Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

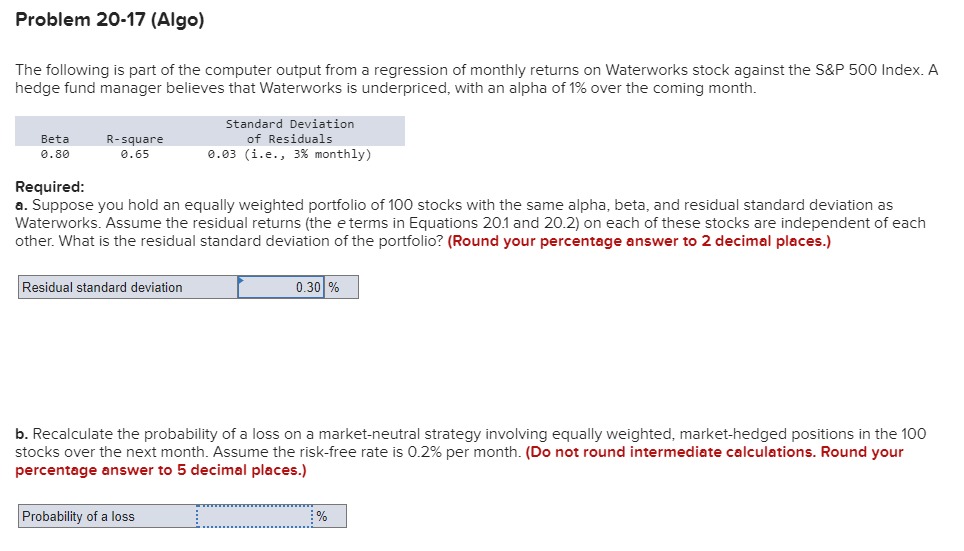

Transcribed Image Text:Problem 20-17 (Algo)

The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 Index. A

hedge fund manager believes that Waterworks is underpriced, with an alpha of 1% over the coming month.

Beta

0.80

R-square

0.65

Required:

a. Suppose you hold an equally weighted portfolio of 100 stocks with the same alpha, beta, and residual standard deviation as

Waterworks. Assume the residual returns (the e terms in Equations 20.1 and 20.2) on each of these stocks are independent of each

other. What is the residual standard deviation of the portfolio? (Round your percentage answer to 2 decimal places.)

Residual standard deviation

Standard Deviation

of Residuals

0.03 (1.e., 3% monthly)

Probability of a loss

0.30 %

b. Recalculate the probability of a loss on a market-neutral strategy involving equally weighted, market-hedged positions in the 100

stocks over the next month. Assume the risk-free rate is 0.2% per month. (Do not round intermediate calculations. Round your

percentage answer to 5 decimal places.)

%

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Required: Using Table 5.3 as your guide, what is your estimate of the expected annual HPR on the market index stock portfolio if the current risk- free interest rate is 4.3% ? (Round your answer to 2 decimal places.) Answer is complete but not entirely correct. 0.120 Expected annual HPR TABLE 5.3 Risk and return of investments in major asset classes, 1927-2018 Average Risk premium Standard deviation max min T-bills 3.38 na 3.12 14.71 -0.02 T-bonds 5.83 2.45 11.59 41.68 -25.96 Stocks 11.72 8.34 20.05 57.35 -44.04arrow_forwardUse the following information to calculate the expected return and standard deviation of a portfolio that is 60 percent invested in 3 Doors, Incorporated, and 40 percent invested in Down Company: Note: Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places. Expected return, E(R) Standard deviation, o Correlation Expected return Standard deviation 3 Doors, Incorporated 16% 46 0.31 2.00% 2.00% Down Company 24% 48arrow_forwardQuantitative Problem: You are holding a portfolio with the following investments and betas: Stock Dollar investment Beta A $300,000 1.2 B 200,000 1.6 C 400,000 0.75 D 100,000 -0.35 Total investment $1,000,000 The market's required return is 11% and the risk-free rate is 4%. What is the portfolio's required return? Do not round intermediate calculations. Round your answer to three decimal places.arrow_forward

- Prudent Bank holds a stock in its portfolio which has the following discrete probability distribution of payoffs: Probability Payoff 33.0 65.5 0.5 0.013 0.987 ($ millions) Answer: 28 36 40 -300 -532 At a 99 % confidence level, what is the Expected Shortfall? (Please only provide the magnitude of Expected Shortfall, i.e. without a minus sign, and round your answer to two decimal places in terms of millions of dollars - please do not show the $ sign in the answer. e.g. if the answer is -$2.134 million, enter 2.13)arrow_forwardThe expected return and standard deviation of a portfolio that is 50 percent invested in 3 Doors, Incorporated, and 50 percent invested in Down Company. are the following: Expected return, E(R) Standard deviation, o 3 Doors, Incorporated 14% 42 Correlation +1 Correlation 0 Correlation-1 What is the standard deviation if the correlation is +1? 0? -1? Note: Do not round intermediate calculations. Enter your answers as a percent rounded to 2 decimal places. Standard Deviation 33.61 % Down Company 10% 31 %arrow_forwardProblem 20-17 (Algo) The following is part of the computer output from a regression of monthly returns on Waterworks stock against the S&P 500 Index. A hedge fund manager believes that Waterworks is underpriced, with an alpha of 1% over the coming month. Beta 0.60 R-square 0.65 Required: a. Suppose you hold an equally weighted portfolio of 100 stocks with the same alpha, beta, and residual standard deviation as Waterworks. Assume the residual returns (the e terms in Equations 20.1 and 20.2) on each of these stocks are independent of each other. What is the residual standard deviation of the portfolio? (Round your percentage answer to 2 decimal places.) Residual standard deviation Standard Deviation of Residuals 0.06 (1.e., 6% monthly) Probability of a loss b. Recalculate the probability of a loss on a market-neutral strategy involving equally weighted, market-hedged positions in the 100 stocks over the next month. Assume the risk-free rate is 1.3% per month. (Do not round intermediate…arrow_forward

- A portfolio manager believes that credit spreads are mean-reverting in the medium term. The manager observes the following information about four corporate issues: Issue 1 2 3 4 O O 1 2 3 Current Spread (bps) 6 month mean spread 4 100 60 130 200 Based on this information, which issue is best to purchase according to mean reversion analysis? 90 90 110 220 6 month spread st.dev. 10 25 15 30arrow_forwardIf a portfolio manager expects the market to go down by 2% next year, which stock should the manager buy? (these are betas) A. -1B. - .5 C. OD. 1E. 2arrow_forwardDetailed steps pls all parts or skiparrow_forward

- aa.3arrow_forwardConsider a position consisting of 200,000 investment in asset A and 300,000 investment in asset B. Assume that the daily volatility of the assets are 1.5% and 1.8% respectively, and that coefficient of correlation between their returns is 0.4. What is the five day 95% VAR for the portfolio (given 95% confidence level represents 1.65 standard deviations on the left side of the normal distribution)?arrow_forwardmni.0arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education