ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:es Mailings Review View Help

a v

v

Po E-E-FEAT

也。

Paragraph

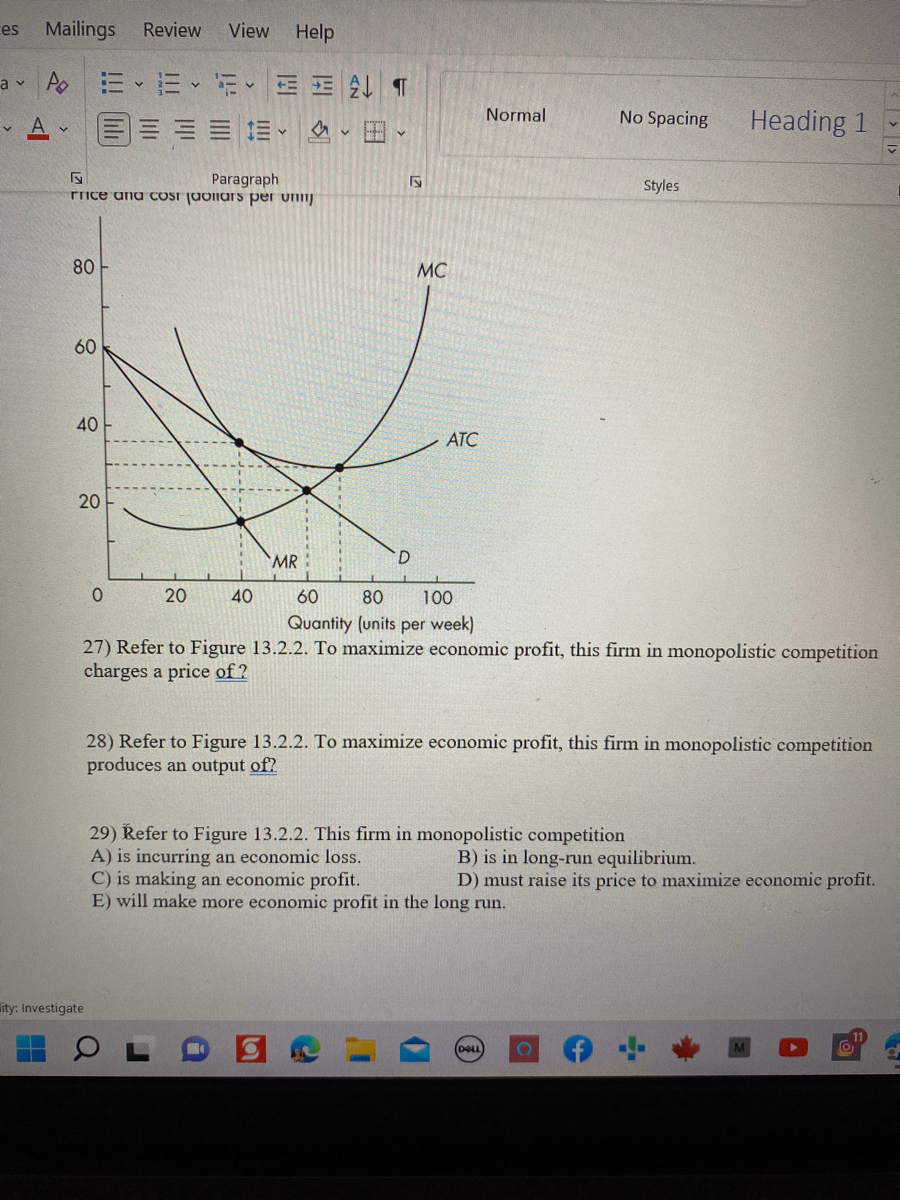

rrice and cost Jaollars per uni

80

60

40

20

ity: Investigate

V

D

0

20

40

60

80 100

Quantity (units per week)

27) Refer to Figure 13.2.2. To maximize economic profit, this firm in monopolistic competition

charges a price of ?

28) Refer to Figure 13.2.2. To maximize economic profit, this firm in monopolistic competition

produces an output of?

29) Refer to Figure 13.2.2. This firm in monopolistic competition

A) is incurring an economic loss.

B) is in long-run equilibrium.

C) is making an economic profit.

D) must raise its price to maximize economic profit.

E) will make more economic profit in the long run.

(DELL)

O

O

J

MR

MC

Normal

ATC

No Spacing

Styles

Heading 1

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Question 37 A monopolistically competitive firm cannot make strictly negative profits in the long run because The firm’s optimal quantity is to produce where marginal revenue equals marginal cost The firm must operate at the efficient scale Either the firm exits or the exit of other firms shifts its demand curve to the right, raising profits until it makes zero profits. Exit of other firms shifts the market supply curve to the left and raises the price until firms make zero profitsarrow_forwardThe accompanying graph depicts average total cost (ATC) marginal cost (MC), marginal revenue (M), and demand (D) 50 facing a monopolistically competitive firm MC 45 Place point A at the firm's profit maximizing price and quantity 40 35 What is the firm's total cost? ATC 30 25 total cost: 20 15 What is the firm's total revenue? 10 5 total revenue: $ MR 0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95100 Quantity What is the firm's total profit? profit: $ Price and Cost ($)arrow_forwardQUESTION 13 A monopolistic competitive firm. a)As presented in Exhibit, the long-run profit-maximizing output for the monopolistic competitive firm is? b) To maximize long-run profits, the monopolistically competitive firm shown in Exhibit will charge a price per unit of ?arrow_forward

- The figure below shows the demand (D, MR) and cost (MC, ATC) curves for Gwen's Country Curtains, operating in a monopolistically competitive industry. Demand and cost conditions facing Gwen's Country Curtains MC Dollars 80 0 ATC 1,000 MR Number of curtains per month Suppose Gwen's Country Curtains is currently producing 1000 curtains per month at a price of $80. In the short run, this company is and in the long run, it should expect to a. earning zero profit; earn zero profit b. suffering a loss; earn zero profit c. suffering a loss; shut down d. making a profit; earn zero profitarrow_forwardWataDine is one of a city’s many restaurants that serve lunch and dinner in a monopolistically competitive market. Assume WataDine, as a typical restaurant in the city, is currently producing the profit-maximizing output level, and earns positive short-run economic profit. (a) How is monopolistic competition similar to each of the following market structures? (i) Perfect competition (ii) Monopoly (b) WataDine is currently earning short-run economic profits. Draw a correctly labeled graph for WataDine in short-run equilibrium and show each of the following. (i) The profit-maximizing quantity, labeled QM (ii) The profit-maximizing price, labeled PM (c) Given that WataDine is currently earning short-run economic profits, what will happen to each of the following in the long run? (i) WataDine's economic profit. Explain. (ii) WataDine's demand curve for its restaurant meals. (d) Assume WataDine is in long-run equilibrium. (i) Is WataDine taking advantage of its economies of scale? Explain.…arrow_forwardThis profit-maximizing firm will produce Blank 1 units. What price will this profit-maximizing firm charge? $Blank 2 (Do NOT enter the '$' in your response. Enter only the whole dollar amount; do NOT enter cents.) If the industry was perfectly competitive instead of monopolistic, then market output would be Blank 3 units and market price would be $Blank 4. (Do NOT enter the '$' in your response. Enter only the whole dollar amount; do NOT enter cents.)arrow_forward

- botharrow_forward#3) Draw a diagram of the long run equilibrium in a monopolistically competitive market. How is price related to average total cost? How is price related to marginal cost?arrow_forwarda) Can the threat of a price war deter entry by potential competitors? What actions might a firm take to make this threat credible? b)Why is the firm’s demand curve flatter than the total market demand curve in monopolistic competition? Suppose a monopolistically competitive firm is making a profit in the short run. What will happen to its demand curve in the long run?arrow_forward

- Answer choices are first blank: negative, positive, zero second blank: an equal number of, fewer, morearrow_forwardSuppose the market for toothpaste is monopolistically competitive and in? long-run equilibrium. The demand? (and marginal? revenue) for a firm in this industry is illustrated in thearrow_forwardThe information below provides conditions faced by a monopolistically competitive firm. Price and costs $70 $65 $60 $55 $50 $45 $40 $40 $35 $30 $25 $250 $20455 $15 $10 $5 0 $32.50 MIR Quantity MC ATC Demand Use the information above to answer the following question. This monopolistically competitive firm's economic profit/loss is $.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education