ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

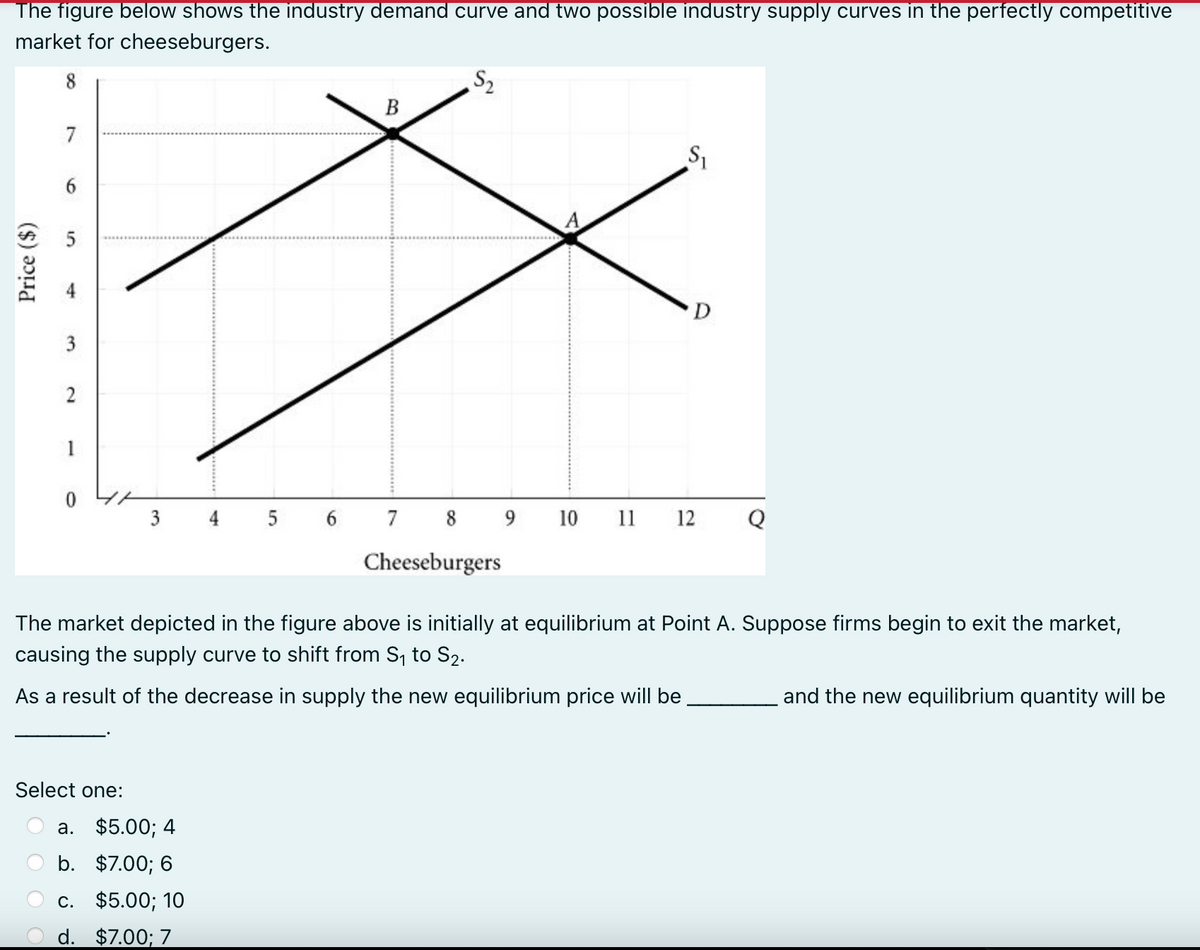

Transcribed Image Text:The figure below shows the industry demand curve and two possible industry supply curves in the perfectly competitive

market for cheeseburgers.

8

Price ($)

7

6

5

3

2

1

0

3

Select one:

5

a. $5.00; 4

b. $7.00; 6

c. $5.00; 10

d. $7.00; 7

B

6 7

S₂

8

Cheeseburgers

9 10 11

S₁

D

12

The market depicted in the figure above is initially at equilibrium at Point A. Suppose firms begin to exit the market,

causing the supply curve to shift from S₁ to S₂.

As a result of the decrease in supply the new equilibrium price will be

Q

and the new equilibrium quantity will be

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- The following graph illustrates the market for small moving trucks in Bloomington, IN, during Indiana's fall move-in week. PRICE (Dollars per small truck) 100 90 80 70 80 50 40 30 20 10 0 Demand I 01 5,50 2 3 8 5 6 7 QUANTITY (Hundreds of small trucks) Supply 9 10 ? Suppose that SendIt is one of over a dozen competitive firms in the Bloomington area that offers moving truck rentals. Based on the preceding graph showing the weekly market demand and supply curves, the price SendIt must take as given is Sarrow_forwardPlease answer sections a-e attached.arrow_forwardFarmer Jones grows sugar. The total revenue, marginal revenue, total cost, and marginal cost of producing various quantities of sugar (bushels in 1000s) are presented in the table below Marginal Output (bushels in 1000s) Total Revenue Marginal Total Revenue Cost Cost 0 $0 0 1 86 86 120 120 2 172 86 200 80 258 86 240 40 344 86 320 80 5 430 86 480 160 516 86 680 200 Suppose the market for sugar is perfectly competitive. To maximize profits, farmer Jones should produce At that level of output, farmer Jones will earn profit of S thousand bushels of sugar. (Enter a numeric response using an integer)arrow_forward

- The figures below show (on the left) two possible demand curves and (on the right) two possible supply curves in the perfectly competitive hamburger market. Price per hamburger 0 A B D₂ D₁ Hamburgers per month Price per hamburger 0 Select one: a. Movement along D₁ from Point A to Point B. b. Demand shifts from D₁ to D₂. F c. Movement along S₁ from Point F to Point G. d. Demand shifts from D₂ to D₁. G Hamburgers per month Assume that people consume either hamburgers or hot dogs. What will be the result of a decrease in the price of hot dogs? Hint: Are hamburgers and hotdogs complements or substitutes? S₂ S₁arrow_forwardThe table below shows the weekly marginal cost (MC) and average total cost (ATC) for Buddies, a purely competitive firm that produces novelty ear buds. Assume the market for novelty ear buds is a competitive market and that the price of ear buds is $6.00 per pair. Buddies Production Costs Quantity MC ATC of Ear Buds ($) ($) 20 1.00 25 2.00 1.20 30 2.46 1.41 35 3.51 1.71 40 4.11 2.01 45 5.43 2.39 50 5.99 2.75 55 8.47 3.27 Instructions: In part a, enter your answer as the closest given whole number. In parts b-d, round your answers to two decimal places. a. If Buddies wants to maximize profits, how many pairs of ear buds should it produce each week? pairs b. At the profit-maximizing quantity, what is the total cost of producing ear buds? 2$ c. If the market price for ear buds is $6 per pair, and Buddies produces the profit-maximizing quantity of ear buds, what will Buddies profit or loss be per week? 2$arrow_forward8. Refer to the information in the table below to answer the following questions: TVC €0 10 15 Quantity of fruit baskets 0 1 2 3 4 5 6 TFC €50 50 50 50 50 50 50 21 31 46 68 TC MC -- 10 5 6 10 15 22 a) The firm sells fruit baskets in a perfectly competitive market. Calculate the firm's total cost for each level of production and complete the table. b) Assume that the market price of a fruit basket is €15. To maximize profit, how many fruit baskets should the firm sell? c) At the profit-maximizing quantity, what is the profit?arrow_forward

- Calculate the consumer surplus if the industry is perfectly competitive according to this diagram in the image.arrow_forwarde following figure, graph (a) depicts the linear marginal cost (MC) of a firm in a competitive market, and grap depicts the linear market supply curve for a market with a fixed number of identical firms. Graph (a): Firm Graph (b): Market PRICE 2 100 MC 200 QUANTITY PRICE O a. The price cannot be determined from the information provided. b. $1.50 c. $2.00 d. $1.00 N Q QUANTITY Q₂ Refer to Figure 14-4. When 100 identical firms participate in this market, at what price will 15,000 units be supplied o this market? Suparrow_forwarda) What is the profit maximising condition in a market with perfect competition?b) Explain what is meant by abnormal profit? What is the adjustment process from short-run abnormal profit to long-run equilibrium in a perfectly competitive market?c) Please find below Pricing options for firm A and B, along with individual payoffs (Firm A’s payoff/Firm B’s payoff)Firm BFirm APrice £2 Price £1Price £2 £20,000/£20,000 £10,000/£24,000Price £1 £24,000/£10,000 £12,000/£12,000Assume you are the pricing manager at Firm A;i) What is your payoff for a ‘maximin’ strategy?ii) What is your payoff for a ‘maximax’ strategy?iii) Does a dominant strategy exist within this prisoners’ dilemma?arrow_forward

- Looking to see how to resolvearrow_forwardFigure 14-7 Graph (a) Graph (b) MC ATC 1. D, Q, a, 0, 0: QUANTITY QUANTITY Refer to Figure 14-7. Assume that the market starts in equilibrium at point W in graph (b). An increase in demand from Do to Di will result in a new market equilibrium at point X. an eventual increase in the number of firms in the market and a new long-run equilibrium at point Z. rising prices and falling profits for existing firms in the market. falling prices and falling profits for existing firms in the market. PRICE PRICEarrow_forward1) If a firm in a purely competitive industry is confronted with an equilibrium price of $5, its marginal revenue: 2) A firm that is motivated by self interest should 3) If price is above the equilibrium level, competition among sellers to reduce the resulting 4) Camille's Creations and Julia's Jewels both sell beads in a competitive market. If at the market price of $5, both are running out of beads to sell (they can't keep up with the quantity demanded at that price), then we would expect both Camille's and Julia's to 5) Since their introduction, prices of DVD players have fallen and the quantity purchased has increased. This statement 6) In a market economy the distribution of output will be determined primarily by 7) In a competitive market economy firms will select the least-cost production technique because 8) Suppose that the price of peanuts falls from $3 to $2 per bushel and that, as a result, the total revenue received by peanut…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education