ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

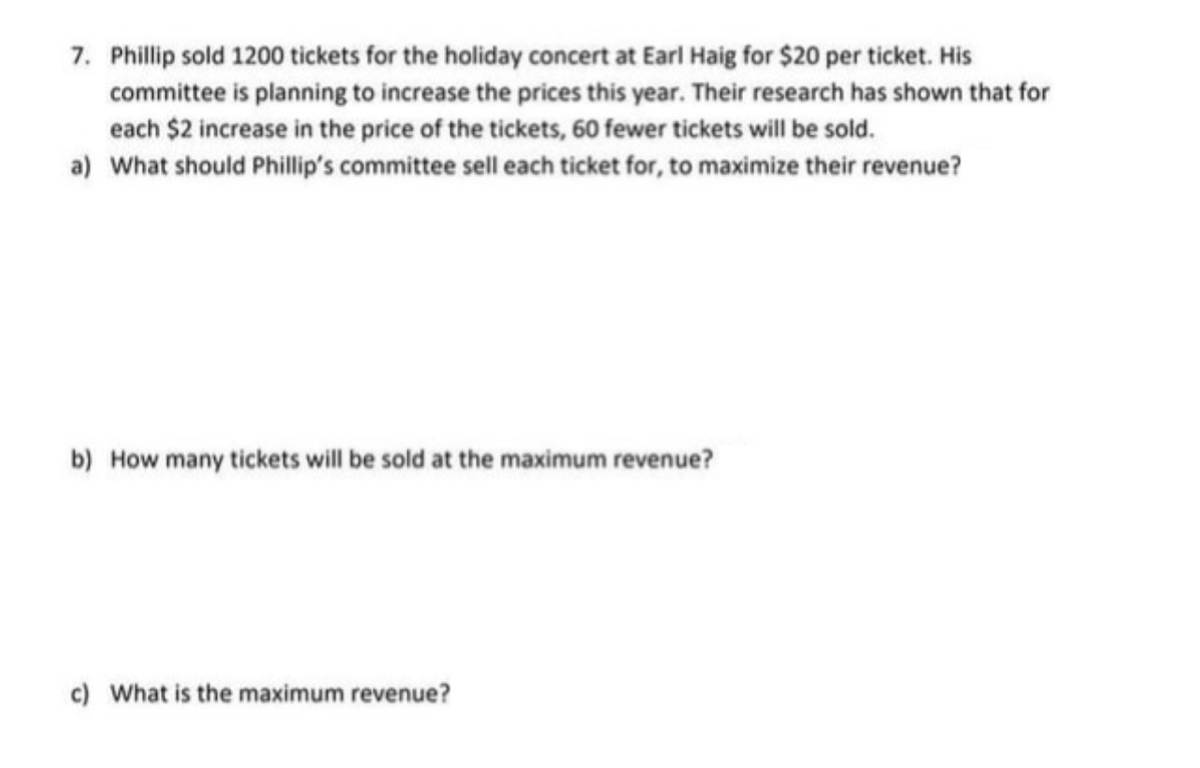

Transcribed Image Text:7. Phillip sold 1200 tickets for the holiday concert at Earl Haig for $20 per ticket. His

committee is planning to increase the prices this year. Their research has shown that for

each $2 increase in the price of the tickets, 60 fewer tickets will be sold.

a) What should Phillip's committee sell each ticket for, to maximize their revenue?

b) How many tickets will be sold at the maximum revenue?

c) What is the maximum revenue?

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- 2. Thrift store clothing is considered an inferior good. The demand for thrift store clothing decreases as the consumer's income decreases decreases as the price of a substitute increases increases as the consumer's income decreases increases as the consumer's income increasesarrow_forwardExercise 2. The demand curve for a product is given Qd = 1500 − 5Px − 0.2Pz by where Pz = $300. What is the own-price elasticity of demand when Px = $200? Is demand elastic or inelastic at this price? What would happen to the firm’s revenue if it decided to charge a price below $200? What is the own-price elasticity of demand when Px = $125? Is demand elastic or inelastic at this price? What would happen to the firm’s revenue if it decided to charge a price above $125? What is the cross-price elasticity of demand between good X and good Z when Px =$125? What about when Px = $200? Are goods X and Z substitutes or complements?arrow_forward#4 Determining the price elasticity of demand of a product involves all of the following factors, but NOT the total number of firms in a market. the availability of substitutes to the product. whether the product is a luxury or a necessity.arrow_forward

- Price (dollars) 8 7 D. 5 10 15 20 25 30 35 Quantity (units per year) In the figure above, when the price falls from $8 to $7, total revenue A) decreases from $210 to $120 so demand is inelastic. B) increases from $120 to $210 so demand is inelastic. C) decreases from $210 to $120 so demand is elastic. D) increases from $120 to $210 so demand is elastic. 6arrow_forwarda. Define price elasticity of demand, and cross-price elasticity of demand. b. If the cross-price elasticity of demand between two goods is negative (EXY<0), what can be said about the relationship between these two goods? c. If the Boston Red Sox know that the demand for their tickets is elastic (ED>1), should they increase or decrease the price of their tickets in order to increase total revenue? Explain.arrow_forward2) Ernesto is looking to purchase a new vehicle as his income has increased from $2,000 per month to $3,000 per month, so his purchase increases from 0 to 1 vehicle. He see's a new Mercedes Benz that decreased its price from $45,000 to $42,000. What is Ernesto's income elasticity of demand for a Mercedes Benz vehicle?arrow_forward

- Question 4 (A) Explain the factors that affect the price elasticity of demand for a product.arrow_forwarda. How much would the firm’s revenue change if it lowered price from $12 to $10? Is demand elastic or inelastic in this range? Revenue change: $ Demand is in this range. b. How much would the firm’s revenue change if it lowered price from $4 to $2? Is demand elastic or inelastic in this range? Revenue change: $ Demand is in this range. c. What price maximizes the firm’s total revenues? What is the elasticity of demand at this point on the demand curve? Price that maximizes total revenues: $ Demand is at this point.arrow_forward8. Substitutes, complements, or unrelated? You work for a marketing firm that has just landed a contract with Run-of-the-Mills to help them promote three of their products: penguin pops, flopsicles, and kipples. All of these products have been on the market for some time, but, to entice better sales, Run-of-the-Mills wants to try a new advertisement that will market two of the products that consumers will likely consume together. As a former economics student, you know that complements are typically consumed together while substitutes can take the place of other goods. Run-of-the-Mills provides your marketing firm with the following data: When the price of penguin pops decreases by 10%, the quantity of flopsicles sold decreases by 9% and the quantity of kipples sold increases by 9%. Your job is to use the cross-price elasticity between penguin pops and the other goods to determine which goods your marketing firm should advertise together. Complete the first column of the following…arrow_forward

- (i) InfoConsider the three demand functions in the file Elasticity. Calculate the elasticities of these three demand functions when the price of the product increases from P = $200 per unit to P = $400 per unit. Enter the elasticities as positive numbers. Elasticity of the red demand function = Elasticity of the green demand function = Elasticity of the blue demand function =..arrow_forwardSuppose the own price elasticity of demand for good X is −2, its income elasticity is 3, its advertising elasticity is 4, and the cross-price elasticity of demand between it and good Y is −6. Determine how much the consumption of this good will change if:Instructions: Enter your responses as percentages. If you are entering a negative number, be sure to use a (−) sign.a. The price of good X decreases by 5 percent. percentb. The price of good Y increases by 10 percent. percentc. Advertising decreases by 2 percent. percentd. Income increases by 3 percent. percentarrow_forwardWhy do we say goods become more elastic over time? Question 9 options: people's incomes will increase, and so the elasticity of demand decreases. the good's price will have a chance to return to its previous level. people can find more substitutes, and so the elasticity of demand decreases. people can find more substitutes, and so the elasticity of demand increases.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education