FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

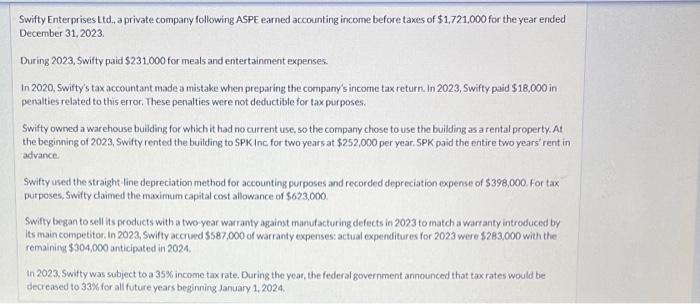

Transcribed Image Text:Swifty Enterprises Ltd., a private company following ASPE earned accounting income before taxes of $1,721,000 for the year ended

December 31, 2023.

During 2023, Swifty paid $231.000 for meals and entertainment expenses.

In 2020, Swifty's tax accountant made a mistake when preparing the company's income tax return. In 2023, Swifty paid $18,000 in

penalties related to this error. These penalties were not deductible for tax purposes.

Swifty owned a warehouse building for which it had no current use, so the company chose to use the building as a rental property. At

the beginning of 2023, Swifty rented the building to SPK Inc for two years at $252,000 per year. SPK paid the entire two years rent in

advance.

Swifty used the straight-line depreciation method for accounting purposes and recorded depreciation expense of $398,000. For tax

purposes, Swifty claimed the maximum capital cost allowance of $623,000.

Swifty began to sell its products with a two-year warranty against manufacturing defects in 2023 to match a warranty introduced by

its main competitor. In 2023, Swifty accrued $587,000 of warranty expenses: actual expenditures for 2023 were $283,000 with the

remaining $304,000 anticipated in 2024.

In 2023, Swifty was subject to a 35% income tax rate. During the year, the federal government announced that tax rates would be

decreased to 33% for all future years beginning January 1, 2024.

Transcribed Image Text:(a)

Your answer is incorrect.

Calculate the amount of any permanent differences for 2023.

Permanent differences $

eTextbook and Media

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Sunland Services Ltd. follows ASPE and had earned accounting income before taxes of $520,000 for the year ended December 31, 2023. During 2023, Sunland paid $77,000 for meals and entertainment expenses. In 2020, Sunland's tax accountant made a mistake when preparing the company's income tax return. In 2023, Sunland paid $10,500 in penalties related to this error. These penalties were not deductible for tax purposes. Sunland owned a warehouse building for which it had no current use, so the company chose to use the building as a rental property. At the beginning of 2023, Sunland rented the building to Trung Inc. for two years at $64,500 per year. Trung paid the entire two years' rent in advance. Sunland used the straight-line depreciation method for accounting purposes and recorded depreciation expense of $286,200. For tax purposes, Sunland claimed the maximum capital cost allowance of $431,400. This asset had been purchased at the beginning of the year for $3,004,400. In 2023, Sunland…arrow_forwardPearl Inc. incurred a net operating loss of $455,000 in 2020. The tax rate for all years is 20%. Assume that it is more likely than not that the entire net operating loss carryforward will not be realized in future years. Prepare all the journal entries necessary at the end of 2020. (Credit account titles are automatically indented when amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter 0 for the amounts.)arrow_forwardUramilabenarrow_forward

- Flint Enterprises Ltd., a private company following ASPE earned accounting income before taxes of $1,712,000 for the year ended December 31, 2020. During 2020, Flint paid $240,000 for meals and entertainment expenses. In 2017, Flint’s tax accountant made a mistake when preparing the company’s income tax return. In 2020, Flint paid $17,000 in penalties related to this error. These penalties were not deductible for tax purposes. Flint owned a warehouse building for which it had no current use, so the company chose to use the building as a rental property. At the beginning of 2020, Flint rented the building to SPK Inc. for two years at $260,000 per year. SPK paid the entire two years’ rent in advance. Flint used the straight-line depreciation method for accounting purposes and recorded depreciation expense of $396,000. For tax purposes, Flint claimed the maximum capital cost allowance of $621,000. Flint began to sell its products with a two-year warranty against manufacturing…arrow_forwardJ-Matt, Inc., had pretax accounting income of $331,000 and taxable income of $376,000 in 2021. The only difference between accounting and taxable income is estimated product warranty costs of $45,000 for sales in 2021. Warranty payments are expected to be in equal amounts over the next three years (2022–2024) and will be tax deductible at that time. Recent tax legislation will change the tax rate from the current 25% to 20% in 2023. Determine the amounts necessary to record J-Matt’s income taxes for 2021 and prepare the appropriate journal entry.arrow_forwardAt the end of 2019, its first year of operations, Beattie Company reported taxable income of $39,000 and pretax financial income of $35,000. The difference is due to the way the company handles its warranty costs. For tax purposes, Beattie deducts the warranty costs as they are paid. For financial reporting purposes, Beattie provides for a year-end estimated warranty liability based on future expected costs. Beattie is subject to a 30% tax rate for 2019, and no change in the tax rate has been enacted for future years. Based on verifiable evidence, the company decides it should establish a valuation allowance of 60% of its ending deferred tax asset. Required: 1. Prepare Beattie’s income tax journal entry at the end of 2019. 2. Prepare the lower portion of Beattie’s 2019 income statement.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education