ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

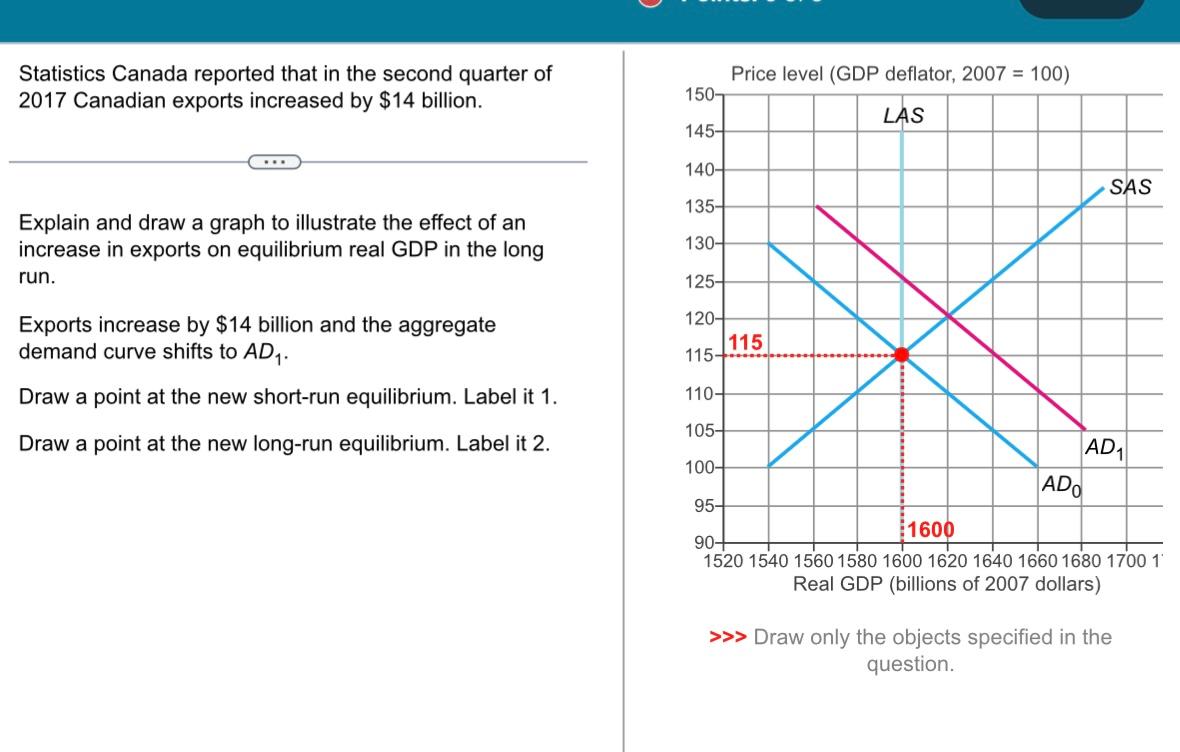

Transcribed Image Text:Statistics Canada reported that in the second quarter of

2017 Canadian exports increased by $14 billion.

Explain and draw a graph to illustrate the effect of an

increase in exports on equilibrium real GDP in the long

run.

Exports increase by $14 billion and the aggregate

demand curve shifts to AD ₁.

Draw a point at the new short-run equilibrium. Label it 1.

Draw a point at the new long-run equilibrium. Label it 2.

150-

145-

140-

135-

130-

125-

120-

115-

Price level (GDP deflator, 2007 = 100)

LAS

115

SAS

110-

105-

100-

95-

1600

90+

1520 1540 1560 1580 1600 1620 1640 1660 1680 1700 11

Real GDP (billions of 2007 dollars)

ADO

AD₁

>>> Draw only the objects specified in the

question.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Which items describe long-run aggregate supply (LRAS), and which ones describe short-run aggregate supply (SRAS)? Long-Run Aggregate Supply The unemployment rate, u, may be above or below the natural rate. Unemployment is at the natural rate, u*. All prices can change. Short-Run Aggregate Supply + Only some prices can change. The economy's output may be above or below the full-employment level, Y*. The economy's output, Y, is at the full- employment level.arrow_forwardFollowing an increase in consumer confidence, the US economy is experiencing a significant increase in aggregate spending. Using a correctly labeled aggregate demand and aggregate supply diagram, show how the change in aggregate spending will affect each of the following in the short run -Output -The price levelarrow_forwardAggregate Demand and Aggregate Supply (AD-AS) Model (Chapter 13) 5.1 Why does the short-run aggregate supply curve slope upward? 5.2 Explain why the long-run aggregate supply curve is vertical. Then, explain how each of the following events would affect the long-run aggregate supply curve. A lower price levels b. A decrease in the labor force A decrease in the quantity of capital goods d. Technological change a. с. 5.3. Starting from long-run equilibrium, use the basic aggregate demand and aggregate supply diagram to show what happens in both the long run and the short run when there is a decline in wealth. Explain how the economy moves back to full employment.arrow_forward

- The following events have occurred at times in the history of the United States: 1. The world economy goes into an expansion. 2. U.S. businesses expect future profits to rise. 3. The government increases its expenditure on goods and services in a time of war or increased international tension. Explain the combined effects of these events on U.S. real GDP and the price level, starting from a position of long-run equilibrium. The graph shows an economy in long-run equilibrium. The world economy goes into an expansion, U.S. businesses expect future profits to rise, and the government increases its expenditure on goods and services in a time of war or increased international tension. Draw one new curve that shows the combined effect of the three events. Label it. Draw a point at the new short-run macroeconomic equilibrium. 140- 130- Price level (GDP deflator, 2012=100) 120- 110- 100- 90- 80- 18.0 LAS SAS AD G 19.0 20.0 21.0 Real GDP (trillions of 2012 dollars) Denonh: the ohiarte conciliad…arrow_forwardhow should I answer this?arrow_forwardThe following graph represents the short-run aggregate supply curve (SRAS) based on an expected price level of 120. The economy's full- employment output level is $9 trillion. Major unions across the country have recently negotiated three-year wage contracts with employers. The wage contracts are based on an expected price level of 120, but the actual price level turns out to be 160. Show the short-run effect of the unexpectedly high price level by dragging the curve or moving the point to the appropriate position. PRICE LEVEL (CPI) 240 200 160 40 0 0 3 SRAS[120] 6 9 12 REAL GDP (Trillions of dollars) 15 18 SRAS[120] 0 (?) Interpret the change you drew on the previous graph by filling in the blanks in the following paragraph:arrow_forward

- 7. The long-run aggregate supply curve and short-run adjustments Suppose an economy's short-run aggregate supply curve (SRAS), current equilibrium aggregate price level (P₁), and real GDP (Q1) are shown on the graph that follows. The economy currently has Natural Real GDP (QN) of $6 trillion. Use this information to place the orange long-run aggregate supply curve (LRAS, square symbols) in the correct position on the graph. 20 PRICE LEVEL 0 2 4 6 Q₁ REAL GDP (Trillions of dollars) 8 SRAS 10 LRASarrow_forwardBy using aggregate supply and demand curves to illustrate your points, discuss the impacts of the following events on the price level and on equilibrium GDP (Y) in the short run: a. A tax cut holding government purchases constant with the economy operating at near full capacity b. An increase in the money supply during a period of high unemployment and excess industrial capacity c. An increase in the price of oil caused by a war in the Middle East, assuming that the Central Bank attempts to keep interest rates constant by accommodating inflation d. An increase in taxes and a cut in government spending supported by a cooperative Fed acting to keep output from fallingarrow_forwardDiscuss how the economy returns to equilibrium in response to changes in aggregate demand (AD) and aggregate supply (AS) in both the short run and long runarrow_forward

- The following graph shows an economy's short-run aggregate supply curve (SRAS), current equilibrium aggregate price level (P₁), and real GDP ( 21). The economy currently has Natural Real GDP (QN) of $6 trillion. Use this information to place the orange long-run aggregate supply curve (LRAS, square symbols) in the correct position on the graph. PRICE LEVEL 10 8 1 A 2 0 0 2 A₁ 4 6 Q₁ REAL GDP (Trillions of dollars) 8 SRAS 10 The equilibrium A₁, shown on the graph, reveals that real GDP (2₁) is shifting SRAS O LRAS Natural Real GDP. As a result, wages will over time,arrow_forwardThe following graph shows the aggregate demand curve (AD), the short-run aggregate supply curve (AS), and the long-run aggregate supply curve ( LRAS) for a hypothetical economy. Initially, the expected price level equals the actual price level, and the economy experiences long-run equilibrium at a natural level of output of $100 billion.. Suppose a bout of severe weather drives up agricultural costs, increases the costs of transporting goods and services, and increases the costs of producing goods and services. Use the graph to help you answer the questions about the short-run and long-run effects of the increase in production costs that follow. (Note: You will not be graded on any adjustments made to the graph.) Hint: For simplicity, ignore any possible impact of the severe weather on the natural level of output.arrow_forwardSuppose that because of globally adverse meteorological conditions, there are serious concerns of climbing prices in an extensive group of commodities. As a result, people now expect an acute increase in the level of input prices. The figure shows aggregate demand (AD), short‑run aggregate supply (SRAS), and long‑run aggregate supply (LRAS). Move one or more of these curves to describe the short‑run effect this would have in the economy and answer the two questions. Adjust graph in picture. In the short run, price level a. increases. b. decreases. c. The change is indeterminate. In the short run, real GDP (or aggregate output) a. The change is indeterminate. b. decreases. c. increases.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education