ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

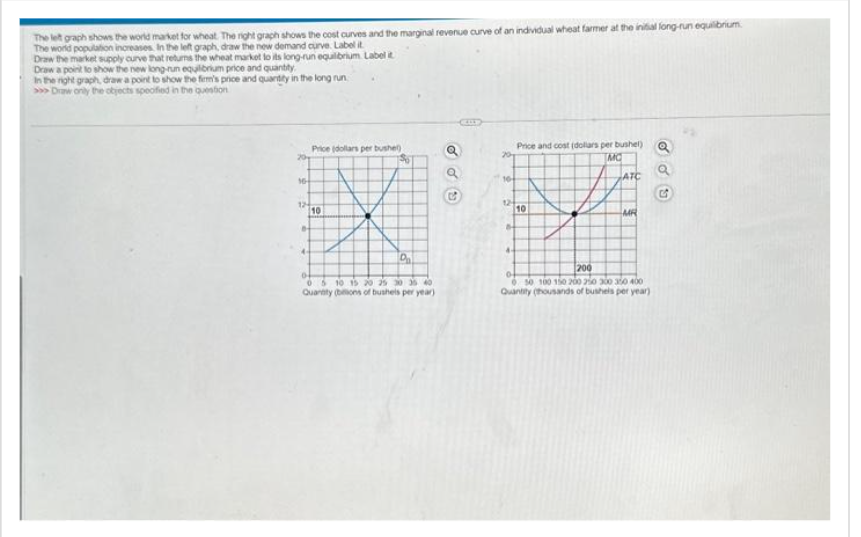

Transcribed Image Text:The let graph shows the world market for wheat. The right graph shows the cost curves and the marginal revenue curve of an individual wheat farmer at the initial long-run equilibrium

The world population increases. In the left graph, draw the new demand curve. Label it

Draw the market supply curve that returns the wheat market to its long-run equilibrium. Label it

Draw a point to show the new long-run equilibrium price and quantity

In the right graph, draw a point to show the firm's price and quantity in the long run

>>>Draw only the objects specified in the question

16

124

Price (dollars per bushel)

10

P₁

05 10 15 20 25 30 35 40

Quantity (bons of bushels per year)

C

Price and cost (dollars per bushel)

20

MC

10

ATC

124

M

10

MAR

200

650 100 150 200 250 300 350 400

Quantity (thousands of bushels per year)

0

a

3

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Herriott's is the only veterinary clinic in a remote village. The graph shows the demand curve for the firm's vet visits. Now suppose that there are 30 veterinary clinics, all able to produce these vet visits at zero marginal cost and with zero fixed costs. How does the equilibrium price and quantity produced with 30 veterinary clinics compare to Herriot's price and quantity produced? Draw the supply curve when there are 30 veterinary clinics. Label it. Draw a point at the equilibrium price and quantity. The monopoly price is The monopoly output is A. higher; less B. higher; greater OC. lower; less D. lower; greater than the perfectly competitive price. than the perfectly competitive output. C 120 100- 80- 60- 40- 20- 0- 0 Price and cost (dollars per visit) D 8 24 16 32 Quantity (visits per day) >>> Draw only the objects specified in the question. 40 ON 48arrow_forwardEvery House in a small town has a well that provides water at no cost. However, if the town wants more than 10,000 gallons a day, it has to buy extra water from firms located outside of the town. The town currently consumes 9,000 gallons per day. a. Draw a linear demand curve b. The firm's supply curve is linear and starts at the origin. Draw the market supply curve, which includes the supply from the town's well. c. Show the equilibrium. What is the equilibrium quantity? What is the equilibrium price? Explain Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardSally runs a vegetable stand. The following table shows two points on the demand curve for the heirloom tomatoes she sells: Price $3.50 $2.25 Quantity demanded per week 150,000 250,000 Sally's marginal revenue from lowering the price of tomatoes from $3.50 to $2.25 is $ 0.375. (Enter your response rounded to two decimal places.) Lowering the price from $3.50 to $2.25 results in an output effect of $ and a price effect of $. (Enter your responses as whole numbers and include a minus sign if necessary.)arrow_forward

- Imagine that the perfectly competitive turkey industry is in long-run equilibrium at a price of $3 per kilogram of turkey and a quantity of 600 million kilograms per year. Imagine the department of health issues a report saying that eating turkey is bad for your health.arrow_forwardThe figures below show (on the left) two possible demand curves and (on the right) two possible supply curves in the perfectly competitive hamburger market. Price per hamburger 0 B D₂ D₁ Hamburgers per month A Price per hamburger 0 F Select one: a. Movement along D₁ from Point A to Point B. b. Demand shifts from D₁ to D₂. c. Movement along S₁ from Point F to Point G. d. Demand shifts from D₂ to D₁. G S₂ S₁ Hamburgers per month Assume that people consume either hamburgers or hot dogs. What will be the result of a decrease in the price of hot dogs? Hint: Are hamburgers and hotdogs complements or substitutes?arrow_forwardSuppose that the tuna industry is in long-run equilibrium at a price of $5 per can of tuna and a quantity of 350 million cans per year. Suppose the Surgeon General issues a report saying that eating tuna is bad for your health. The Surgeon General's report will cause consumers to demand tuna at every price. In the short run, firms will respond by Shift the demand curve, the supply curve, or both on the following graph to illustrate these short-run effects of the Surgeon General's report. 10 Supply Demand 8 7 Supply Demand 2 1 70 140 210 280 350 420 490 560 630 700 QUANTITY (Millions of cans) In the long run, some firms will respond by until PRICE (Dollars per can)arrow_forward

- Suppose a corn dog stand market is perfectly competitive and in long-run equilibrium. One day, the city starts imposing a $300 per year tax on each stand. How does this policy impact the number of corn dogs produced and sold in the market in the short run and long run? Down in the short run and no change in the long run No change in the short run and down in the long run Up in the short run and no change in the long run No change in the short run and up in the long runarrow_forwardNo image solutionarrow_forwardAnswer the allarrow_forward

- In a competitive market, are market supply curves typically more elastic in the short run or in the long run? Explain within 40 words.arrow_forward. In Taiwan, there is only one beer producer, called Taiwan Beer. The Taiwanese government has passed a law prohibiting any other company from producing and selling beer in Taiwan. Suppose that the demand for beer in Taiwan increases. Explain what happens in the market for beer in Taiwan in the short run. Specifically, explain what happens to the price of beer, the number of beer producers, and the profits of beer producers. Explain what happens in the market for beer in Taiwan in the long run. Specifically, explain what happens to the price of beer, the number of beer producers, and the profits of beer producers. Explain who benefits and who is hurt by the government regulation granting Taiwan Beer a monopoly.arrow_forward9arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education