ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

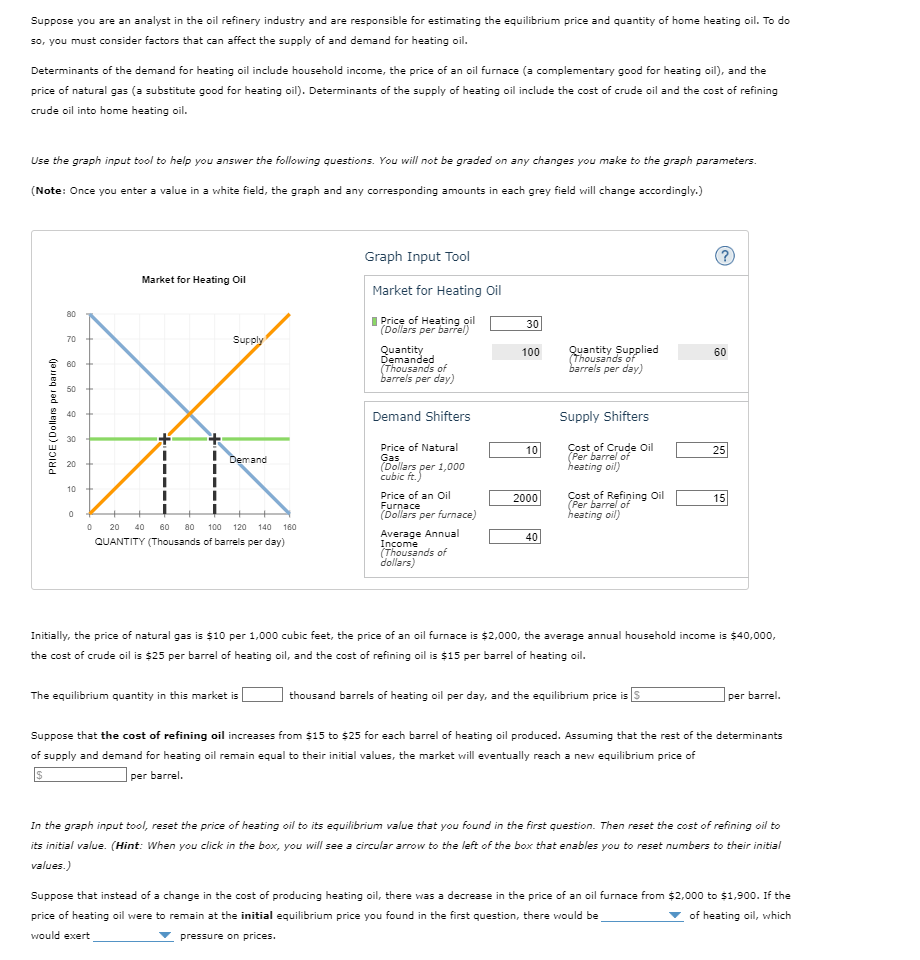

Transcribed Image Text:Suppose you are an analyst in the oil refinery industry and are responsible for estimating the equilibrium price and quantity of home heating oil. To do

so, you must consider factors that can affect the supply of and demand for heating oil.

Determinants of the demand for heating oil include household income, the price of an oil furnace (a complementary good for heating oil), and the

price of natural gas (a substitute good for heating oil). Determinants of the supply of heating oil include the cost of crude oil and the cost of refining

crude oil into home heating oil.

Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to the graph parameters.

(Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly.)

PRICE (Dollars per barrel)

80

70

60

50

40

30

20

10

0

0

Market for Heating Oil

Supply

Demand

20 40 60 80 100 120 140 160

QUANTITY (Thousands of barrels per day)

Graph Input Tool

Market for Heating Oil

Price of Heating oil

(Dollars per barrel)

The equilibrium quantity in this market is

Quantity

Demanded

(Thousands of

barrels per day)

Demand Shifters

Price of Natural

Gas

(Dollars per 1,000

cubic ft.)

Price of an Oil

Furnace

(Dollars per furnace)

Average Annual

Income

(Thousands of

dollars)

30

100

10

2000

40

Quantity Supplied

of

barrels per day)

Supply Shifters

Cost of Crude Oil

(Per barrel of

heating oil)

Cost of Refining Oil

(Per barrel of

heating oil)

(?

thousand barrels of heating oil per day, and the equilibrium price is S

60

25

Initially, the price of natural gas is $10 per 1,000 cubic feet, the price of an oil furnace is $2,000, the average annual household income is $40,000,

the cost of crude oil is $25 per barrel of heating oil, and the cost of refining oil is $15 per barrel of heating oil.

15

per barrel.

Suppose that the cost of refining oil increases from $15 to $25 for each barrel of heating oil produced. Assuming that the rest of the determinants

of supply and demand for heating oil remain equal to their initial values, the market will eventually reach a new equilibrium price of

$

per barrel.

In the graph input tool, reset the price of heating oil to its equilibrium value that you found in the first question. Then reset the cost of refining oil to

its initial value. (Hint: When you click in the box, you will see a circular arrow to the left of the box that enables you to reset numbers to their initial

values.)

Suppose that instead of a change in the cost of producing heating oil, there was a decrease in the price of an oil furnace from $2,000 to $1,900. If the

price of heating oil were to remain at the initial equilibrium price you found in the first question, there would be

of heating oil, which

would exert

pressure on prices.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 1 steps

Knowledge Booster

Similar questions

- A certain manufacturer has determined that the weekly demand and supply functions for their product are given by the equations: supply: p=-2x² +80 demand: p = 15x+30 where z represents the quantity demanded in units of a thousand and p is the unit price in dollars. Find the market equilibrium (equilibrium price and equilibrium quantity).arrow_forwardConsider the market for pens. Suppose that the number of students who are allergic to the rubber used in pencil erasers increases, leading more students to switch from pencils to pens in school. Further, the price of ink, a major input in the pen production process, has increased sharply. On the following graph, labeled Scenario 1, indicate the effect these two events have on the demand for and supply of pens. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther. 10 P 2 1 D 10 9 3 2 1 0 Next, complete the following graph, labeled Scenario 2, by shifting the supply and demand curves in the same way that you did on the Scenario 1 graph. 0 1 2 Scenario 1 3 Scenario 2 Supply Demand Supply 5 6 QUANTITY (Millions of pens) Equilibrium Object Price Quantity Demand 7 8 9 10 -o Demand Supply Scenario 1 (?) Demand Compare both the Scenario 1…arrow_forwardIdentify the flaw in this analysis: “If more Bahamians go on a low-carb diet, the demand for pasta will fall. The decrease in the demand for pasta will cause the price of pasta to fall. The lower price, however, will then increase the demand. In the new equilibrium, Americans might end up consuming more pasta than they did initially.”arrow_forward

- Determine the equilibrium price and quantity for the following laws of demand and supply in the manufacture of computer parts Demand: 3p + 5x = 200Bid: 7p - 3x = 56arrow_forwardThe market for cod liver oil pills is characterized by the demand and supply equations: QD = 100-4P and QS = -20+2P, where P is the price per bottle and Q is the quantity of bottles. If consumers want to purchase 60 more bottles at any given price, what is the new equilibrium quantity? 30 10 40 20arrow_forwardDS Determinants of supply The following calculator shows the supply curve for sedans in an imaginary market. For simplicity, assume that all sedans are identical and sell for the same price. Two factors that affect the supply of sedans are the level of technical knowledge-in this case, the speed with which manufacturing robots can fasten bolts, or robot speed-and the wage rate that auto manufacturers must pay their employees. Initially, the graph shows the supply curve when robots can fasten 2,500 bolts per hour and autoworkers earn $25 per hour. Use the graph input tool to help you answer the following questions. You will not be graded on any changes you make to this graph. Note: Once you enter a value in a white field, the graph and any corresponding amounts in each grey field will change accordingly. PRICE (Thousands of dollars) 8 20 10 0 0 Supply 100 200 300 400 500 600 700 800 900 QUANTITY (Sedans per month) Graph Input Tool Supply for Sedans Price of a Sedan (Thousands of…arrow_forward

- Assume the demand curve for gasoline is downward sloping and the supply curve is upward sloping. Start by considering the gasoline market in 2020. Draw a graph that shows supply and demand analysis for gasoline in this city. Label the supply curve as S0; demand curve as D0; the equilibrium price as P0; and equilibrium quantity as Q0.arrow_forwardThe following graph shows the supply curve for sedans in an imaginary market. For simplicity, assume that all sedans are identical and sell for the same price. Two factors that affect the supply of sedans are the level of technical knowledge—in this case, the speed with which manufacturing robots can fasten bolts, or robot speed—and the wage rate that auto manufacturers must pay their employees. Initially, the graph shows the supply curve when robots can fasten 2,500 bolts per hour and autoworkers earn $25 per hour. Suppose that the price of a sedan increases from $21,000 to $26,000. This would cause the quantity supplied of sedans to ________ (options: increase, decrease) , which is reflected on the graph by a ________ (options: shift of, movement along) the supply curve. Suppose the workers' union negotiates a pay raise. This causes a _________ (options: leftward movement along, rightward movement along, leftward shift of, rightward shift of) the supply curve because the pay raise…arrow_forwardConsider two markets: the market for waffles and the market for pancakes. The initial equilibrium for both markets is the same, the equilibrium price is $6.50, and the equilibrium quantity is 35.0. When the price is $9.75, the quantity supplied of waffles is 57.0 and the quantity supplied of pancakes is 101.0. For simplicity of analysis, the demand for both goods is the same. Using the midpoint formula, calculate the elasticity of supply for pancakes. Please round to two decimal places. Supply in the market for waffles isarrow_forward

- The following graph presents the market for motorcycles in 2015. Between 2015 and 2016, the equilibrium quantity of motorcycles remained constant, but the equilibrium price of motorcycles decreased. Given this information, you can conclude that between 2015 and 2016, the supply of motorcycles and the demand for motorcycles Make changes to the graph to illustrate your answer by showing the positions of the supply and demand curves in 2016. Note: Select and drag one or both of the curves to the desired position. Curves will snap into position, so if you try to move a curve and it snaps back to its original position, just drag it a little farther." lars per motorcycle) Supply Demand Supply ?arrow_forwardhello please help mearrow_forwardAssume that pickled eggs are an inferior good and its market is currently in equilibrium. What will happen to the equilibrium price and quantity of pickled eggs if consumer incomes increase? Group of answer choicesarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education