FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

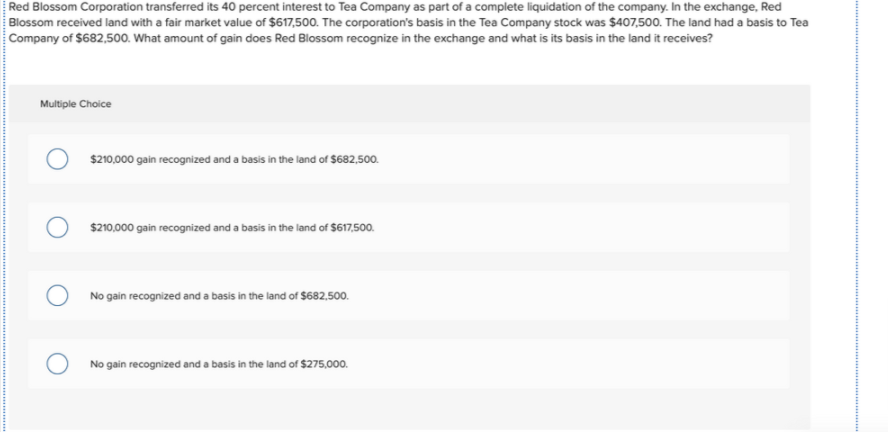

Transcribed Image Text:Red Blossom Corporation transferred its 40 percent interest to Tea Company as part of a complete liquidation of the company. In the exchange, Red

Blossom received land with a fair market value of $617,500. The corporation's basis in the Tea Company stock was $407,500. The land had a basis to Tea

Company of $682,500. What amount of gain does Red Blossom recognize in the exchange and what is its basis in the land it receives?

Multiple Choice

$210,000 gain recognized and a basis in the land of $682,500.

$210,000 gain recognized and a basis in the land of $617,500.

No gain recognized and a basis in the land of $682,500.

No gain recognized and a basis in the land of $275,000.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

Knowledge Booster

Similar questions

- Please Compute the Goodwill on the Acquisition Data. That is all of the Information that is needed for the question Also Please make sure it is correctarrow_forwardCompany X acquires 100 percent of the voting shares of Company Y for $275,000 on December 31, 2008. The fair value of the net assets of Company X at the date of acquisition was $300,000. This is an example of a(n): Select one: a. extraordinary loss b. revaluation adjustment c. bargain purchase d. positive differentialarrow_forwardSummer Company holds assets with a fair value of $125,000 and a book value of $93,000 and liabilities with a book value and fair value of $28,000. Required: Compute the following amounts if Parade Corporation acquires 65 percent ownership of Summer: a. What amount did Parade pay for the shares if no goodwill and no gain on a bargain purchase are reported? b. What amount did Parade pay for the shares if the fair value of the noncontrolling interest at acquisition is $45,150 and goodwill of $32,000 is reported? c. What balance will be assigned to the noncontrolling interest in the consolidated balance sheet if Parade pays $79,300 to acquire its ownership and goodwill of $25,000 is reported?arrow_forward

- Firm PO and Corporation QR exchanged the following business real estate: Marvin Gardens (exchanged by PO) $ 1,040,000 (715,000) 325,000 $ FMV Mortgage Equity $ Required A Required B Required: a. If PO's adjusted basis in Marvin Gardens was $403,000, compute PO's realized gain, recognized gain, and basis in Boardwalk. b. If QR's adjusted basis in Boardwalk was $78,000, compute QR's realized gain, recognized gain, and basis in Marvin Gardens. Boardwalk (exchanged Complete this question by entering your answers in the tabs below. Realized gain Recognized gain Basis $ by QR) 325,000 -0- 325,000 If PO's adjusted basis in Marvin Gardens was $403,000, compute PO's realized gain, recognized gain, and basis in Boardwalk. Amountarrow_forwardI wont solvearrow_forward[The following information applies to the questions displayed below.) Metro Corporation traded Building A for Building B. Metro originally purchased Building A for $50,000, and Building A's adjusted basis was $25,000 at the time of the exchange. What is Metro's realized gain or loss, recognized gain or loss, and adjusted basis in Building B in each of the following alternative scenarios? Note: Loss amounts should be indicated by a minus sign. Input all other amounts as positive values. Leave no answers blank. Enter zero is applicable. d. The fair market value of Building A is $45,000, and Metro trades Building A for Building B valued at $40,000 and $5,000 cash. Building A and Building B are like kind property. Description (1) Amount realized from Building B (2) Amount realized from boot (cash). (3) Total amount realized (4) Adjusted basis (5) Gain realized (6) Gain recognized (7) Deferred gain Adjusted basis in Building Br Amount S $ $ 40,000 5,000 45.000arrow_forward

- Hoolia Corporation acquires equipment and patents from another company for $50 million and records the acquisition as an asset acquisition. The equipment has a fair value of $19.20 million and the patents have a fair value of $28.80 million. Neither asset is nonqualifying. At what value does Hoolia record the equipment? Select one: a. $25.0 million b. $20.0 million c. $21.2 million d. $19.2 millionarrow_forwardOn January 1, 2021, Casey Corporation exchanged $3,300,000 cash for 100 percent of the outstanding voting stock of Kennedy Corporation. Casey plans to maintain Kennedy as a wholly owned subsidiary with separate legal status and accounting information systems. At the acquisition date, Casey prepared the following fair-value allocation schedule: Fair value of Kennedy (consideration transferred) $ 3,300,000 Carrying amount acquired 2,600,000 Excess fair value $ 700,000 to buildings (undervalued) $ 382,000 to licensing agreements (overvalued) (108,000 ) 274,000 to goodwill (indefinite life) $ 426,000 Immediately after closing the transaction, Casey and Kennedy prepared the following postacquisition balance sheets from their separate financial records (credit balances in parentheses). Accounts Casey Kennedy Cash $ 457,000 $ 172,500 Accounts receivable 1,655,000…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education