ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

thumb_up100%

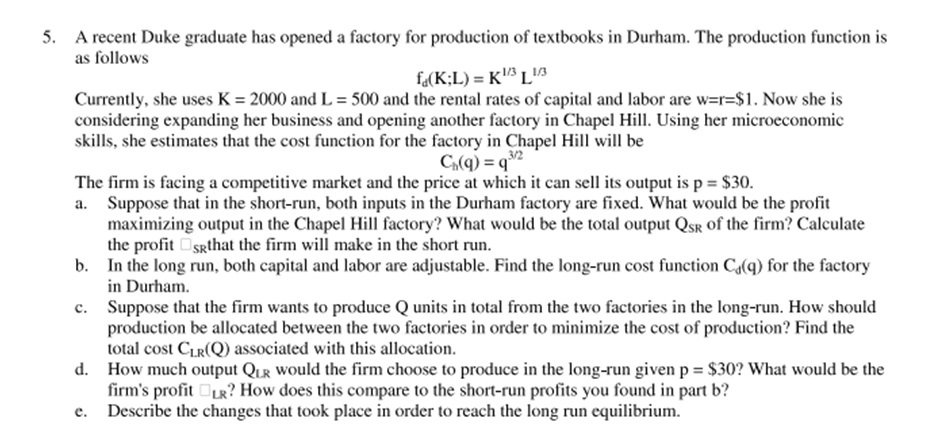

Transcribed Image Text:5. A recent Duke graduate has opened a factory for production of textbooks in Durham. The production function is

as follows

f«(K;L) = K³ L

Currently, she uses K = 2000 and L = 500 and the rental rates of capital and labor are w=r=$1. Now she is

considering expanding her business and opening another factory in Chapel Hill. Using her microeconomic

skills, she estimates that the cost function for the factory in Chapel Hill will be

3/2

C(q) = q°

The firm is facing a competitive market and the price at which it can sell its output is p = $30.

a. Suppose that in the short-run, both inputs in the Durham factory are fixed. What would be the profit

maximizing output in the Chapel Hill factory? What would be the total output QSR of the firm? Calculate

the profit Sgthat the firm will make in the short run.

b. In the long run, both capital and labor are adjustable. Find the long-run cost function Ca(q) for the factory

in Durham.

c. Suppose that the firm wants to produce Q units in total from the two factories in the long-run. How should

production be allocated between the two factories in order to minimize the cost of production? Find the

total cost CLR(Q) associated with this allocation.

d. How much output QuR Would the firm choose to produce in the long-run given p = $30? What would be the

firm's profit R? How does this compare to the short-run profits you found in part b?

Describe the changes that took place in order to reach the long run equilibrium.

е.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Does the production function y=0.8x_1x_2 exhibit constant returns to scale, increasing returns to scale, decreasing returns to scale, or homothetic returns to scalearrow_forwardRBW produces light sticks for one of their legendary girl groups, Kara. Suppose that RBWuses capital, K, and labor, L, to produce the light sticks. The production function is given as: Q(K,L)=2K0.75L0.51. Identify if RBW’s production function is increasing, constant, or decreasing returns to scale with a brief explanation. Also, solve for the company’s cost minimization problem by providing conditional demand functions of labor and capital, with respect to their input prices. Assume that w is the wage of labor and r is the rent cost of capital.2. Suppose that RBW is preparing for a mini-fan meet for the group’s “When I move” mini-album launch and that they have to provide 200 light sticks. The wage of labor, w, is $6.00 and the cost of capital, r, is $2.00. Determine how much labor and capital they have to use and the total cost of producing the light sticks.arrow_forward22. Suppose a firm has a production technology given by the Cobb-Douglas production function: Q = f(L,K) = AL¤ KB with a + ß 0, where L and K represent labour and capital respectively and A is technology. (a) Does this production function exhibit constant, increasing or decreasing returns to scale? Explain how you would be able to see this on an isoquant graph. (b) Set out the unconstrained profit maximisation problem (assuming input prices are w for labour and r for capital and the output price is p) and then solve for the unconditional input demand functions for capital and labour and find the firm's supply function (c) Now set up the cost minimisation problem and solve for the conditional labour and capital demands. What is the difference between the unconditional input demand functions from part (b) and the conditional input demand functions you have just derived? (d) Give an expression for the total cost function (no need to simplify) and explain how the average and marginal cost…arrow_forward

- can you explain the solution for part b like for example how did they get M=y^2/2 and L=2y^2arrow_forwardsolve this onearrow_forwardExplain why this statement is true or false: "If the labor cost per table is $20 and the material cost per table is $30, the short run average cost per table is $50."arrow_forward

- Note: Enter your answer withtout the dollar sign ($) For the cost function TC= 520 + 10Q + 5Q2, determine the average fixed cost of producing 5 units of output.arrow_forwardQ3, A firm operates with the following Cobb-Douglas production function where Q is output, L is labor hours per week, and K is machine hours per week. Cobb-Douglas Production Function: Q = 5(L1/3K2/3) The firm intends to produce 5,000 units of output per week by contracting employees for $40 per hour and renting machinery for $10 per hour. Determine the cost minimizing combination of labor and capital for the firm. Based on your solution in part (a), calculate the firm’s total cost of producing 5,000 units of output per week.arrow_forwardCould you solve d,e,f ? Thank youarrow_forward

- Please answer fast please arjent help please ASAP pls answer fastarrow_forwardThe short run production function of a competitive firm is given The short-run production function of a competitive firm is given by f (L) = 6L2/3, where L is the amount of labor it uses. (For those who do not know calculus—if total output is aLb, where a and b are constants, and where L is the amount of some factor of production, then the marginal product of L is given by the formula abLb−1.) The cost per unit of labor is w = 6 and the price per unit of output is p = 3. (a) Plot a few points on the graph of this firm’s production function and sketch the graph of the production function, using blue ink. Use black ink to draw the isoprofit line that passes through the point (0, 12), the isoprofit line that passes through (0, 8), and the isoprofit line that passes through the point (0, 4). What is the slope of each of the isoprofit lines? (b) How many units of labor will the firm hire? (c) Suppose that the wage of labor falls to 4, and the price of output…arrow_forwardConsider the following production functions, to be used in this week’s assignment:(A) F(L, K) = 20L^2 + 20K^2(B) F(L, K) = [L^1/2 + K^1/2]^2 (i) Neatly draw the Q = 2,000 isoquant for a firm with production function (A) given above,putting L on the horizontal axis and K on the vertical axis. As part of your answer, calculate three inputbundles on this isoquant. (ii) Neatly draw the Q = 10 isoquant for a firm with production function (B) givenabove. As part of your answer, calculate three input bundles on this isoquant. For your three input bundles,choose one with L = 0, choose one with K = 0, and the third with L = K. PLEASE SHOW ALL WORKarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education