Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

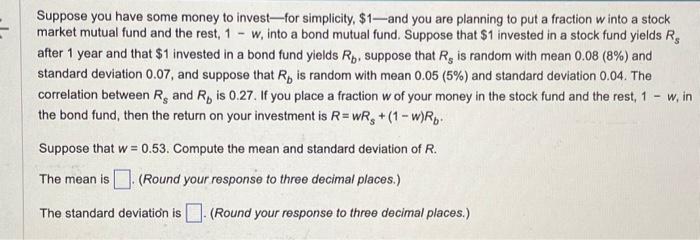

Transcribed Image Text:Suppose you have some money to invest-for simplicity, $1-and you are planning to put a fraction w into a stock

market mutual fund and the rest, 1 w, into a bond mutual fund. Suppose that $1 invested in a stock fund yields R

after 1 year and that $1 invested in a bond fund yields Rp. suppose that R, is random with mean 0.08 (8%) and

standard deviation 0.07, and suppose that R, is random with mean 0.05 (5%) and standard deviation 0.04. The

correlation between R. and R, is 0.27. If you place a fraction w of your money in the stock fund and the rest, 1

the bond fund, then the return on your investment is R = wR₂ + (1-w)Rp.

-

Suppose that w = 0.53. Compute the mean and standard deviation of R.

The mean is. (Round your response to three decimal places.)

The standard deviation is. (Round your response to three decimal places.)

w, in

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- You own a portfolio equally invested in a risk-free asset and two stocks. One of has risky as has a beta of 1.6, and the total portfolios is equally as risky as the market. What's the beta of the second stock?arrow_forwardPortfolio Suppose rA ~ N (0.05, 0.01), rB ~ N (0.1, 0.04) with pA,B = 0.2 where rA and rB are CCR’s. a) Suppose you construct a portfolio with 50% for A and 50% for B. Find the variance of the portfolio CCR. b) Find the portfolio expected gross return. c) Find the expected portfolio CCR.arrow_forwardIn the following exercise, separate the investments according to the type of Keynesian demand they are: Transactions (0% to 5%), Precautionary (6% to 9%), and Speculative demand (greater than 10%). Investment in each category has the same risk. So you want to invest in the highest return for the same risk. Take each demand type and choose the highest return and put that amount into the investment. For example, if Bond fund A has a return of 4% and Fund B has a return of 5%, they have the same risk, so you would put $70 into bond fund B. You have the following investments Opportunities ad returns. Fidelity Bonds 11% Fidelity Magellan 9% Putman Bonds one 4% Putman bonds Two 12% Growth Stock One 15% Growth and Income 8% Income Fund 3% Putman Growth…arrow_forward

- After learning the course, you divide your portfolio into three equal parts (i.e., equal market value weights), with one part in Treasury bills, one part in a market index, and one part in a mutual fund with beta of 1.11. What is the beta of your overall portfolio?arrow_forwardAfter learning the course, you divide your portfolio into three equal parts (i.e., equal market value weights), with one part in Treasury bills, one part in a market index, and one part in a mutual fund with beta of 0.77. What is the beta of your overall portfolio?arrow_forwardYou have estimated the single index model (SIM) fund B and found that its alpha and beta are 0.035 and 1.1 respectively. The standard deviation of Fund B's excess returns is 30% and the market portfolio excess returns have a standard deviation of 20%. What's the information ratio of Fund B?arrow_forward

- If an investor that owns a portfolio with 3 stocks increases their portfolio to 30 stocks, which of the following is MOST LIKELY to happen? Select one: a. risk will increase b. risk would decrease c. Systematic risk would increase d. return would increasearrow_forwardConsider the following information for stocks A, B, and C. The returns on the three stocks are positively correlated, but they are not perfectly correlated. (That is, each of the correlation coefficients is between 0 and 1.) Stock Expected Return Standard Deviation Beta A B с 9.30% 10.35 12.10 14% 14 14 0.8 1.1 1.6 Fund P has one-third of its funds invested in each of the three stocks. The risk-free rate is 6.5%, and the market is in equilibrium. (That is, required returns equal expected returns.) a. What is the market risk premium (гM-TRF)? Round your answer to one decimal place. % b. What is the beta of Fund P? Do not round intermediate calculations. Round your answer to two decimal places. c. What is the required return of Fund P? Do not round intermediate calculations. Round your answer to two decimal places. % d. What would you expect the standard deviation of Fund P to be? I. Less than 14% II. Greater than 14% III. Equal to 14% -Select-arrow_forwardConsider the information on the market, the risk-free asset, and a mutual fund. You want to build a two-asset portfolio comprising the market portfolio and the risk-free asset such that your portfolio beta is the same as the mutual fund. What is the portfolio weight on the market in your portfolio? Mutual Fund Market Risk Free E(k) 11.1% 8.5% 2.0% Beta 1.4 1 0arrow_forward

- After learning the course, you divide your portfolio into three equal parts (i. e.. equal market value weights), with one part in Treasury bills, one part in a market index, and one part in a mutual fund with beta of 1.32. What is the beta of your overall portfolio?arrow_forwardSuppose you manage an equity fund with the following securities. Use the following data to help build an active portfolio. Input Data Vogt Industries Isher Corporation Hedrock, Incorporated Alpha 0.012 0.006 0.016 Beta 0.277 1.015 1.630 Standard Deviation 0.156 0.168 0.181 Residual Standard Deviation 0.117 0.048 0.113 Information Ratio 0.1026 0.1250 0.1416 Alpha/Residual Variance 0.877 2.604 1.253 Market Data S&P 500 Treasury Bills Expected Raturn 12.00% 2.50% Standard Deviation 20.00% 0.00% Required: Using the information in the table above, please first calculate the initial weight of each stock in an active portfolio, using the Treynor Black approach. Then adjust each weight for beta. (Use cells A5 to D14 from the given information to complete this question.) Treynor-Black Model Vogt Industries Isher Corporation Hedrock, Incorporated…arrow_forwardAssume that you formed a portfolio of three stocks, X, Y, and Z. The stock X's beta is 1.5, stock Y's beta is 2, and stock Z's beta is 0.5. If the weight of your wealth invested in stock X is 0.4, the weight invested in stock Y is 0.2, find the portfolio's beta.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education