ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

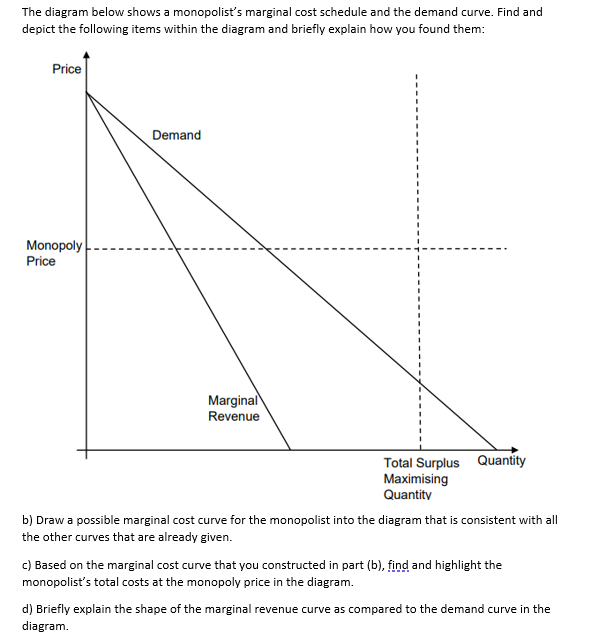

Transcribed Image Text:The diagram below shows a monopolist's marginal cost schedule and the demand curve. Find and

depict the following items within the diagram and briefly explain how you found them:

Price

Monopoly

Price

Demand

Marginal

Revenue

Total Surplus Quantity

Maximising

Quantity

b) Draw a possible marginal cost curve for the monopolist into the diagram that is consistent with all

the other curves that are already given.

c) Based on the marginal cost curve that you constructed in part (b), find and highlight the

monopolist's total costs at the monopoly price in the diagram.

d) Briefly explain the shape of the marginal revenue curve as compared to the demand curve in the

diagram.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- what is the profit from perfect price discrimination?arrow_forwardWith regard to market structure, answer the following: (a) A monopolist never produces in the inelastic portion of its demand curve. True or false? Why? (b) Draw a figure showing a monopolist producing at the lowest point on its long-run average cost curve. (c) What is third degree price discrimination? Why does a monopolist practice it? What are the conditions are necessary for the monopolist to be able to practice it? Give a real-world example of third degree price discrimination? (c) If the price elasticity of demand is -3 in market 1 and -2 in market 2 and the price in market 1 is $12, what price should a monopolist practicing third degree price discrimination set in market 2?arrow_forwardWhich of the following best explains why the monopolist’s marginal revenue is less than the sales price?A) To sell more units, the monopolist must increase the price on all units sold.B) As the monopolist expands output, its total revenue always will decline.C) When the monopolist reduces price in order to sell more units, it must lower the price of units that could otherwise have been sold at a higher price.D) When a firm has a monopoly, consumers have no choice other than to pay the price set by the monopolist.arrow_forward

- Market research shows that a particular monopolist faces a market demand function given byIts cost function isP (Q) = 50 - 2Q.C(Q)= 47 + 10Q What is the monopoly market price and quantity? What is the monopolist’s profit? What is consumer surplus at the monopoly price? What would the price and quantity be in this market be if the monopolist behaved as in perfect competition? What is the consumer surplus in the case of perfect competition? Which is higher and why? What is the “social cost” of monopoly?arrow_forwardA monopolist has a cost function given by C(y)=y2 and faces a demand curve given by P(y) = 120-y. If you impose a lump sum tax of £100 on this monopolist, what will be the impact on output? Explain your calculations and the intuition behind your result.arrow_forwardA monopolist is deciding how to allocate output between two geographically separated markets. The demand curve for the firm's output in each market is: P1 = 4,000 - 100Q1 P2 = 2,000 - 50Q2 Where P1 and P2 are the prices of the product in each market and Q1 and Q2 are the amounts sold in each market. The firm's marginal cost curve is: MC = 25Q where Q is the firm's entire output (Q = Q1 + Q2) a) how many units should the firm sell in each market? (Keep Q1 and Q2 in decimal form) b) What price should it charge in the first market? (Use Q1 in decimal form) c) What price should it charge in the second market? ( Use Q2 in decimal form)arrow_forward

- The following graph gives the demand (D) curve for water services in the fictional town of Streamship Springs. The graph also shows the marginal revenue (MR) curve, the marginal cost (MC) curve, and the average total cost (ATC) curve for the local water company, a natural monopolist. On the following graph, use the black point (plus symbol) to indicate the profit-maximizing price and quantity for this natural monopolist. PRICE (Dollars per hundred cubic feet) 40 36 32 28 24 20 0 0 1 2 3 5 6 7 8 QUANTITY (Hundreds of cubic feet) MR 4 True ATC MC O False 9 10 D The water company is experiencing economies of scale. Which of the following statements are true about this natural monopoly? Check all that apply. + Monopoly Outcome The water company must own a scarce resource. It is more efficient on the cost side for one producer to exist in this market rather than a large number of producers. In order for a monopoly to exist in this case, the government must have intervened and created it.…arrow_forwardIn the following table, enter the price and quantity that would arise in a competitive market; then enter the profit-maximizing price and quantity that would be chosen if a monopolist controlled this market. Market Structure Price Quantity (Dollars) (Hot dogs) Competitive Monopolyarrow_forwardGraphically show a monopoly firm that currently sells 250 units of output at a price of $60/unit, where the marginal revenue of the 250th unit is $40, the marginal cost of the 250th unit is $50, and the average total cost at 250 units is $60. [Hint: Based on the information given, is the quantity you’re asked to show the profit-maximizing quantity? Think about what has to be true for profit-maximization.] Based on the graph and assuming the firm attempts to profit maximize (and succeeds), what would happen to price, quantity, MR, MC, and ATC? (rise, fall, or stay the same?)arrow_forward

- A monopolist has discovered that the inverse demand function of a person with income Y for the monopolist’s product is P = 0.002Y-Q where P is the price, Y the income, and Q is the output. The monopolist can observe the incomes of its consumers and hence vary its price accordingly. The monopolist has a total cost function C(Q) = 100Q. A. Calculate the profit maximising price as a function of the consumer’s income Y carefully explaining all the steps in the derivation of the formula. B. A monopolist has a constant marginal cost of £2 per unit and no fixed costs. He faces two separate markets in the United States and in the UK. The goods sold in one market are never resold in the other. He sets one price P1 for the US market and another price P2 for the UK market (both measured in £). The demand in the United States is given by Q1=7,000-700P1 and the demand in the UK is given by Q2=1,200-200P1. Calculate the profit maximising output produced and price charged in each country by the…arrow_forwardThe graph above shows the cost and revenue curves for a natural monopoly that provides electrical power to the town of Fanaland. If unregulated, the monopolist operates to maximize its profit. (a) Identify the monopolist’s profit-maximizing quantity and price. (b) Assume the town government of Fanaland regulates the monopolist’s price to achieve the allocatively efficient quantity. What price would the government set in order to achieve the allocatively efficient quantity? (c) Will producing the allocatively efficient quantity be economically feasible for the monopolist? Explain. (d) Suppose instead the town government wants to regulate the monopolist to earn zero economic profit. What price would the government set to have the monopolist earn zero economic profit? (e) Based on your answer to part (d), will the deadweight loss increase, decrease, or stay the same as that of the unregulated monopolist? Explain.arrow_forwardQuestion 2: Suppose a monopoly firm produces bicycles and can sell 10 bicycles per month at a price of $700 per bicycle. In order to increase sales by one bicycle per month, the monopolist must lower the price of its bicycles by $100 to $600 per bicycle. What is the marginal revenue of the eleventh bicycle?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education