ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

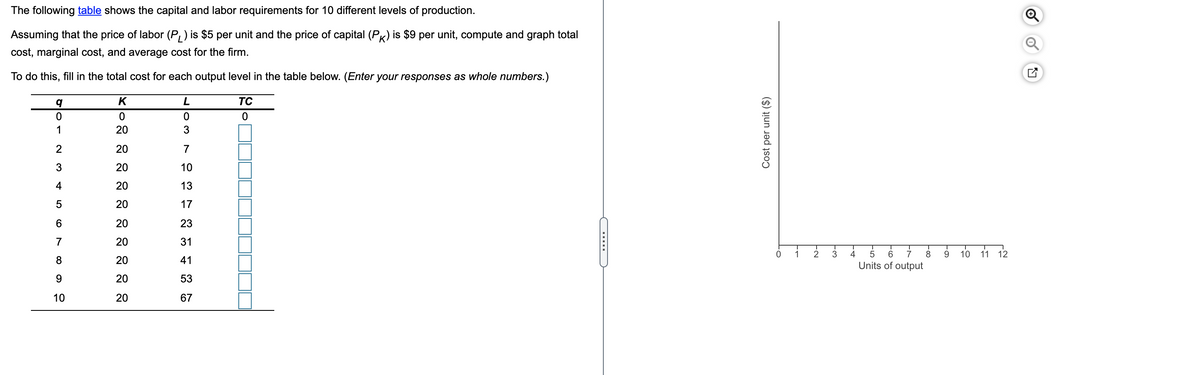

Transcribed Image Text:The following table shows the capital and labor requirements for 10 different levels of production.

Assuming that the price of labor (P, ) is $5 per unit and the price of capital (PK) is $9 per unit, compute and graph total

cost, marginal cost, and average cost for the firm.

To do this, fill in the total cost for each output level in the table below. (Enter your responses as whole numbers.)

K

TC

1

20

3

20

7

3

20

10

4

20

13

20

17

6.

20

23

7

20

31

3 4 5 6 i &

Units of output

0 1

7

10

11 12

8.

20

41

20

53

10

20

67

LO

Cost per unit ($)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Similar questions

- Suppose that the Acme Gumball Company has a fixed proportions production function that requires it to use two gumball presses and one worker to produce 1,000 gumballs per hour. a. Explain why the cost per hour of producing 1,000 gumballs is 2v + w (where v is the hourly rent for gumball presses and w is the hourly wage). b. Assume Acme can produce any number of gumballs they want using this technology. Explain why the cost function in this case would be TC = q(2v +w), where q is output of gumballs per hour, measured in thousands of gumballs. c. What is the average and marginal cost of gumball production (again, measure output in thousands of gumballs)? (show the complete formula) Draw the graph for the average and marginal cost curves for gumballs assuming v=3, w-5 (show working) Now draw the graph for these curves for v=6, w=5.( show working) Explain why these curves have shifted.arrow_forwardcan you explain the solution for part b like for example how did they get M=y^2/2 and L=2y^2arrow_forwardCalculate total costs at 4 units of output. Do not put a dollar sign in your answer. (The 6 columns are Quantity, Total Fixed Cost, Total Variable Cost, Total Cost, Average Total Cost, and Marginal Cost. The Quantity and Total Variable Cost columns have been filled in along with the first row for Total Fixed Cost. Average Total Costs and Marginal Costs are not calculated at a quantity of 0.) Quantity Total Fixed Cost Total Variable Cost Total Cost Average Total Cost Marginal Cost 0 15 0 XXXXX XXXXX 1 25 2 40 3 50 4 55 5 65 Calculate average total costs at 2 units of output. Calculate average total cost at 5 units of output. Calculate marginal cost at 4 units of output (moving from 3 units to 4 units). Can you tell if this is the short run or long run? Can you tell at which level of output profits will be maximized?arrow_forward

- Confused and uncertain on what to do to solve correctlyarrow_forwardLet F be the fixed cost of production, let VC be the variable cost of production, C be the total cost, MC be the marginal cost, AFC, the average fixed cost, AVC, the average variable cost, and AC, the average cost. Complete the following cost table. (Enter numeric responses rounded to two decimal places.) Output (q) 1 2 3 4 5 6 7 8 9 10 F $250 250 250 250 250 250 250 250 250 с MC AFC AVC AC $266 $16 $250.00 $16.00 $266.00 12 125.00 14.00 139.00 8 83.33 12.00 4 62.50 10.00 72.50 298 50.00 59.60 8 310 12 41.67 10.00 51.67 76 326 35.71 10.86 46.57 96 346 20 12.00 43.25 41.11 27.78 13.33 120 370 24 148 28 25.00 14.80 VC $16 28 278 36 286 40 48arrow_forwarddiscussion should be no less than 75 words. In doing so, be certain to address each of the components from the topic. The most desirable output quantity for the firm clearly depends on how costs change as output varies. First, discuss the three types of cost curves economists use to display and analyze this information. Then, discuss the marginal product relationship. Lastly, give one example of how costs change as output varies for the firm from a recent news articlearrow_forward

- Explain why this statement is true or false: "If the labor cost per table is $20 and the material cost per table is $30, the short run average cost per table is $50."arrow_forwardWhat is direct cost? What is indirect cost? Provide detailed definitions and example for botharrow_forwardMarginal cost, average total cost and average variable cost Marginal cost and average total cost are always equal. Do you agree? Explain. If you disagree then write under what situation they are equal. b. Marginal cost and average variable cost are always equal. Do you agree? Explain. If you disagree then write under what situation they are equal.arrow_forward

- The production function for a product is given by q= 10K^(1/2)L^(1/2) where K is capital, and L is labor and q is output d) Now suppose w =30 and r = 120. What is the minimum cost of producing q=1000. (You must show your work by clearly writing the equations that you use to derive the cost minimizing levels of L and K.) e) Now suppose that the firm is in the short run and cannot vary the amount of capital. That is, it must use the same amount of capital as in part d). However, the firm wants to produce 1200 units of output. How much labor should it use to minimize its cost and what is the minimum cost of producing q =1200?arrow_forward30. The production function is f(L, M) = 4L1/2 M¹2, where L is the number of units of labor and M is the number of machines used. If the cost of labor is $49 per unit and the cost of machines is $16 per unit, then what is the total cost of producing 5 units of output?arrow_forwardLet F be the fixed cost of production, let VC be the variable cost of production, C be the total cost, MC be the marginal cost, AFC, the average fixed cost, AVC, the average variable cost, and AC, the average cost. Complete the following cost table. (Enter numeric responses rounded to two decimal places.) Output (q) 1 2 3 4 31 5 6 7 8 9 06 10 F $200 200 200 200 200 200 200 200 200 VC $48 84 108 120 144 344 380 228 428 288 488 60 560 с MC $248 $48 AFC AVC AC $200.00 $48.00 $248.00 284 36 100.00 42.00 142.00 308 24 66.67 36.00 12 50.00 30.00 80.00 24 40.00 68.80 36 33.33 30.00 63.33 28.57 32.57 61.14 36.00 61.00 40.00 62.22 44.40 360 444 72 84 22.22 20.00arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education