ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

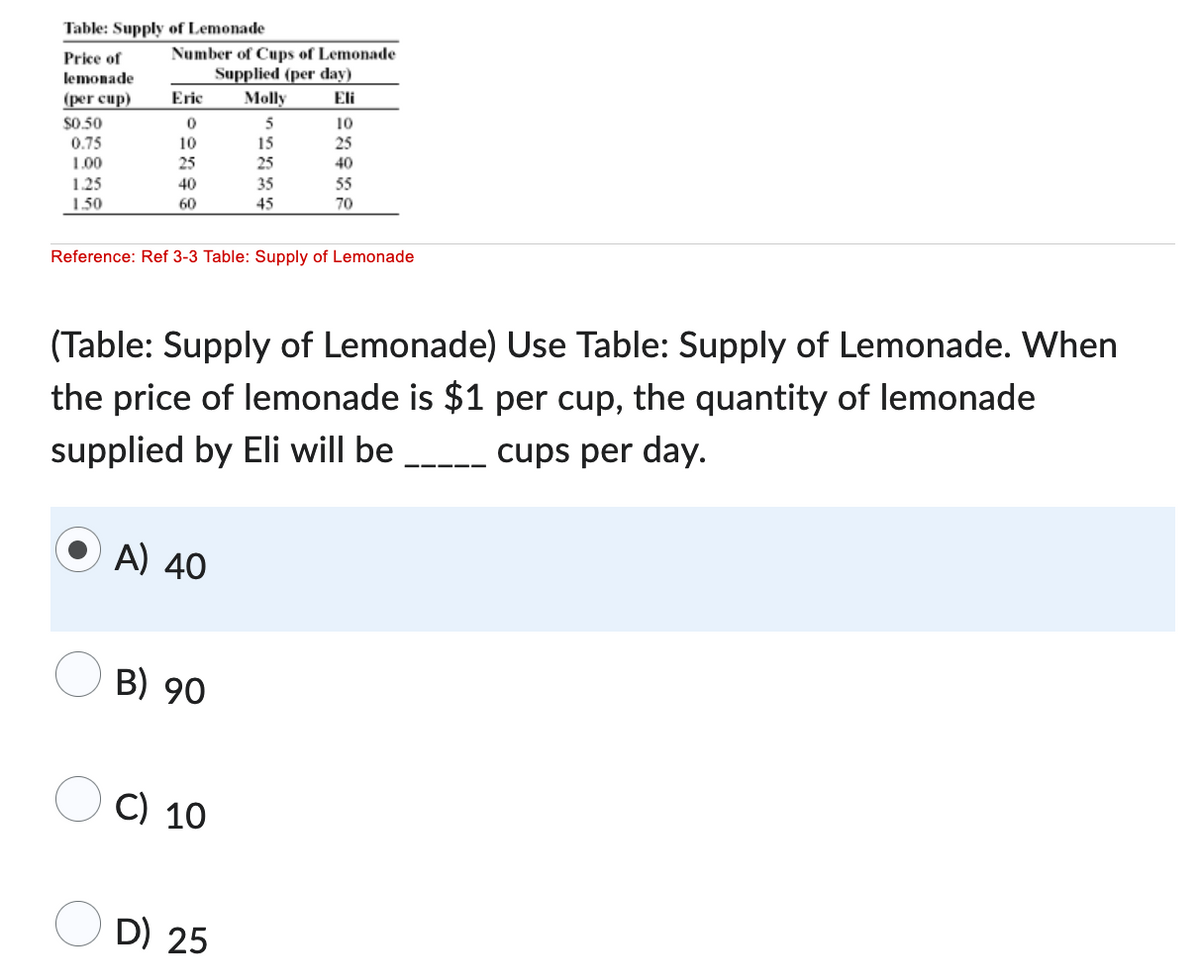

Transcribed Image Text:Table: Supply of Lemonade

Price of

lemonade

(per cup)

$0.50

0.75

1.00

1.25

1.50

Number of Cups of Lemonade

Supplied (per day)

Eli

Eric

0

10

25

40

60

A) 40

B) 90

Molly

5

Reference: Ref 3-3 Table: Supply of Lemonade

C) 10

15

25

(Table: Supply of Lemonade) Use Table: Supply of Lemonade. When

the price of lemonade is $1 per cup, the quantity of lemonade

supplied by Eli will be

cups per day.

D) 25

35

45

10

25

40

55

70

Expert Solution

arrow_forward

Step 1

Supply in economics is defined as the total amount of a given product or service a supplier offers to consumers at a given period and a given price level. It is usually determined by market movement.

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- (Table: Lembas bread) The table shows the maximum consumer willingness to pay for Lembas bread. Consumer Maximum willingness to pay for Lembas bread Frodo $11.65 Sam Mary Pippin 17.99 12.99 16.75 If the market price for bread is $12.00, what is the total consumer surplius in this market? Do not include dollar sign in your answer. 11.38arrow_forwardPrice (dollars per dozen) 30 50 Quantity supplied (dozens per day) 8 12 The table gives some data on the supply of roses in a small town. When the price rises from $15 a dozen to $25 a dozen, the elasticity of supply is O 0.80. O 0.20 O 1.25. O 5.00.arrow_forwardModule 5 Homework i 2 eBook Refer to the figure. Price (dollars) 10 8 7 4 3 2 1 0 Market for Artichokes 50 100 D 150 S 200 Quantity (pounds of artichokes) 250 Tools PS Saved Ⓡ The graph represents the market for artichokes (in pounds per week) at a Midwest farmers' market. Suppose the equilibrium price of artichokes is $3 per pound and the equilibrium quantity is 100 pounds of artichokes per week. Using the graph, show the area representing producer surplus in this market, and then determine how much producer surplus will be generated by the market each week. Instructions: Use the tool provided “PS” to illustrate this area on the graph. Producer surplus: Help Save &arrow_forward

- Indicate the answer choice that best completes the statement or answers the question. 1. (Figure: Demand for jazz shows) The graph shows Jayden's monthly demand curve for live music at a small, local venue. Price per show ($) $20 $18 $16 $14 $12 $10 $8 $6 $4 $2 $0 Demand 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 Quantity of shows If Jayden currently attends six shows per month, what is probably TRUE? a. The price of a concert ticket is between $9 and $12. b. Jayden does not have enough income to go to more than six shows per month. c. Each concert provides Jayden with the same marginal benefit. d. If the price rose to $18, Jayden would not attend any concerts. Page 1arrow_forward13. Application Problem Use the table to find the (a) Linear Supply equation: P = mx + b (b) Linear Demand equation: P = mx + b Prof herbert (c) The equilibrium point. This is the point where the two lines meet. Supply In millions Demand in millions Year Price $ per unit 2002 2003 340 270 2,22 370 250 | 2.72 Hint to finding solution (a) Find the slopes for demand and supply using the point (x,p) given in the table (b) Use point slope equation substituting the slope obtained and one point (x,p) to obtain the requires demand and supply equations respectively. (c) Graph the two equations, The point (x,p) the two lines meet is the equilibrium point meaning when Demand = Supply. (x,p) 14. Modeling problem Medgar Evers College bookstore sells a custom printed T-Shirt. The cost function is given as C(x) = 250 + 4.50x. (a) What is the slope in the cost function (b) Interpret the meaning of the slope in the context of this problem.arrow_forwardFigure: The Demand and Supply of Wheat Price (per bushel) $10 9 8 7 6 5 4 3 2 1 0 Reference Ref 3-6 2 B. $5: 5,000 C. 56; 7,000 D. $8; 8,000 4 8 10 12 Quantity of wheat (thousands of bushels per period) 6 (Figure: The Demand and Supply of Wheat) Look at the figure The Demand and Supply of Wheat. If there is an increase in demand of 2,000 bushels at each price, the equilibrium price and quantity will be and bushels, respectively. A. $7; 7,000arrow_forward

- I already did the graph but I need help with question 17 to 22arrow_forwardRefer to the figure, Price (dollars) 600 550 500 450 400 350 300 250 200 150 100 50 0 Market for Game Consoles S 10 20 30 40 50 60 70 80 90 100110 Quantity Toola DL 0 O Use the graph to show the area representing the deadweight loss, and then determine the deadweight loss created as a result of setting the price at $150. Instructions: Use the tool provided "DL to illustrate this area on the graph. Deadweight loss: $arrow_forward12LGjjfiV9KIUa7A14QC7gvvPrKFtW6ZwP60WrVE/edit AP 100% PRICE Dolars perp Answer Price ($) 10. Using the graph below, determine the equilibrium price and quantity of pens. 0000 5000- 3000 2000- Normal text Answer: RUBRIC Worksheet 2 Scenario 11. Using the graph below, determine the approximate equilibrium price and quantity of soap. Supety 3 QUANTITY ons of pens) Demand Curve Arial Supply Curve Cartoon P Quantity Supplied Price determination AND PRICE 11 Demand + B I UA Aarrow_forward

- Question 1 The table shows market data for mobile phone kits. The original equilibrium price is GHC 23. Price GHO Quantity Quantity New demanded supplied per month per (000) 56 month (000) 7 8 9 8 7 25 24 23 22 21 9 As a result of a successful advertising campaign, demand increased by 3000 mobile phone kits at all prices. At the same time production costs fell leading to an increase in supply of 1000 mobile phone]kits at all prices. la) Calculate the new equilibrium price and quantity following the successful advertising campaign and fall in production costs. New quantity quantity demanded supplied 6 5 per month per month (000) (000) 1b) Consider the retail market for petrol. Do you believe that this market operates under conditions of imperfect competition? Explain with reasons for your answers. 1c) Suppose a producer sells 1,000 units of a product at GHC5 per unit one year, 2,000 units at GHC8 the next year, and 3,000 units at GHC10 the third year. Is this evidence that the law of…arrow_forward4. Which of the following statements is (are) correct? (x) When quantity supplied responds very little to changes in price, supply is said to be inelastic. (y) If the quantity supplied changes substantially when the price of the good changes a small amount, then the coefficient of price elasticity of supply is a number larger than one and supply is elastic. (z) Holding all else constant, if a paper manufacturer increases production by 12 percent when the market price of paper increases by 15 percent, then the price elasticity of supply must be inelastic since the coefficient of price elasticity of supply is equal to 0.80. A. (x), (y) and (z) C. В. (x) and (y) only (x) and (z) only E. (x) only D. (y) and (z) onlyarrow_forwardch QUESTION 55 P ($ per gallon) $2.20 $1.80 $1.40 $1.20 $1.00 $0.60 Excess supply or surplus O Equilibrium price is If supply is 680, price is If demand is 700, price is S --- An above-equilibrium price E - Equilibrium price A below-equilibrium price Excess demand or shortage 300 400 500 600 700 800 900 Quantity of Gasoline (millions of gallons) 113 hparrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education