Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

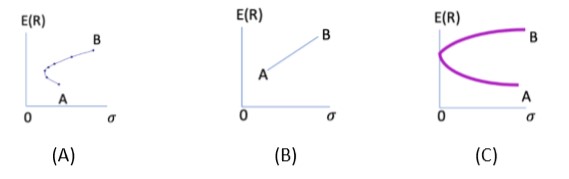

Q1) The covariance between stocks A and B is 0.0014, standard deviation of stock A is 0.032, and standard deviation of stock B is 0.044. Which of the following is the most appropriate to depict the risk-return characteristics of a portfolio consisting of only stocks A and B, and explain why?

(Image attached as Q)

Transcribed Image Text:E(R)

E(R)

E(R)

A

A

B.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- If the standard deviation of stock 'A' is .25, the standard deviation of stock 'B' is .30, and the correlation between stocks 'A' and 'B' is 0.7, the covariance between stocks 'A' and 'B' is___.arrow_forwardYou are given the following information concerning three portfolios, the market portfolio, and the risk-free asset: Portfolio X Y Z Market Risk-free Rp 14.0% 13.0 .8.5 12.0 7.2 Ор 39.00% 34.00 24.00 29.00 0 Bp 1.50 1.15 0.90 1.00 0 Assume that the correlation of returns on Portfolio Y to returns on the market is 0.90. What percentage of Portfolio Y's return is driven by the market? Note: Enter your answer as a decimal not a percentage. Round your answer to 4 decimal places. R-squaredarrow_forwardThe expected return of a portfolio is simply the weighted average of the expected returns for the individual assets within the portfolio. Group of answer choices True Falsearrow_forward

- You are given the following information concerning three portfolios, the market portfolio, and the risk- free asset: Portfolio X Y Z Market Risk-free Rp 14.5% R-squared 13.5 9.1 10.7 5.4 op 36% 31 21 26 0 6p 1.60 1.30 .80 1.00 0 Assume that the correlation of returns on Portfolio Y to returns on the market is 72. What percentage of Portfolio Y's return is driven by the market? (Enter your answer as a decimal not a percentage. Round your answer to 4 decimal places.)arrow_forwardWhich of the following stocks have the highest systematic risk? A. A stock with a high correlation to the market and a low return volatility. B. A stock with a low correlation to the market and a high return volatility. C. A stock with a high correlation to the market and high return volatility. D. A stock with a low correlation to the market and a low return volatility.arrow_forwardThe beta of a portfolio is: A. A measure of the correlation of betas of the securities in the portfolio. B. Always greater than one. C. The market value weighted average beta of the securities in the portfolio. D. The geometric average of the beta of the securities in the portfolio.arrow_forward

- The following figures show the optimal portfolio choice for two investors with different levels of risk-aversion graphically. Which statement is correct? E[R] 0.3 0.25 0.2 0.15 0.1 0.05 0 0 0.05 0.1 0.15 Figure 1 0.2 0.25 0.3 0.35 o(R) 0.4 0.45 [H]Z 0.3 0.25 0.2 0.15 0.1 0.05 0 0 0.05 0.1 Figure (2) shows an investor that borrows in risk-free rate and invests in the risky asset. Figure (1) shows an investor with a conservative investment behavior. In the optimal point of both figures, the highest indifference curve is tangent to the efficient frontier. In Figure (1), more aggressive investment decision led to a higher Sharpe ratio. 0.15 Figure 2 0.2 0.25 o (R) 0.3 0.35 0.4 0.45arrow_forwardchoose which one ? 3.Assume CAPM holds. What is the correlation between an efficient portfolio and the market portfolio?a.1b.-1c.0d.Not enough informationarrow_forwardE(FAssume that using the Security Market Line (SML) the required rate of return (RA) on stock A is found to be half of the required return (Rs) on stock B. The risk-free rate (R;) is one-fourth of the required return on A. Return on market portfolio is denoted by RM. Find the ratio of beta of A (BA) to beta of B (BB). a oarrow_forward

- T/F. The “Fear Index” is calculated using estimates of implied volatility. Group of answer choices True Falsearrow_forwardThe index model for stock A has been estimated with the following result: RA = 0.01 + 0.9RM + eA. If σM = 0.25 and R2A = 0.25, the standard deviation of return of stock A is:arrow_forwardA stock has a correlation with the market of 0.4. If the Sharpe ratio of the market portfolio is 0.7, what is the Sharpe ratio of the stock? (Hint: algebraically manipulate the SML equation.) 0.28 0.75C. 0.60D. 0.55arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education