ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

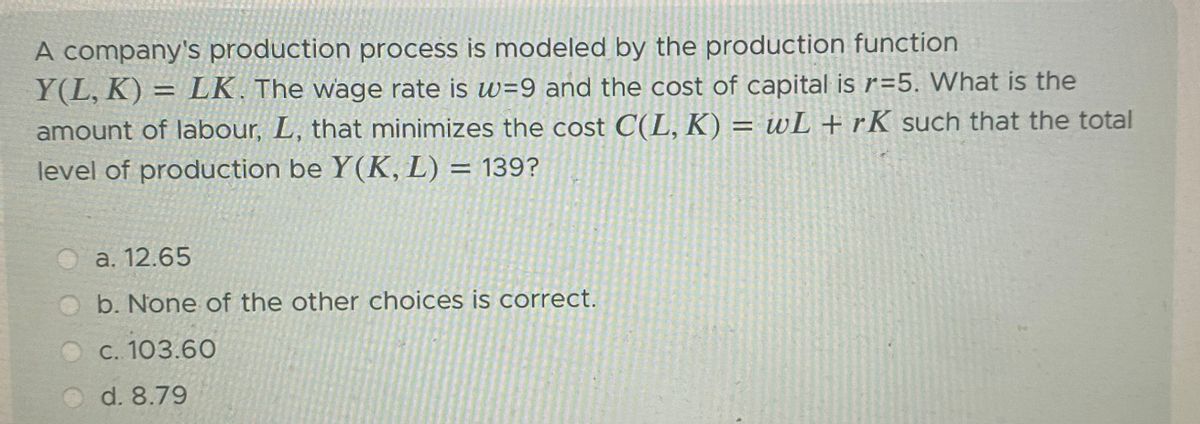

Transcribed Image Text:A company's production process is modeled by the production function

Y(L, K)= LK. The wage rate is w=9 and the cost of capital is r=5. What is the

amount of labour, L, that minimizes the cost C(L, K) = wL + rK such that the total

level of production be Y(K, L) = 139?

a. 12.65

b. None of the other choices is correct.

c. 103.60

d. 8.79

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Cost minimization when output is known and total costs are unknown. A factory that you are managing has an hourly production process that can be represented by the following Cobb Douglas Production function: Q = 2K0.50L 0.5 The price of one unit of capital per hour is $20 and the price of one unit of labour per hour is $20. You have been instructed to produce 200 units per hour or Q = 200. Find the optimal amount of labour and capital that you will be using, and compute the total cost.arrow_forwardGiven Q=100k0.5L0.5 , C=1200 w=30 r=40 (a)Determine the quantity of labour and capital the firm should use in order to minimize the cost. (b)What is the level of output at this level.arrow_forward1/3 1/3 Bridget's Widgets produces widgets with the production function, y = x1 x2, where 1 is the quantity of labor input, x2 is the quantity of capital input, and y is the quantity of output. The per-unit price of labor input is w₁ = 20 and the per-unit price of capital input is w₂ = 80. What is Bridget's long run total cost function, C(y), given that both inputs can be varied in the long run? C(y) 20/2 C(y)-80y/ C(y)-80y = ⚫ C(y)=20y³arrow_forward

- Suppose the short-run production function is q = 5L0.5. If the marginal cost of producing the 5th unit is $13, what is the wage per unit of labor? Your Answer:arrow_forwardA firm faces a production function with inputs capital (K) and labor (L): F(K, L) = K¹/² L¹/4 The amount of capital used for production is determined at the beginning of the year. The prices of K and L are v and w respectively.arrow_forwardA firm uses labor (L) and capital (K) to produce output (q) according to the function: q= L ².K In the short-run, the firm's level of capital is fixed at one unit (K 1). Assume the firm has already paid a fixed cost of $1 (F = 1) for their one unit of capital. In addition, assume that each unit of labor must be paid a wage of $1 (w = 1). If the firm can sell each unit of output at a price of $6 ( p = 6), answer the following two questions: A) What is the firm's profit maximizing level of output in the short-run? Profit maximizing q 3 = B) What is the maximum profit the firm can earn in the short-run? Maximum profit 8 = dollarsarrow_forward

- Suppose w= 1 and r= 3. Solve the cost minimization problem to find L*(q) and K*(q). Then find the cost function C(q).arrow_forwardGiven the total cost equation: level of Q yields the minimum cost of production? TC = 32 + 2Q², what level of total averagearrow_forwardSuppose the production function is given by f(K,L) = 3Kl, where K denotes capital and L denotes labor. The price of capital is 2 TL/machine-hr, the price of labor is 24 TL/person-hr, and capital is fixed at 4 machine-hr in the short run. a) Find the short-run TC, TVC, and TFC curves for this production process. Sketch them on a single graph. Do not forget to label all axes and necessary points on your graph. b) Find short-run ATC, AVC, AFC, and MC curves for this production process. Sketch them on a single figure. Do not forget to label all axes and necessary points on your graph.arrow_forward

- Hannah and Sam run Moretown Makeovers, a home remodeling business. The number of square feet they can remodel in a week is described by the Cobb-Douglas production function Q=F(L,K) Q=10L^0.5K^0.5,where L is their number of workers and K is units of capital. The wage rate is $250 per week and a unit of capital costs $250 per week. Suppose that when initially producing 100 square feet a week, they use 10 units of capital.a. What is their short-run cost of remodeling 1,000 square feet per week? Instructions: Enter your answer as a whole number. $ b. What is their long-run cost of remodeling 1,000 square feet per week? Instructions: Enter your answer as a whole number. $arrow_forwardA factory that you are managing has an hourly production process that can be represented by the following Cobb Douglas Production function: Q=10KL. The price of one unit of capital per hour is $20 and the price of one unit of labour per hour is $20. You have been instructed to produce 100 units per hour or Q-100. Find the optimal amount of labour and capital that you will be using, and compute the total cost.arrow_forwardA firm’s only variable factor is labour and it produces a single product, X. It also has fixed costs. The short-run production function is; X=-0.1L3 + 6L2 + 12L. Where X is the output in tons, and L is the number of persons employed. How many persons are employed if the average physical product of labour is maximized? How many persons are employed if the marginal physical product of labour is maximized? What is the quantity of X when average variable cost is minimized? If the weekly wage is $360 and the price of X is $30 per ton, how much X should be produced to maximize profits?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education