and Little Kona does not enter. Big Brew threatens Little Kona by saying, “If you enter, we're going to set a low price, so you had better stay out.” True or False: Little Kona should not believe the threat. True or False If the two firms could collude and agree on how to split the total profits, what outcome would they…arrow_forwardQUESTION 13 Consider a market where two firms (1 and 2) produce differentiated goods and compete in prices. The demand for firm 1 is given by D₁(P₁, P2) = 140 - 2p1 + P2 and demand for firm 2's product is D2 (P1, P2) 140 - 2p2 + P1 Both firms have a constant marginal cost of 20. What is the Nash equilibrium price of firm 1? (Only give a full number; if necessary, round to the lower integer; no dollar sign.)arrow_forwardConsider the payoff matrix below representing two firms engaged in Bertrand Competition. Firm A is player 1 and Firm B is player 2. High price Low price High price 10, 12 -1, 13 Low price 12, 2 0, 3 What is Firm A's dominant strategy? Question 14Answer a. High price b. Low price c. Firm A does not have a dominant strategyarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education