ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

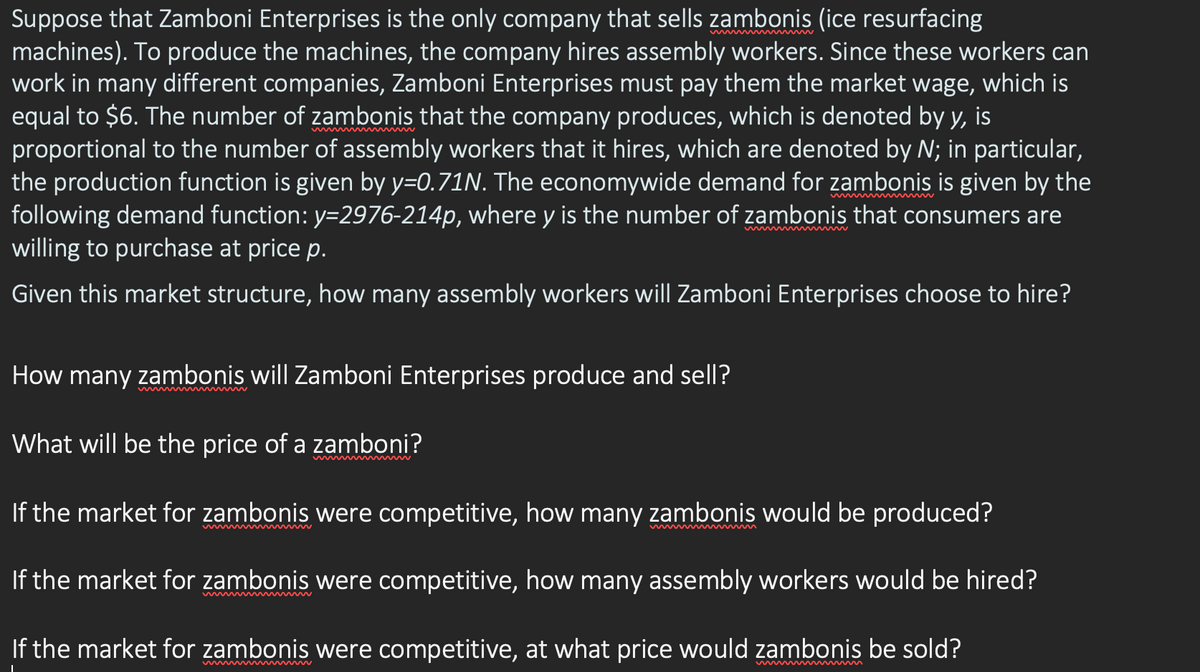

Transcribed Image Text:Suppose that Zamboni Enterprises is the only company that sells zambonis (ice resurfacing

machines). To produce the machines, the company hires assembly workers. Since these workers can

work in many different companies, Zamboni Enterprises must pay them the market wage, which is

equal to $6. The number of zambonis that the company produces, which is denoted by y, is

proportional to the number of assembly workers that it hires, which are denoted by N; in particular,

the production function is given by y=0.71N. The economywide demand for zambonis is given by the

following demand function: y=2976-214p, where y is the number of zambonis that consumers are

willing to purchase at price p.

Given this market structure, how many assembly workers will Zamboni Enterprises choose to hire?

How many zambonis will Zamboni Enterprises produce and sell?

What will be the price of a zamboni?

If the market for zambonis were competitive, how many zambonis would be produced?

If the market for zambonis were competitive, how many assembly workers would be hired?

If the market for zambonis were competitive, at what price would zambonis be sold?

I

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Consider a price-taking firm whose production function is given by q = 3 (L-9) ¹/5 (K-5)¹/⁹ where L and K denote respectively the amount of labour and capital the firm uses to produce q units of output. Suppose the price of labour is w = 16, the price of capital is 24 and the price of the firm's output is p=225. Enter below the value of the firm's fixed cost.arrow_forwardA firm produces output via the function: Q = L - (L²/800), where Q is the output per week and L is the number of labor hours per week. The firm's additional cost of hiring an extra hour of labor is about $25 per hour (wage plus fringe benefits). The firm faces the fixed selling price, P = $40. How much labor should the firm employ?arrow_forwardConsider the following production function: 9=100L0.8K0.4 Currently the wage rate (w) is $4.00 and the price of capital (r) is $2.00. If the firm is using 200 units of capital in production, how much labor should be employed to minimize costs? Labor input = units. (Enter a numeric response using a real number rounded to two decimal places.)arrow_forward

- Suppose a firm has the following expenditures per day: $250 for wages and salaries, $50 for materials, $60 for equipment, and $40 for rent. The market wage for the manager is $120 per day but the owner-manager does not draw a salary. Assume the daily revenue is $420. What are the daily economic costs for the firm described above? Just give equation formula.arrow_forwardConsider a firm with Total Output function (Production Function) given by Q = 6L2 – 0.4L3, where L is variable labor input. The firm is faced with the decision to hire the optimal number of workers in order to maximize its output level. (a) Obtain the Marginal Product function. (b) Find the Average Product function. (c) Determine the level of employment that would maximize the firm’s output level. (d) Verify that the second-order condition is met for the firm's output maximum.arrow_forwardAssume a firm is trying to produce q0 units of output at the lowest total cost. The wage decreases, rotating the isocost line as shown in the below graph. Make the necessary changes to the graph to show the input combination that will now produce q0 at the lowest total cost. Make sure you show the new levels of labor and capital.arrow_forward

- A firm produces output via the function: Q = L - (L2/800), where Q is the output per week and L is the number of labor hours per week. The firm’s additional cost of hiring an extra hour of labor is about $30 per hour (wage plus fringe benefits). The firm faces the fixed selling price, P = $50. How much labor should the firm employ?arrow_forwardSuppose a firm’s production function is q= 2L+ 5K, the wage is w= 4, and the rental rate of capital is r= 8. What is the firm’s cost function C(q)?arrow_forwardConsider the following production function: q= 100L0.8K0.4 Currently the wage rate (w) is $15.00 and the price of capital (r) is $5.00. If the firm is using 200 units of capital in production, how much labor should be employed to minimize costs? Labor input= units. (Entera numeric response using a real number rounded to two decimal places.)arrow_forward

- If the marginal product of labor increases because of a technological advancement, it will likely cause a fall in the number of workers employed. an increase in the price of output produced by labor. a fall in the wage paid to labor. an increase in demand for labor. an increase in the supply of labor.arrow_forwardSuppose, the demand and supply curve in a US manufacturing firm are provided as follows: ES = 20 + 2w ED = 70 − 3w where E is the level of employment and w is the hourly wage. Let’s assume this firm shows the representative wage of the manufacturing industry. Suppose the price of each unit of capital used in this industry is $25. The price of output is constant at $50 per unit. The production function is f(E,K) = E½K ½ , so that the marginal product of labor is MPE = (½)(K/E) ½ If the current capital stock is fixed at 1,600 units, how much labor should the industry employ in the short run? How much profit will the industry earn?arrow_forwardThe cost of producing � units of stuffed alligator toys is �(�)=0.004�2+10�+4000. Find the marginal cost at the production level of 1000 units.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education