Principles of Economics 2e

2nd Edition

ISBN: 9781947172364

Author: Steven A. Greenlaw; David Shapiro

Publisher: OpenStax

expand_more

expand_more

format_list_bulleted

Related questions

Question

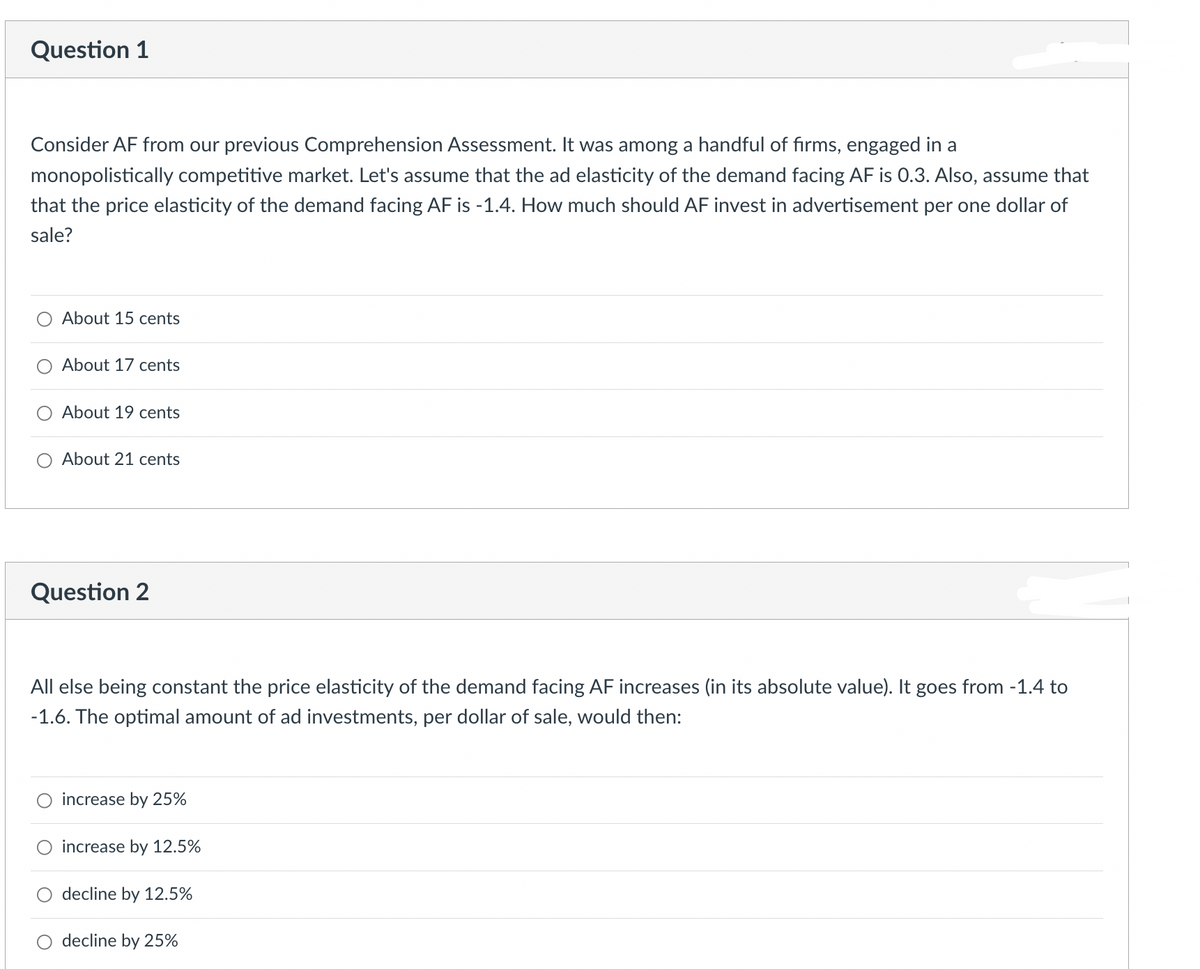

Transcribed Image Text:Question 1

Consider AF from our previous Comprehension Assessment. It was among a handful of firms, engaged in a

monopolistically competitive market. Let's assume that the ad elasticity of the demand facing AF is 0.3. Also, assume that

that the price elasticity of the demand facing AF is -1.4. How much should AF invest in advertisement per one dollar of

sale?

About 15 cents

About 17 cents

About 19 cents

About 21 cents

Question 2

All else being constant the price elasticity of the demand facing AF increases (in its absolute value). It goes from -1.4 to

-1.6. The optimal amount of ad investments, per dollar of sale, would then:

increase by 25%

increase by 12.5%

○ decline by 12.5%

decline by 25%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Similar questions

- Assuming you are the managing director of a firm that produces three goods: A, Band C. The price elasticity of demand for A is 1.2, for B it is 1.00 and for C it is 0.75.It is known that he firm is experiencing serious cash flow problems and you have toincrease total revenue as soon as possible. If you were in a position to set the pricesfor these goods, what would be your pricing strategy for each productarrow_forwardurgentttt needarrow_forwarder to the information provided in Figure 15.2 below to answer the questions that follo Demand and cost conditions for We Do Hair MC ATC 32 28 24 20 MR 40 46 50 60 Number of perms b. 1) Refer to Figure 15.2. The profit-maximizing number of perms for We Do Hair, a monopolistically competitive firm, is 2) Refer to Figure 15.2. At We Do Hair, a monopolistically competitive firm, the profit- maximizing price for a perm is 3) Refer to Figure 15.2. If We 1Do Hair is maximizing profit as a monopolistically competitive firm, it is earning a profit of 4) Refer to Figure 15.2. If We Do Hair is maximizing profit as a monopolistically competitive firm, its total revenue equals 5) Refer to Figure 15.2. If We Do Hair is maximizing profit as a monopolistically competitive firm, its total costs are 6) Refer to Figure 15.2. From society's point of view, the efficient level of output is 7) Refer to Figure 15.2. In this monopolistically competitive industry, in the long run, Acessibility: Investigate D…arrow_forward

- PRICE (Dollars per engine) 100 90 80 70 60 40 30 & 2 20 10 MO D 0 10 ATC MR Demand 20 30 40 50 60 70 DO 90 QUANTITY (Thousands of engines) 100 Mon Comp Outcome Min Unit Cost Because this market is a monopolistically competitive market, you can tell that it is in long-run equilibrium by the fact that optimal quantity. Furthermore, a monopolistically competitive firm's average total cost in long-run equilibrium is average total cost. at the the minimumarrow_forwardexplains it correctltarrow_forwardSuppose that a firm produces wool jackets in a monopolistically competitive market. The following graph shows its demand curve, marginal revenue (MR) curve, marginal cost (MC) curve, and average total cost (ATC) curve. Place a black point (plus symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm. Next, place a grey point (star symbol) to indicate the minimum average total cost the firm faces and the quantity associated with that cost. (?) PRICE (Dollars perjacket) 100 90 80 70 60 50 40 30 20 10 0 0 MC 10 ATC MR 20 30 40 50 80 70 QUANTITY (Thousands of jackets) 80 Demand 90 100 O F ++ Mon Comp Outcome Min Unit Cost hp earrow_forward

- Solve all this question......you will not solve all questions then I will give you down?? upvotearrow_forward2arrow_forwardWould you rather have efficiency or variety? That is, one opportunity cost of the variety of products we have is that each product costs more per unit than if there were only one kind of product of a given type, like shoes. Perhaps a better question is, What is the right amount of variety? Can there be too many varieties of shoes, for example?arrow_forward

- Suppose the local electrical utility, a legal monopoly based on economies of scale, was split into four films of equal size, with the idea that eliminating the monopoly would promote competitive pricing of electricity. What do you anticipate would happen to prices?arrow_forwardΣ B. 20 10 50 30 20 PRICE (Dollars per bat) Homework (C (91. 4. Is monopolistic competition efficient? Suppose that a firm produces baseball bats in a monopolistically competitive market. The following graph shows its demand curve, marginal revenue (MR) curve, marginal cost (MC) curve, and average total cost (ATC) curve. Place a black point (plus symbol) on the graph to indicate the long-run monopolistically competitive equilibrium price and quantity for this firm. Next, place a grey point (star symbol) to indicate the minimum average total cost the firm faces and the quantity associated with that cost. 06 Mon Comp Outcome Min Unit CAst 09 40 10 MR Demand pleuwe 09 06 QUANTITY (Thousands of bats) Because this market is a monopolistically competitive market, you can tell that it is in long-run equilibrium by the fact that ▼ at the optimal eticall the miair MacBook Pro ACID & 5. R H N command commarrow_forwardStudy Tools ins ess Tips ss Tips PRICE (Dellars per engine) 288 RSS #RR 100 50 30 20 10 MO 0 0 10 ATC MR Demand 20 30 40 50 70 DO 90 QUANTITY (Thousands of engines) 100 Mon Comp Outcome Min Unt Cost Decause this market is a monopolistically competitive market, you can tell that it is in long-run equilibrum by the fact that optimal quantity. Furthermore, a monopolistically competitive firm's average total cost in long-run equilibrium is average total cost. at the the minimumarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Principles of Economics 2eEconomicsISBN:9781947172364Author:Steven A. Greenlaw; David ShapiroPublisher:OpenStax

Principles of Economics 2e

Economics

ISBN:9781947172364

Author:Steven A. Greenlaw; David Shapiro

Publisher:OpenStax