ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

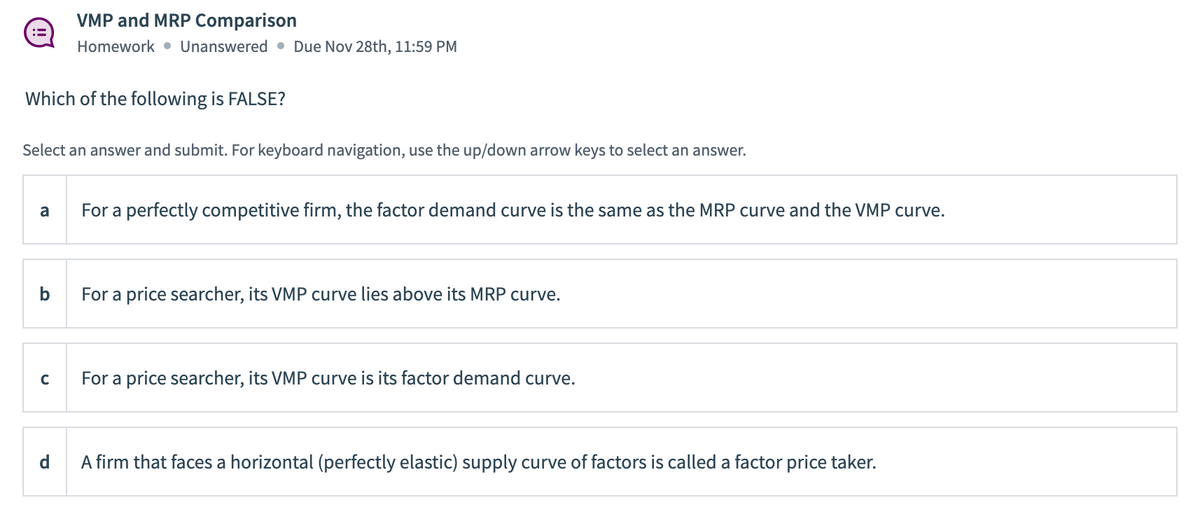

Transcribed Image Text:**VMP and MRP Comparison**

*Homework* | *Unanswered* | *Due Nov 28th, 11:59 PM*

---

**Which of the following is FALSE?**

Select an answer and submit. For keyboard navigation, use the up/down arrow keys to select an answer.

a) For a perfectly competitive firm, the factor demand curve is the same as the MRP curve and the VMP curve.

b) For a price searcher, its VMP curve lies above its MRP curve.

c) For a price searcher, its VMP curve is its factor demand curve.

d) A firm that faces a horizontal (perfectly elastic) supply curve of factors is called a factor price taker.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Assume you look at the graph of a perfectly competitive firm and its average total cost curve is entirely above the horizontal price line. In this case the firm is breaking even. O True O Falsearrow_forwardDoes a compentve firms price equal its marginal cost in a short run, on the long run or both? Explain, Does a competitive firms price equal the minimum of its average total cost in the short run, in the long run, or both ? Explainarrow_forwardOnly typed answer and don't use chatgptarrow_forward

- The figure is not finished but how will you draw the long run equilbirum at the price of $100 on this?arrow_forwardConsider the graph of a firm in a perfectly competitive market to answer the question below: P MC АТС 7 3 MR 10 What is the value of this firm's revenue if it operates where MR=MC? Enter your answer as a number below. Do not include a "$" sign.arrow_forwardRefer to the above diagram for a purely competitive producer. The lowest price at which the firm should produce (as opposed to shutting down) is?arrow_forward

- Consider a firm selling apples and the market for apples is perfectly competitive. The following table presents the costs of a firm. Use the given information to answer questions 35 - 42. Q AFC AVC ATC MC TC 1$300 $100 $400$100$400 2 150 75 225 50 3 100 70 170 60 4 75 72.5 147.5 80 5 60 80 140 11O| 6 50 90 140 140| Find the market price such that the firm's maximized profit = $0 Answer: The firm's maximized profit is $0 if the market price = $.arrow_forwardWhat is output per firm at the long-run equilibrium price? What is the long-run equilibrium profit?arrow_forwardO Farmer Brown grows peaches in Georgia. Suppose the market for peaches is perfectly competitive and that the market price for a box of peaches is $32 per box. Farmer Brown's marginal cost of production is illustrated in the table. Boxes of Peaches Market Price (per box) Marginal Cost (MC) 0 $32 1 32 10.00 2 32 5.00 3 32 15.00 4 32 30.00 5 32 60.00 6 32 90.00 What price will farmer Brown charge when maximizing profit? Farmer Brown will charge a price of $☐ per box of peaches. (Enter your response as an integer.) What is farmer Brown's profit-maximizing level of output? Farmer Brown maximizes profit when producing boxes of peaches. (Enter your response as an integer.) Time Remaining: 01:15:52 Nextarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education