FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

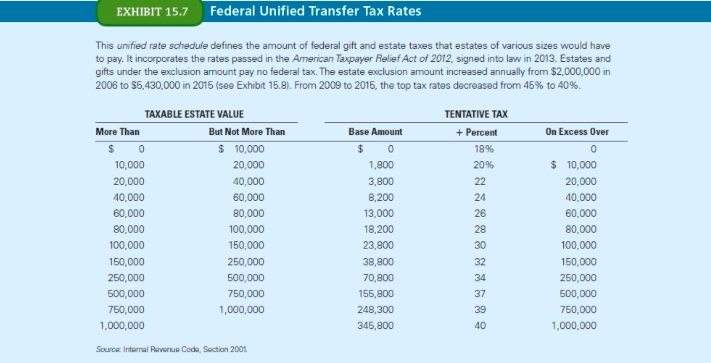

When Jacob Kohler died unmarried in 2015, he left an estate valued at $7,900,000. His trust directed distribution as follows: $20,000 to the local hospital, $170,000 to his alma mater, and the remainder to his three adult children. Death-related costs and expenses were $15,800 for funeral expenses, $50,000 paid to attorneys, $3,500 paid to accountants, and $35,000 paid to the trustee of his living trust. In addition, there were debts of $80,000. Use Exhibit 15.7 and Exhibit 15.8 to calculate the federal estate tax due on his estate. Round your answer to the nearest whole dollar.

Transcribed Image Text:EXHIBIT 15.7 Federal Unified Transfer Tax Rates

This unified rate schedule defines the amount of federal gift and estate taxes that estates of various sizes would have

to pay. It incorporates the rates passed in the American Taxpayer Relief Act of 2012, signed into law in 2013. Estates and

gifts under the exclusion amount pay no federal tax. The estate exclusion amount increased annually from $2,000,000 in

2006 to $5,430,000 in 2015 (see Exhibit 15.8). From 2009 to 2015, the top tax rates decreased from 45% to 40%.

TAXABLE ESTATE VALUE

TENTATIVE TAX

But Not More Than

On Excess Over

More Than

Base Amount

+ Percent

$ 10,000

$ 0

18%

10,000

20,000

1,800

20%

$ 10,000

20,000

40,000

3,800

22

20,000

40,000

60,000

8,200

24

40,000

60,000

80,000

13,000

26

60,000

80,000

100,000

18,200

28

80,000

100,000

150,000

23,800

30

100,000

150,000

250,000

38,800

32

150,000

250,000

500,000

70,800

34

250,000

500,000

750,000

155,800

37

500,000

750,000

1,000,000

248,300

39

750,000

1,000,000

345,800

40

1,000,000

Source: Intornal Revonue Codo, Section 2001

Transcribed Image Text:EXHIBIT 15.8

Unified Credits and Applicable Exclusion Amounts for Estates and Gifts

On December 17, 2010, the Tax Relief, Unemployment Insurance Reauthorization and Job Creation Act of 2010 was

signed into law. The major features of the transfer tax provisions were to reinstate the transfer tax on estates, change the

applicable exclusion amount for both gift transfers and estate transfers, and add the portability of the unified transfer tax

credit. This table shows the recent history of the applicable exclusion amounts.

Year

Unified Tax

Credit-Estates

Applicable Exclusion

Amount-Estates

Unified Tax

Credit-Gifts

Applicable Exclusion

Amount-Gifts

2006

$780,800

$2,000,000

$345,800

$1,000,000

2007

$790,800

$2,000,000

$345,800

$1,000,000

2008

$780,800

$2,000,000

$345,800

$1,000,000

2009

$1,455,800

$3,500,000

$345,800

$1,000,000

2010

Estate tax repealed for 2010

$330,800

$1,000,000

$1,730,800

$5,000,000

$1,730,800

$5,000,000

$5, 120,000

$5,250,000

$5,340,000

2011

2012

$1,772,800

$5,120,000

$1,772,800

2013

$2,045,800

$5,250,000

$2,045,800

2014

$2,081,800

$5,340,000

$2,081,800

2015

$2,117,800

$5,430,000

$2,117,800

$5,430,000

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- narrow_forwardThe terms of a will currently undergoing probate are: “A gift to my brother Chris of $40,000 cash; to my son Eric, $75,000 from my Redstone Savings Bank account; and to my daughter Lauryn, all of my remaining property.” At the time of death, the balance in the savings account was $60,000, and there was additional cash (after payment of funeral expenses and all claims against the estate) of $95,000. The gift to Chris is aarrow_forwardFor the current year, Gina Hestopolis had adjusted gross income of $100,000. During the year, she contributed a total of $6,000 in cash to her church evenly throughout the year and an additional $3,000 in cash to qualified charities. She also contributed religious artwork with a fair market value of $60,000 and a basis of $20,000 to her church. The church intends to display the religious artwork in the church foyer. If Gina chooses to itemize her deductions, what is the amount of her deductible charitable contribution in the current year?Group of answer choices$9,000. $20,000. $35,400.$60,000.arrow_forward

- When Jacob Kohler died unmarried in 2015, he left an estate valued at 7,900,000. His trust directed distribution as follows: $19,000 to the local hospital, $150,000 to his alma mater, and the remainder to his 3 children. Death-related costs and expenses were $15,100 for funeral, $30,000 paid to attorneys, $6,500 paid to accountants, and $35,000 paid to the trustee of his living trust. In addition, debts of $115,000. Calculate the federal estate tax due on his estate.arrow_forwardHana's only child, Kwan, passed away last year at the age of 42. Kwan had been diagnosed with a severe disability as a child and was financially and physically dependent on Hana his entire life. Hana opened an RDSP for Kwan nine years ago and contributed a total of $27,000 to the account. Hana's contributions attracted total Canada Disability Savings Grants (CDSG) of $6,000. The RDSP had a balance of $42,000 when Kwan died. What is the tax impact resulting from Kwan's death? Question 20 options: Kwan's estate will receive taxable income of $9,000 and non-taxable income of $ 27,000. Kwan's estate will receive taxable income of $15,000 and Hana will receive non-taxable income of $27,000. Kwan's estate will receive taxable income of $27,000 and non-taxable income of $15,000.arrow_forwardCora, 79, has an estate that includes her personal residence valued at $120,000 and $18,000 in a bank account that is solely in her name. She would like to arrange her estate so that she maintains exclusive control of the assets during her lifetime, but at her death the assets will pass to her friend, Mabel, outside of probate. Based on Cora's goals and situation, which of the following are correct statements about will substitutes that she could use? She should put her bank account in tenancy in common with Mabel. She should title her personal residence in joint tenancy with her friend, Mabel. She should execute a will that names her friend, Mabel, as the legatee of the bank account and the devisee of the personal residence. She should place the bank funds in a payable on death (POD) account with Mabel as beneficiary. She should change the title on her personal residence to indicate a life estate reserved for her lifetime and a remainder to her friend, Mabel. A)IV and V…arrow_forward

- Norma, a widow, has made lifetime gifts to her two grandchildren in an effort to reduce the size of her gross estate. In 2012, Norma made a $100,000 taxable gift. She made another $150,000 taxable gift in 2014. She used her gift tax applicable credit amount to offset any gift tax liability for all gifts. What amount of gift tax applicable credit remains available to Norma in 2022? A)$4,641,000 B)$70,800 C)$4,656,000 D)$4,699,000arrow_forwardBob died with a gross estate of $4,500,000, half of which is attributable to the value of stock in Graystone Inc., a closely held corporation. Bob owns 80% of Graystone Inc. He had no debts, and his estate administrative expenses were $50,000, of which $10,000 constitutes the personal representative's statutory fee. His will named his wife, Pearl, as the sole beneficiary of his estate and as his personal representative. Bob made no lifetime taxable gifts. Which of the following postmortem techniques are available and advisable for Bob's estate or its sole beneficiary, Pearl? Election of Section 6166 payment of estate taxes Use of the alternate valuation date Waiver by Pearl of the right to her statutory fee as personal representative Election of a Section 303 stock redemption A) III and IV B) II only C) I and II D) I, III, and IVarrow_forwardThis year Carla received corporate stock worth $35,000 as a gift from her grandfather. Her grandfather originally had purchased the stock in 2012 at a cost of $20,000. No gift taxes were paid on the transfer. Three months after receiving the stock. Carla sold it for $32,000. What are the amount and character of gain or loss recognized by Carla on this transaction?arrow_forward

- To whom is the income allocated, why, and how much: When Worf’s parent’s died, the made him the beneficiary of a trust which holds real estate as well as income producing assets. Worf distributes one of the rental properties to Alexander outright. Alexander collects the rent from the tenants and manages the properties. In 2011, his revenue less his costs was 50K, and in 2010 his revenue less his costs was 32K.arrow_forwardMunabhaiarrow_forwardLinda Smith paid $25,000 in premiums on a 20-year endowment policy on her life. The policy has a face value of $40,000. At age 60, Linda decides to collect the face value of the policy. In the year of collection, how much will Linda include in her taxable income?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education