ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Confused on how to find the long-run supply

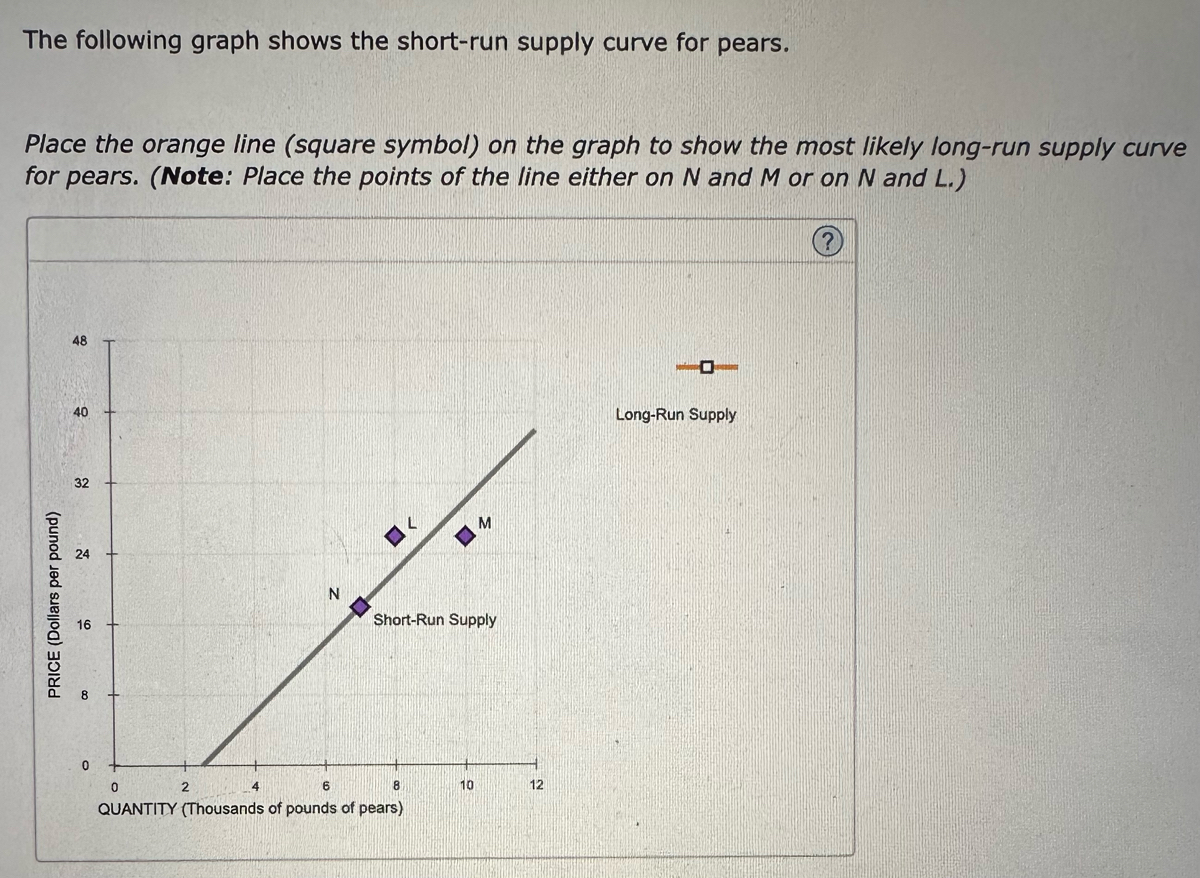

Transcribed Image Text:The following graph shows the short-run supply curve for pears.

Place the orange line (square symbol) on the graph to show the most likely long-run supply curve

for pears. (Note: Place the points of the line either on N and M or on N and L.)

PRICE (Dollars per pound)

48

40

32

24

16

8

0

0

N

2

6

8

QUANTITY (Thousands of pounds of pears)

Short-Run Supply

M

10

12

-

Long-Run Supply

Expert Solution

arrow_forward

Step 1

The supply curve depicts the positive relationship between price and quantity supplied, keeping other factors of supply constant.

In the short run, the quantity supplied is less responsive to changes in price.

In the long run, the quantity supplied is more responsive to changes in price.

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- In 2003, a single case in Alberta of bovine spongiform encephalopathy, also known as mad cow disease, temporarily shut down export markets for Canadian beef. a. Using firm and industry diagrams, show the short-run effect of declining demand for Canadian beef due to the shutdown of its export markets. Label the diagram carefully and write out in words all of the changes that you can identify. b. Although export markets eventually began to open up later that same year, the demand for Canadian beef remained low. On a new diagram, show the long-run effect of the declining demand. Explain in words.arrow_forwardExplain in detail how purely competitive markets, in the long-run, know how to adjust to and provide the correct output, at the correct price. Give an example of a good or service you might buy that is closest to being in a purely competitive market. Explain your logic.arrow_forwardChoose the one alternative that best that answers the question. Assume the market for organic produce is perfectly competitive. All else being equal, as more farmers choose to produce and sell organic produce, in the long-run, Select one: a. The equilibrium price is likely to increase, and profits are likely to remain unchanged. b. The equilibrium price is likely to remain unchanged, and profits are likely to increase. c. The equilibrium price is likely to decrease, and profits are likely to decrease. d. The equilibrium price is likely to increase, and profits are likely to increase. e. Both the equilibrium price and quantity are likely to remain unchanged.arrow_forward

- Explain in detailarrow_forwardThe figure below depicts the market supply and demand for the perfectly competitive rollerblade industry. S Price per pair of Rollerblades 1,140 070 50 150 Number of pairs of Rollerblades per week Based on the figure above, if the current quantity demanded of rollerblades is 150 per week, you accurately predict that in the short run, Q Select one: a. price and quantity supplied will increase and quantity demanded will decrease. b. price and quantity supplied will decrease and quantity demanded will increase. c. price, quantity supplied and quantity demanded will increase. d. price, quantity supplied and quantity demanded will decrease.arrow_forwardPrice Average total cost AVC Demand Marginal cost Marginal revenue Q Quantity Discuss the firm plotted on the figure. What type of firm do you see?is the firm operating at the optimal point of production? is the firm making a proht? s the firm operating in the short or in the long run?arrow_forward

- Assume that the market for pasta is in long-run equilibrium and that the pasta industry is a constant-cost industry. Explain with a graph and words what will happen to the price and quantity in the market when the demand for pasta decreases.arrow_forwardYou are the manager of a taco truck that is in a perfectly competitive industry comprised if identical firms. The cost of taco ingredients increases form $15 to $20 per hundred pounds. a. In the short run, how do you respond to the increases in the price of ingredients? b. Describe the long-run adjustments that take place in the market place. c. What long-run decisions will you make as the manager of your firm?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education