ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

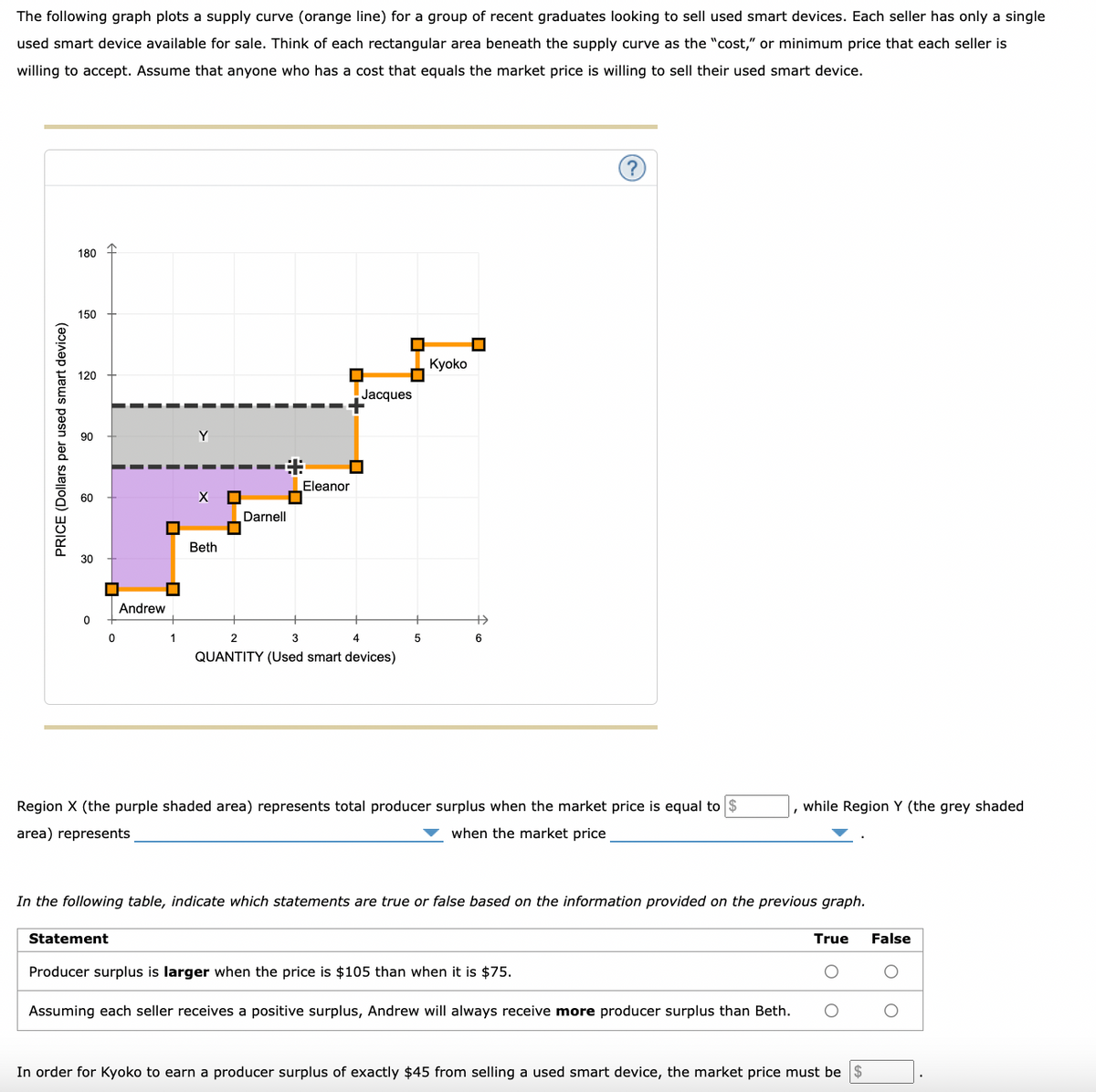

Transcribed Image Text:The following graph plots a supply curve (orange line) for a group of recent graduates looking to sell used smart devices. Each seller has only a single

used smart device available for sale. Think of each rectangular area beneath the supply curve as the "cost," or minimum price that each seller is

willing to accept. Assume that anyone who has a cost that equals the market price is willing to sell their used smart device.

PRICE (Dollars per used smart device)

180

150

120

90

60

30

0

0

Andrew

U

Statement

1

Y

X

Beth

ロロ

04

Darnell

张 ☐

Eleanor

Jacques

ロロ

2

3

4

QUANTITY (Used smart devices)

5

Kyoko

+

6

Region X (the purple shaded area) represents total producer surplus when the market price is equal to $

area) represents

when the market price

In the following table, indicate which statements are true or false based on the information provided on the previous graph.

while Region Y (the grey shaded

Producer surplus is larger when the price is $105 than when it is $75.

Assuming each seller receives a positive surplus, Andrew will always receive more producer surplus than Beth.

True

In order for Kyoko to earn a producer surplus of exactly $45 from selling a used smart device, the market price must be $

False

O

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Last Saturday, Sammy supplied 100 baskets of strawberries at the farmer’s market when the equilibrium price was $3. This Saturday, he supplied 120 baskets of strawberries when the equilibrium price increased to $4. Sammy’s producer surplus did not change; it was the same this Saturday as it was last Saturday. Select one: True Falsearrow_forwardAs you can see from the article in the prior problem, "Rents Hit All-Time Highs amid Job Growth and Low Vacancy Rates," some people move out as a result of rent increases, while others are ready to pay an even higher rent. Rent control adds yet another aspect by setting a ceiling on what the rental price can ultimately rise to. The supply and demand model can be used to illustrate the mechanism that leads to all these different market outcomes. Consider the market for rental properties in Los Angeles and Orange counties in Southern California. Suppose that while average earnings increased by about 10% in Los Angeles and Orange counties, the average rent has increased by 20%. (Assume for a moment that there are no rent control regulations.) Adjust the following graph to illustrate the rent increase by either using the black point (cross symbol) or by shifting the supply and demand curves. The Market for Rental Properties in Los Angeles and Orange Counties 4000 3600 Supply Demand 3200…arrow_forwardA1-1. Imagine that a market for a good is characterized by the following supply and demand equations: QS = –35 + 35P QD =100 – 10P where QS and QD are quantities in units and P is the price per unit. (a) Graph the supply and demand curves with quantity on the horizontal and price on the vertical axis. Be sure to calculate the P and Q intercepts for demand and the P intercept for supply. Calculate and illustrate the equilibrium price and quantity. [Hint: Show your work.] (b) Calculate both the demand and supply elasticity around the equilibrium point. [Hint: you can use either the point method or the average arc (midpoint) method.] (c) If a regulator imposes a quantity restriction by granting quotas for 60 units of output to existing producers, what is the new price and quantity traded? Does this policy create deadweight loss (DWL) in the market? Briefly explain and identify any DWL in your diagram. (d) What is the value of a unit of quota? Illustrate in your diagram.…arrow_forward

- Find the consumer surplus and producer surplus for the demand and supply functions asfollows respectively. pz (x) = -0.2x +8, pi (x) = 0.1x + 2. Please interpret the meaning of both by a sketch.arrow_forwardAnderson is willing to pay $12. Kendrick can provide the item for $10, but producing the item imposes a cost of $8 on Talib. If Anderson purchases the item from Kendrick for $11, what is the total surplus from the transaction? (Remember, do not enter the $, and enter the - if TS is negative.)arrow_forwardOnly typed solutionarrow_forward

- Corn is a very valuable product for which the U.S. government routinely offers subsidies. With no price support, the equilibrium price for corn is $300 per ton and the equilibrium quantity is 500 million tons per year. Suppose that the government agrees to pay farmers $350 for every ton of corn they produce and can't sell in the market. According to the farmer's market supply curve, 600 million tons per year is supplied at the price of $350 a ton, so production should increase to this amount. However, domestic users of corn cut back their purchases. Only 450 million tons a year is demanded at the price of $350 a ton, and purchases decrease to this amount. Farmers continue to produce 500 million tons of corn per year, so because they produce a greater quantity of corn than domestic buyers are willing to purchase, something must be done with the surplus. To make the price support work, the government decides to buy the surplus. a. In this example, how many million tons does the…arrow_forwardEach rectangle on the graph corresponds to a particular seller in this market: blue (circe symbols) for Andrew, green (triangle symbols) for Beth, purple (diamond symbols) for Darnell, tan (dash symbols) for Eleanor, and orange (square symbols) for Jacques. (Note: The name labels are to the right of the corresponding segment on the supply curve.) Use the rectangles to shade the areas representing producer surplus for each person who is willing to sell a motor scooter at a market price of $70. (Note: If a person will not sell a motor scooter at the market price, indicate this by leaving their rectangle in its original position on the palette.) ? PRICE (Dollars per motor scooter) 160 140 120 100 180 60 40 20 0 0 Andrew 2 K Bet Darnell Jacques Eleanor 5 3 QUANTITY (Motor scooters) Market Price 6 7 8 ITI Andrew Beth Damell Eleanor 8 8 Jacquesarrow_forwardSmall engines are the main components of office and house appliances like printers, hand dryers, microwave ovens, food processors, etc. The graph depicts the market for small engines in the United States. Suppose that the government imposes a $15 tariff on each imported engine in an effort to bring manufacturing jobs back to the United States. Place the Waste shape to describe the waste of resources that would result from the trade restriction. Price (3) Incorrect 50 45 40 35 30 25 20 15 10 5 0 0 total cost: What is the total cost of the tariff? 337.5 Domestic supply Domestic demand 15 30 45 60 75 90 105 120 135 150 Quantity (millions of engines) Incorrect World supply Waste millions of dollarsarrow_forward

- Next, consider an example of DWL in the labour market. Suppose the demand for labour is given by the fixed gross wage W = $16. The supply is given by W = 0.8L. (a) Illustrate the market geometrically. (b) Calculate the equilibrium amount of labour supplied, and the supplier surplus. (c) Suppose a wage tax that reduces the wage to W = $12 is imposed. By how much is the supplier’s surplus reduced at the new equilibrium?arrow_forward6. Producer surplus and price changes The following graph plots a supply curve (orange line) for a group of recent graduates looking to sell used smart devices. Each seller has only a single used smart device available for sale. Think of each rectangular area beneath the supply curve as the "cost," or minimum price that each seller is willing to accept. Assume that anyone who has a cost that equals the market price is willing to sell their used smart device. PRICE (Dollars per used smart device) 360 300 240 180 120 60 0 0 □ 0 Jacques 1 XO Kyoko 49 Musashi ☐ Rina U Sean 2 3 4 QUANTITY (Used smart devices) D 0 ☐ 5 Yvette Đ 6 (?)arrow_forwardIf the inverse market demand function for a good is P(Q) = 100 - 3Q and the inverse market supply function for a good is P(Q)= ) = 2Q, what are the consumer and producer surplus in the market equilibrium? The consumer surplus is $ 600. (round your answer to two decimal places.) The producer surplus is $400.00. (round your answer to two decimal places.)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education