Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

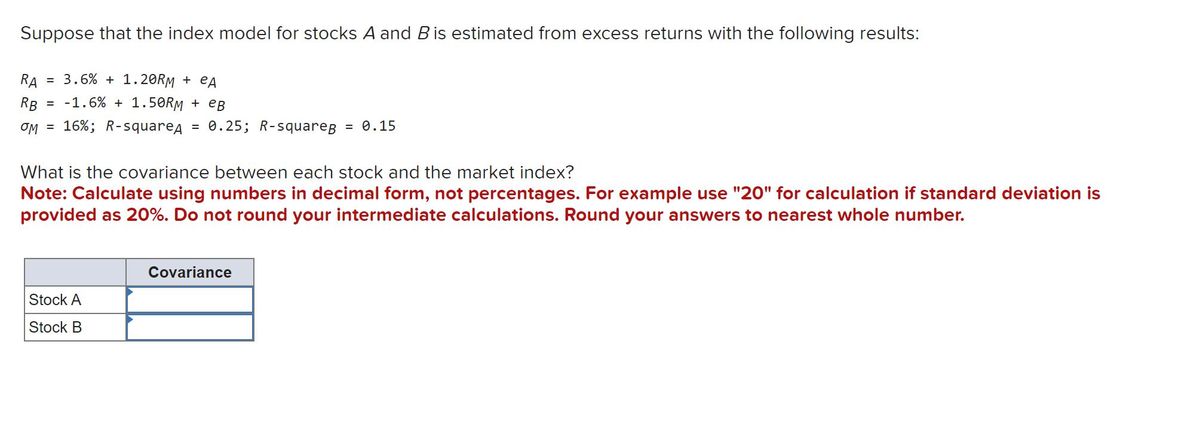

Transcribed Image Text:Suppose that the index model for stocks A and B is estimated from excess returns with the following results:

RA = 3.6% + 1.20RM + eA

RB = -1.6% + 1.50RM + eB

OM = 16%; R-squareд = 0.25; R-squarep = 0.15

What is the covariance between each stock and the market index?

Note: Calculate using numbers in decimal form, not percentages. For example use "20" for calculation if standard deviation is

provided as 20%. Do not round your intermediate calculations. Round your answers to nearest whole number.

Stock A

Stock B

Covariance

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Suppose your expectations regarding the stock price are as follows: State of the Market Boom Normal growth Recession Probability Ending Price 0.26 $ 140 0.25 110 0.49 80 Use the equations E (r) = Ep (s) r(s) and o² = Ep (s) [r(s) — E(r)]² to compute the mean and standard deviation of the HPR on - S S Mean Standard deviation HPR (including dividends) 55.0% 21.0 -16.0 stocks. Note: Do not round intermediate calculations. Round your answers to 2 decimal places. % %arrow_forwardBaghibenarrow_forwardWe know the following expected returns for stocks A and B, given the different states of the economy: State(s) Probability E(rA,s) E(rB,s) Recession 0.1-0.06 0.04 Normal 0.5 0.09 0.07 Expansion 0.4 0.17 0.11 What is the standard deviation of returns for stock B?arrow_forward

- 10:06 9. Given: EXR) .10 E(R) .15 0₁.03 0₂.05 Calculate the expected returns and expected standard deviations of a two-stock portfolio in which Stock I has a weight of 60 percent under the following conditions: a. 1.00 b.2-0.75 c. P₁2=0.25 d.n=0.00 c. P₁2=-0.25 f.r=-0.75 872-1.00 a. w-1.00 b. w₁=0.75 c. w=0.50 d. w₁ -0.25 c. w;0.05 Expert Q&A Calculate the expected returns and expected standard deviations of a two-stock portfolio having a correlation coefficient of 0.70 under the following conditions: 10. Given: E(R₁) 0.12 E(R₂) = 0.16 .ll? G₁-0.04 0₂-0.06 Plot the results on a return-risk graph. Without calculations, draw what a curve with varying weights would look like if the correlation coefficient had been 0.00, or if it had been -0.70. Donearrow_forwardData: S0 = 102; X = 115; 1 + r = 1.1. The two possibilities for ST are 146 and 84. Required: The range of S is 62 while that of P is 31 across the two states. What is the hedge ratio of the put? Form a portfolio of one share of stock and two puts. What is the (nonrandom) payoff to this portfolio? What is the present value of the portfolio? Given that the stock currently is selling at 102, calculate the put value.arrow_forwardE(FAssume that using the Security Market Line (SML) the required rate of return (RA) on stock A is found to be half of the required return (Rs) on stock B. The risk-free rate (R;) is one-fourth of the required return on A. Return on market portfolio is denoted by RM. Find the ratio of beta of A (BA) to beta of B (BB). a oarrow_forward

- What is the standard deviation of Stock B returns given the information below about its returns across future states of nature? Enter return in decimal form, rounded to 4th digit, as in "0.1234"arrow_forwardK -61 =1 2 N (Expected rate of return and risk) Syntex, Inc. is considering an investment in one of two common stocks. Given the information that follows, which investment is better, based on the risk (as measured by the standard deviation) and return? Probability 0.25 0.50 0.25 Common Stock A Probability 0.25 0.25 0.25 0.25 (Click on the icon in order to copy its contents into a spreadsheet.) @ 2 a. Given the information in the table, the expected rate of return for stock A is 16.25 %. (Round to two decimal places.) The standard deviation of stock A is %. (Round to two decimal places.) b. The expected rate of return for stock B is%. (Round to two decimal places.) The standard deviation for stock B is%. (Round to two decimal places.) c. Based on the risk (as measured by the standard deviation) and return of each stock, which investment is better? (Select the best choice below.) 30² F2 W OA. Stock A is better because it has a higher expected rate of return with less risk B. Stock B is…arrow_forwardRefer to the graph below, what is the beta of portfolio X under CAPM? E(r) A 0.14 0.10 0.06 N Beta of portfolio X = place) M X o(r) (to the nearest 1 decimalarrow_forward

- v.2arrow_forwardSuppose securities A, B, and C have the following expected return and risk. Stock Expected return Risk A 8% 6% B 7% 9% C 13% 9% What is the coefficient of variation for stock A?arrow_forwardUse the following information: Stock A B Good state 10% 14% Bad state 2% -2% Assume there is 60% probability that the good state occurs and 40% chance the bad state occurs. What is the standard deviation of stock A? (Please use 5 decimal places, this should be written in percentage, so an answer of 23.143% should be written as .23143)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education