ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

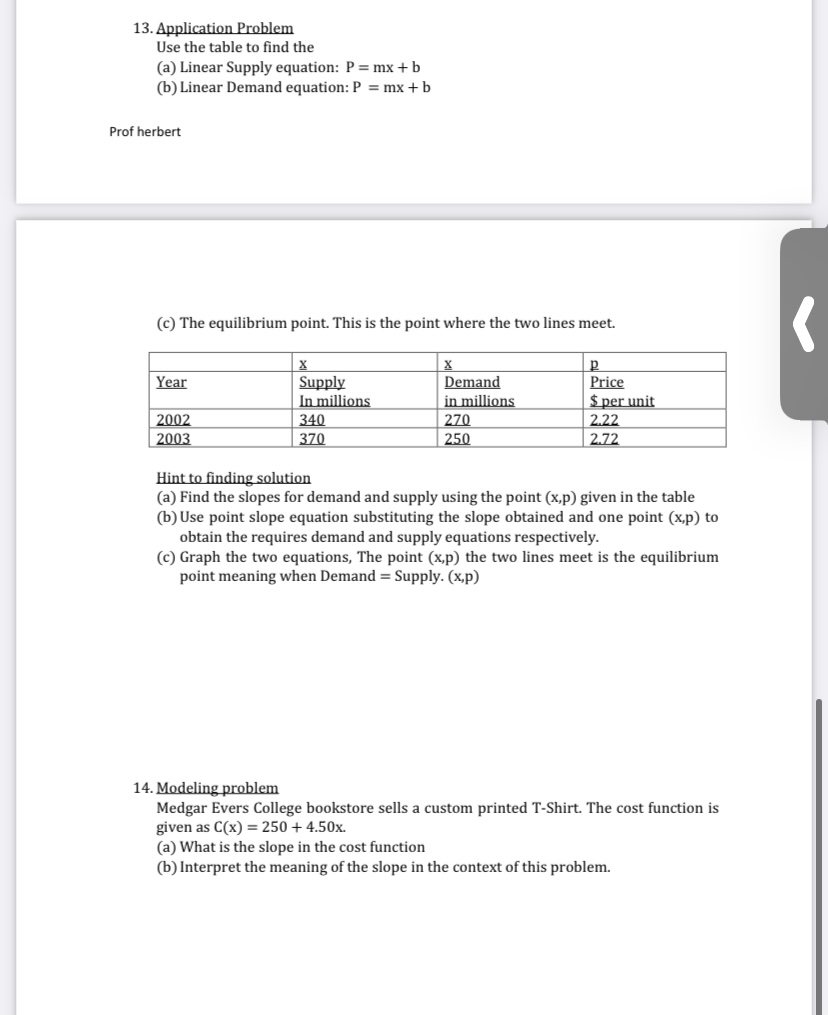

Transcribed Image Text:13. Application Problem

Use the table to find the

(a) Linear Supply equation: P = mx + b

(b) Linear Demand equation: P = mx + b

Prof herbert

(c) The equilibrium point. This is the point where the two lines meet.

Supply

In millions

Demand

in millions

Year

Price

$ per unit

2002

2003

340

270

2,22

370

250

| 2.72

Hint to finding solution

(a) Find the slopes for demand and supply using the point (x,p) given in the table

(b) Use point slope equation substituting the slope obtained and one point (x,p) to

obtain the requires demand and supply equations respectively.

(c) Graph the two equations, The point (x,p) the two lines meet is the equilibrium

point meaning when Demand = Supply. (x,p)

14. Modeling problem

Medgar Evers College bookstore sells a custom printed T-Shirt. The cost function is

given as C(x) = 250 + 4.50x.

(a) What is the slope in the cost function

(b) Interpret the meaning of the slope in the context of this problem.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 1 images

Knowledge Booster

Similar questions

- Subject : Engineering Economics Please write handwritten Answerarrow_forwardimg' (a If po increases, what happens to the demand and supply of public transportation (shifts left/shifts right/doesn’t change) What happens to the equilibrium quantity and price for public transportation? (increase/decrease) (b)At a given price p, as oil becomes more expensive (po increases), does the (own) price elasticity of demand for public transportation increase / decrease / stay the same? (c) Calculate the cross-price elasticity of public transportation demand with respect to the oil price po, at the point p = 1 and po = 2. Are the two goods (public transportation and oil) substitutes or complements, or unrelated?arrow_forwardTyped plzzzz And Asap Thanksarrow_forward

- Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardGive every questions answer and take likearrow_forwardI cant seem to remeber the formula to use to fill out S2 and D2arrow_forward

- Please let me know seftuon A) if the input price would rise or fallarrow_forwardNote:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardA Define "supply." 9.( The definition of supply is very similar to that of demand. Supply is a schedule which shows the various amounts of a product sellers are at each price in a series of possible prices during a specified period, other things being equal. Supply portrays relationship between ( related either in the table or in the (graph). ) and ( ) to produce and offer for sale ) and ( ), they are (directly, inversely) S Describe and give a reason for the law of supply. The law of supply indicates that producers will produce and sell (more, less ) of their product at a high price than at a low price. This means that there is a positive, negative ) relationship between price and quantity supplied. The basic explanation is that, given product costs, a higher price means greater profits and thus more incentive for business to increase the quantity supplied.arrow_forward

- Nonearrow_forwardPRICE (Dollars per unit) 350 225 175 50 0 12 +--- Region Between X and Y Between W and X Between Y and Z Z True False 42 54 QUANTITY (Units) For each of the regions listed in the following table, use the midpoint method to identify if the demand for this good is elas elastic, or inelastic. 84 W Demand - Elastic Inelastic Unit Elastic True or False: The slope of the demand curve is equal to the value of the price elasticity of demand.arrow_forwardhe quantity demanded each month of Russo Espresso Makers is 250 when the unit price is $136. The quantity demanded ach month is 1000 when the unit price is $106. The suppliers will market 750 espresso makers when the unit price is $80 er higher. At a unit price of $100, they are willing to market 2250 units. Both the supply and demand equations are known o be linear. (a) Find the demand equation. -1 -x + 146 25 p = (b) Find the supply equation. 1 x+ 70 p = 75* (c) Find the equilibrium quantity and the equilibrium price. |× unitsarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education