ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

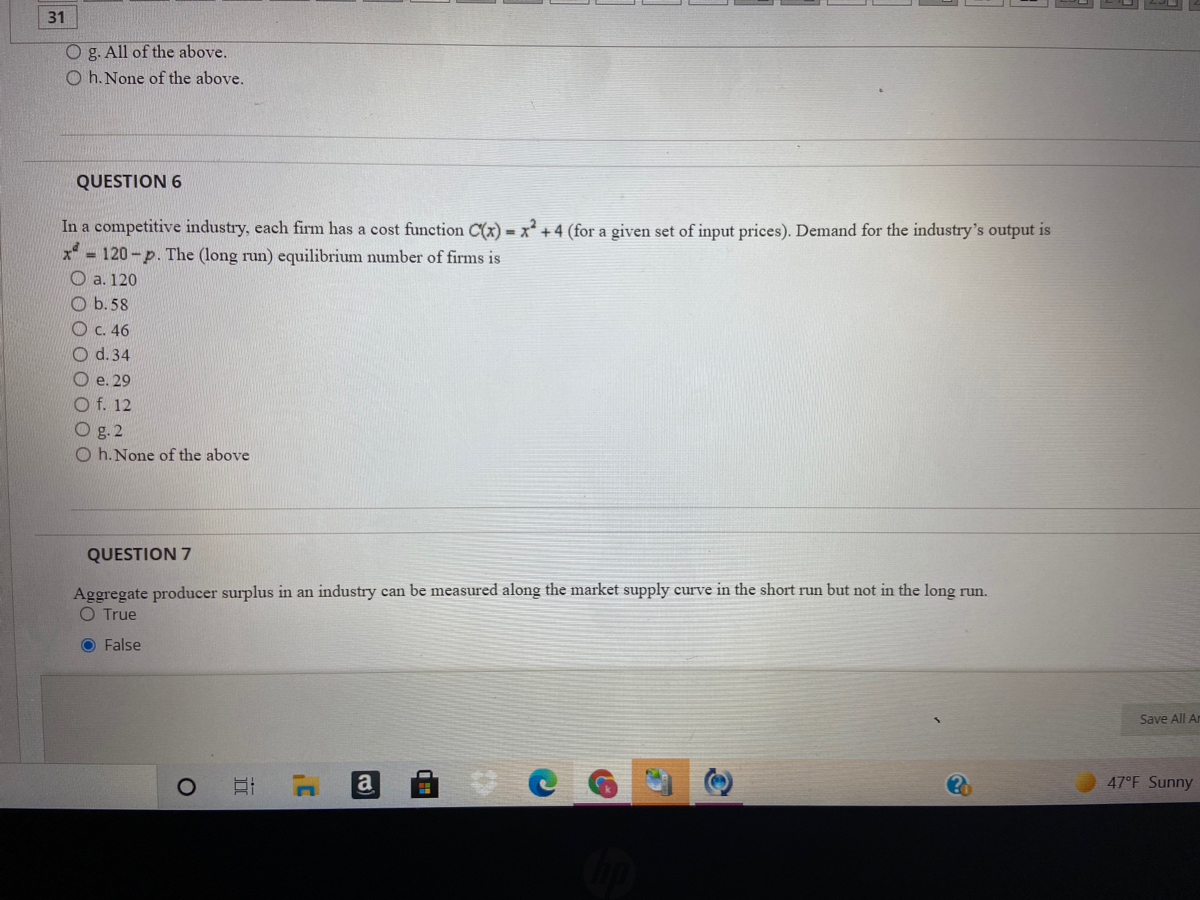

Transcribed Image Text:31

O g. All of the above.

O h. None of the above.

QUESTION 6

In a competitive industry, each firm has a cost function C(x) = x² +4 (for a given set of input prices). Demand for the industry's output is

x = 120-p. The (long run) equilibrium number of firms is

O a. 120

O b.58

C. 46

O d. 34

O e. 29

O f. 12

O g. 2

O h. None of the above

QUESTION 7

Aggregate producer surplus in an industry can be measured along the market supply curve in the short run but not in the long run.

O True

O False

Save All An

a

47°F Sunny

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- ✓ Question Completion Status: A non- competitive firm's demand curve is P = 10-4Q. So its MR is O 5-2Q O 10-40 10-8Q 05-Q QUESTION 3 For a non-competitive firm with a demand curve P = 1800-2Q and marginal costs of MC = $200, how much is the equilibrium quantity (Q)? 360 400 560 620 QUESTION 4 For a non-competitive firm with a demand curve P = 1800-2Q and marginal costs of MC = $200, how much is the equilibrium price (P*)? O $500 (4750 Click Save and Submit to save and submit. Click Save All Answers to save all answers. Save All Ararrow_forward3arrow_forwardSuppose that in a competitive market the equilibrium price is $2.50. What is marginal revenue for the last unit sold by the typical firm in this market? Select one: O a. less than $2.50 O b. more than $2.50 Oc. exactly $2.50 Od. The marginal revenue cannot be determined without knowing the actual quantity sold by the typical firm.arrow_forward

- In a perfectly competitive market, each firm has a long-run total cost given by LTC = 100Q - 10Q² + 1/2Q³. What is the market's long-run equilibrium price? 00 O 50 O25 150 4arrow_forwardThe table below describes a firm that sells output in a perfectly competitive market. Note the second column describes total costs. O $8 O $12 O $6 Output O $4 0 1 2 3 4 5 Which of the following market prices would cause the firm's profit-maximizing output level to be equal to 5? 6 Total Cost (in dollars) $3 $9 $14 $18 $23 $30 $40 4arrow_forwardBecause perfectly competitive firms are price takers, a permanent increase in the market demand does not change the price of the product in either the short run or long run. O A. True O B. Falsearrow_forward

- Figure A Competitive Firm1.2 MC ATC AVC Given Pl =$7.00 P2 $8.50 P3 =$9.20 QI=100.00 A P3 B P2 P1 MR Quantity Q1 Refer to Figure A Competitive Firm1.2. At an output level of Q1, the average fixed cost is about O $0.70 O No answer text provided. O No answer text provided. O S0.80 %24arrow_forwardFigure A Competitive Firm1.2 MC ATC Given P1 =$7.00 P2 = S8.50 P3 = SS.80 Ql = 120.00 AVC A P3 P2 P1 MR C Quantity Q1 Refer to Figure A Competitive Firm1.2. At an output level of Q1, the average fixed cost is about O $0.50 O $0.30 O No answer text provided. No answer text provided. %24arrow_forwardPrice and costs (dollars) 20 10 L O 10 20 MC O always. ATC MR 40 30 Quantity (per day) The figure above shows a perfectly competitive firm. In the short run, the firm will shut down only if the AVC of producing 10 units is more than $20. only if the AVC curve reaches its minimum before 10 units are produced. only if the AVC of producing 10 units is less than $20.arrow_forward

- 44 40 36 32 28 24 20 16 12 8 4 O a firm in a perfectly competitive market $ (c) 16 (d) 23 (e) 25 0 14 {}} 4 11 8 14 10 34 11 12 14 41 12 TH 14 D 35. What is the long-run equilibrium quantity? (a) 10 (b) 14 12 14 11 240 DET WHATH 114 IN M 421 31 ME ara 110 MI LENECE www. M IP 11 MC HE 16 20 24 31 EN MEN 28 M il ATC --AVC F 32 Qarrow_forwardConsider the perfectly competitive market for titanium. Assume that, regardless of how many firms are in the industry, every firm in the industry is identical and faces the marginal cost (MC), average total cost (ATC), and average variable cost (AVC) curves shown on the following graph. 18, 80 80 72 64 56 ATC 48 40 32 24 16 AVC 8 + MC O 3 12 15 18 21 24 27 30 QUANTITY OF OUTPUT (Thousands of pounds) COSTS (Dollars per pound)arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education