Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

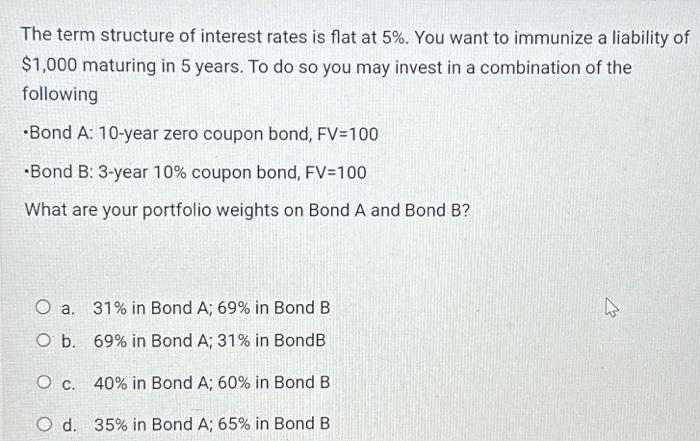

Transcribed Image Text:The term structure of interest rates is flat at 5%. You want to immunize a liability of

$1,000 maturing in 5 years. To do so you may invest in a combination of the

following

•Bond A: 10-year zero coupon bond, FV=100

•Bond B: 3-year 10% coupon bond, FV=100

What are your portfolio weights on Bond A and Bond B?

O a. 31% in Bond A; 69% in Bond B

O b. 69% in Bond A; 31% in BondB

O c. 40% in Bond A; 60% in Bond B

O d. 35% in Bond A; 65% in Bond B.

ہے

4

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Consider a bond that is currently priced at $1100. If the face value of the bond is $1000, coupon payments are made semiannually, the bond matures in 5 years, and the YTM is 3%, what is the coupon rate? Group of answer choices 5.17% 2.58% 3.00% $25.84arrow_forwardSuppose that you want to construct a 2-year maturity forward loan commencing in 3 years. The face value of each bond is $1,000. Maturity (Years) 1 2 3 4 5 Price $ 996.04 895.89 833.92 772.80 675.18 Required: a. Suppose that you buy today one 3-year maturity zero-coupon bond with face value $1,000. How many 5-year maturity zeros would you have to sell to make your initial cash flow equal to zero (specifically, what must be the total face value of those 5-year zeros)? b. What are the cash flows on this strategy in each year? c. What is the effective 2-year interest rate on the effective 3-year-ahead forward loan? d. & e. Confirm that the effective 2-year forward interest rate equals (1 + f4) ×(1 + f5)-1. You therefore can interpret the 2-year loan rate as a 2-year forward rate for the last two years. Alternatively, show that the effective 2-year forward rate equals (1 + y5) 15 + (1+y3) ³. - 1arrow_forwardWhat is the price of a bond with the following information? It is 1.5 years until expiration. The coupon rate is 7 percent and coupon payments are made once per year. The market rate of return is 5.9 percent. The bond has a face value of 2000 SEK. Tips Draw a time axis so that you do not make any mistakes with the discounting. Don't look at the cash flows as an annuity, but as two separate cash flows. There is always a coupon payment when the bond matures, how long is it then until the next coupon payment? (Answers are rounded to integers) a) 265 b) 2100 c) 1971 d) 1990 e) 2216arrow_forward

- Consider a 5 year non-call 3 year bond that is callable in 3 year and 4 year at prices of 101 and 100. It pays an annual coupon of 4% and is priced at 101. What is the yield-to-worst for this bond?arrow_forwardYou are considering a 10-year, Rs. 1000 par value bond. Its coupon rate is 10% and interest is paidsemiannually. If you require an effective annual interest rate of 8%, how much should you be willingto pay for the bond? Is effective annual interest rate differing from coupon rate? Explain.arrow_forwardA bond has a coupon rate of 5.2%, and 6.5 years until maturity. If the YTM is 6.2%, what is the price of this bond? TIP: Write the price as a percentage of the bonds par value. All bonds in this class make two coupon payments per year, and have a face value of $1,000. You don't need to write in the "%" sign.arrow_forward

- 2. You are holding a 3-year bond with coupon rate 10%. Coupon payments are annual and par values are 100. Spot rates are: r₁ = 5%, r₂ 6%, r3 = 6.5%. (a) Determine as many forward rates as you can based on the spot rates above. (b) You would like to get a guaranteed 3-year return on your coupon bond. Explain how this can be achieved using forward rates. Which forward rates should you use? What is your guaranteed 3-year return?arrow_forwardSimplest way plsarrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education