FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

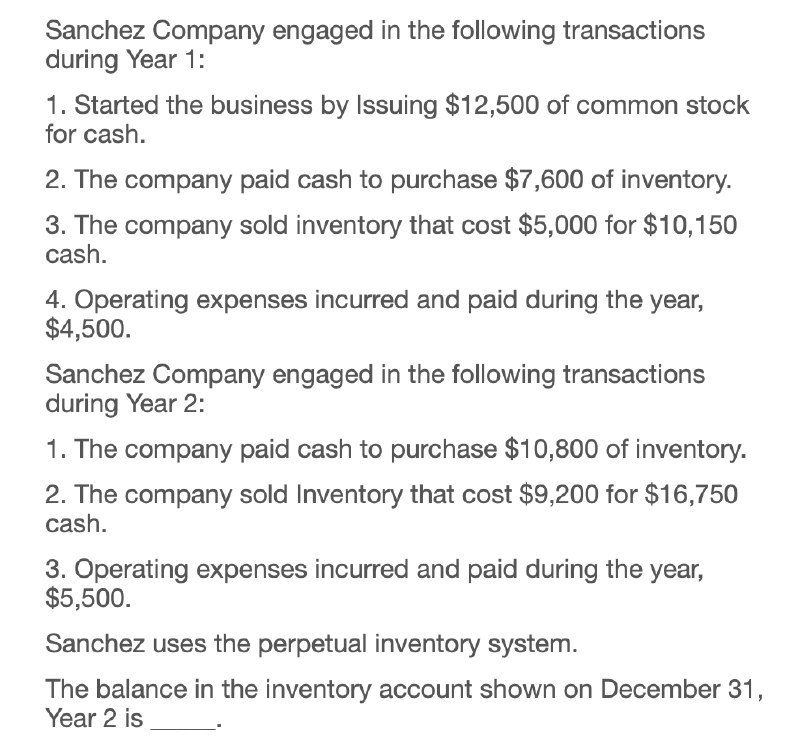

Transcribed Image Text:Sanchez Company engaged in the following transactions

during Year 1:

1. Started the business by Issuing $12,500 of common stock

for cash.

2. The company paid cash to purchase $7,600 of inventory.

3. The company sold inventory that cost $5,000 for $10,150

cash.

4. Operating expenses incurred and paid during the year,

$4,500.

Sanchez Company engaged in the following transactions

during Year 2:

1. The company paid cash to purchase $10,800 of inventory.

2. The company sold Inventory that cost $9,200 for $16,750

cash.

3. Operating expenses incurred and paid during the year,

$5,500.

Sanchez uses the perpetual inventory system.

The balance in the inventory account shown on December 31,

Year 2 is

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps

Knowledge Booster

Similar questions

- Sanchez Company engaged in the following transactions during Year 1: 1) Started the business by issuing $13,100 of common stock for cash. 2) The company paid cash to purchase $7,900 of inventory. 3) The company sold inventory that cost $5,300 for $10,900 cash. 4) Operating expenses incurred and paid during the year, $4,800. Sanchez Company engaged in the following transactions during Year 2: 1) The company paid cash to purchase $11,400 of inventory. 2) The company sold inventory that cost $9,500 for $17,500 cash. 3) Operating expenses incurred and paid during the year, $5,800. Note: Sanchez uses the perpetual inventory system. What is Sanchez's gross margin for Year 2? Multiple Choice $9,500 $2,200 $6,100 $8,000arrow_forwardYork Company engaged in the following transactions for Year 1. The beginning cash balance was $86,000 and the ending cash balance was $59,100. 1. Sales on account were $548,000. The beginning receivables balance was $128,000 and the ending balance was $90,000. 2. Salaries expense for the period was $232,000. The beginning salaries payable balance was $16,000 and the ending balance was $8,000. 3. Other operating expenses for the period were $236,000. The beginning other operating expenses payable balance was $16,000 and the ending balance was $10,000. 4. Recorded $30,000 of depreciation expense. The beginning and ending balances in the Accumulated Depreciation account were $12,000 and $42,000, respectively. 5. The Equipment account had beginning and ending balances of $44,000 and $56,000, respectively. There were no sales of equipment during the period. 6. The beginning and ending balances in the Notes Payable account were $36,000 and $44,000, respectively. There were no payoffs of…arrow_forwardLine following information applies to the questions displayed below.j The following transactions apply to Park Company for Year 1: 1. Received $31,000 cash from the issue of common stock. 2. Purchased inventory on account for $143,000. 3. Sold inventory for $172,500 cash that had cost $105,500. Sales tax was collected at the rate of 8 percent on the inventory sold. 4. Borrowed $24,000 from First State Bank on March 1, Year 1. The note had a 8 percent interest rate and a one-year term to maturity. 5. Paid the accounts payable (see transaction 2). 6. Paid the sales tax due on $153,500 of sales. Sales tax on the other $19,000 is not due until after the end of the year. 7. Salaries for the year for one employee amounted to $28,000. Assume the Social Security tax rate is 6 percent and the Medicare tax rate is 1.5 percent. Federal income tax withheld was $5,300. 8. Paid $2,600 for warranty repairs during the year. 9. Paid $12,000 of other operating expenses during the year. 10. Paid a…arrow_forward

- Gibson Company engaged in the following transactions for Year 1. The beginning cash balance was $28,100 and the ending cash balance was $74,991. 1. Sales on account were $283,100. The beginning receivables balance was $94,700 and the ending balance was $77,000. 2. Salaries expense for the period was $55,460. The beginning salaries payable balance was $3,815 and the ending balance was $2,180. 3. Other operating expenses for the period were $120,170. The beginning other operating expenses payable balance was $4,860 and the ending balance was $9,181. 4. Recorded $19,330 of depreciation expense. The beginning and ending balances in the Accumulated Depreciation account were $14,340 and $33,670, respectively. 5. The Equipment account had beginning and ending balances of $211,970 and $238,570, respectively. There were no sales of equipment during the period. 6. The beginning and ending balances in the Notes Payable account were $48,500 and $150,500, respectively. There were no payoffs of…arrow_forwardnces Blooming Flower Company was started in Year 1 when it acquired $60,500 cash from the issue of common stock. The following data summarize the company's first three years' operating activities. Assume that all transactions were cash transactions. Purchases of inventory Sales Cost of goods sold Selling and administrative expenses Income Statements Required: Prepare an income statement (use multistep format) and balance sheet for each fiscal year. (Hint: Record the transaction data for each accounting period in the accounting equation before preparing the statements for that year.) Complete this question by entering your answers in the tabs below. Balance Sheets Assets Cash Merchandise inventory Prepare a balance sheet for each fiscal year. (Hint: Record the transaction data for each accounting period in the accounting equation before preparing the statements for that year.) Total assets Liabilities Stockholders' equity Common stock Retained earnings Year 1 $ 22,200 26,400 12,500…arrow_forwardVigeland Company completed the following transactions during Year 1. Vigeland’s fiscal year ends on December 31. January 15 Purchased and paid for merchandise. The invoice amount was $15,200; assume a perpetual inventory system. April 1 Borrowed $774,000 from Summit Bank for general use; signed a 10-month, 9% annual interest-bearing note for the money. June 14 Received a $24,000 customer deposit for services to be performed in the future. July 15 Performed $3,450 of the services paid for on June 14. December 12 Received electric bill for $26,160. Vigeland plans to pay the bill in early January. December 31 Determined wages of $15,000 were earned but not yet paid on December 31 (disregard payroll taxes). Required: Prepare journal entries for each of these transactions. Prepare the adjusting entries required on December 31.arrow_forward

- Blooming Flower Company was started in Year 1 when it acquired $61,700 cash from the issue of common stock. The following data summarize the company's first three years' operating activities. Assume that all transactions were cash transactions. Purchases of inventory Sales Cost of goods sold Selling and administrative expenses Income Statements Required: Prepare an income statement (use multistep format) and balance sheet for each fiscal year. (Hint: Record the transaction data for each accounting period in the accounting equation before preparing the statements for that year.) Complete this question by entering your answers in the tabs below. Balance Sheets Assets Cash Merchandise inventory Prepare a balance sheet for each fiscal year. (Hint: Record the transaction data for each accounting period in the accounting equation before preparing the statements for that year.) Total assets Liabilities Stockholders' equity Common stock Retained earnings Year 1 $ 22,600 27,000 13,200 5,490…arrow_forwardNorthwest Sales had the following transactions in Year 1: The business was started when it acquired $58,500 cash from the issue of common stock. Northwest purchased $185,000 of merchandise for cash in Year 1. During the year, the company sold merchandise for $198,220. The merchandise cost $109,021. Sales were made under the following terms: a. Cash sales $48,870b. Credit card sales (The credit card company charges a $2.25 percent service fee.) $139,520c. Sales on account $9,830 The company collected all the amount receivable from the credit card company. The company collected $9,044 of accounts receivable. The company paid $40,927 cash for selling and administrative expenses. Determined that 3.75 percent of the ending accounts receivable balance would be uncollectible. Required Show the effects of each of the transactions on the elements of the financial statements, using a horizontal statements model. Use + for increase, − for decrease, and leave blank for not affected. In the…arrow_forwardcreate a income statement for: The following transactions apply to Ozark Sales for Year 1: The business was started when the company received $50,000 from the issue of common stock. Purchased equipment inventory of $380,000 on account. Sold equipment for $510,000 cash (not including sales tax). Sales tax of 8 percent is collected when the merchandise is sold. The merchandise had a cost of $330,000. Provided a six-month warranty on the equipment sold. Based on industry estimates, the warranty claims would amount to 2 percent of sales. Paid the sales tax to the state agency on $400,000 of the sales. On September 1, Year 1, borrowed $50,000 from the local bank. The note had a 4 percent interest rate and matured on March 1, Year 2. Paid $6,200 for warranty repairs during the year. Paid operating expenses of $78,000 for the year. Paid $250,000 of accounts payable. Recorded accrued interest on the note issued in transaction no. 6.arrow_forward

- During Year 1, Hardy Merchandising Company purchased $21,000 of inventory on account. Hardy sold inventory on account that cost $15,800 for $23,600. Cash payments on accounts payable were $13,100. There was $21,000 cash collected from accounts receivable. Hardy also paid $4,100 cash for operating expenses. Assume that Hardy started the accounting period with $18,500 in both cash and common stock. Required a. Record the events in a horizontal statement model. In the Cash Flow column, use OA to designate operating activity, IA for investment activity, FA for financing activity, or NC for net change in cash. If the element is not affected by the event, leave the cell blank. b. What is the balance of accounts receivable at the end of Year 1? c. What is the balance of accounts payable at the end of Year 1? d. What are the amounts of gross margin and net income for Year 1? e. Determine the amount of net cash flow from operating activities. Complete this question by entering your answers in…arrow_forwardThe general ledger of Hubert Corporation provides the following information: End of Year Beginning of Year Accounts Receivable $ 125,000 $ 94, 000 Inventory 280,000 210,000 Accounts Payable 130,000 65,000 The company's net sales for the year were $2,850,000 and cost of goods sold amounted to $1,650,000. Instructions Calculate the following: a) Cash receipts from customers. b) Cash payments to suppliers.arrow_forwardGeneral Accountingarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education