ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

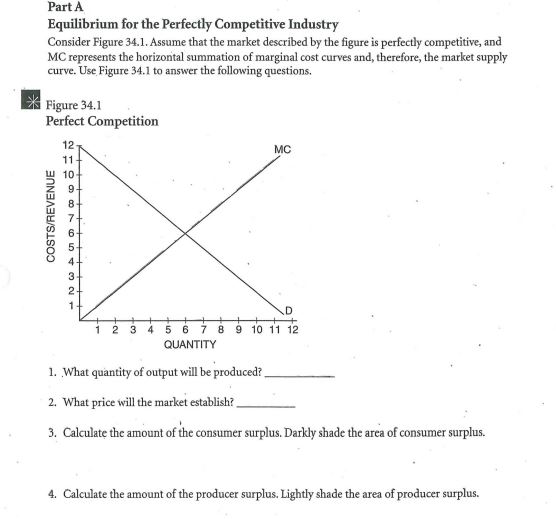

Transcribed Image Text:Part A

Equilibrium for the Perfectly Competitive Industry

Consider Figure 34.1. Assume that the market described by the figure is perfectly competitive, and

MC represents the horizontal summation of marginal cost curves and, therefore, the market supply

curve. Use Figure 34.1 to answer the following questions.

Figure 34.1

Perfect Competition

12

MC

11

10

9.

3

2-

1-

1 2 3 4 56 7 8 9 10 11 12

QUANTITY

1. What quantity of output will be produced?

2. What price will the market establish?

3. Calculate the amount of the consumer surplus. Darkly shade the area of consumer surplus.

4. Calculate the amount of the producer surplus. Lightly shade the area of producer surplus.

COSTS/REVENUE

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- part 3 4.............arrow_forwardConsider the perfectly competitive market for sports jackets. The following graph shows the marginal cost ( MCMC ), average total cost ( ATCATC ), and average variable cost ( AVCAVC ) curves for a typical firm in the industry.arrow_forward67. In a perfectly competitive market, industry demand is given by Q = 1000 – 20P. The typical firm’s average cost is TC = 300 + Q2 /3, and marginal cost by MC = (2/3)Q. Suppose there are 10 identical firms in the market. What is the market supply? A. 30Q B. 40Q C. 15Q D. 5Qarrow_forward

- Use the figure below to answer the following question. Total revenue and total cost (dollars) 400 300 Z 200 100 Q 0 99 Quantity Figure 12.2.1 Refer to Figure 12.2.1, which shows a perfectly competitive firm's total revenue and total cost curves. Which one of the following statements is false? A) At an output of Q1 units a day, the firm makes zero economic profit. B) At an output less than Q1 units a day, the firm incurs an economic loss. OC) At an output of Q2 units a day, the firm incurs an economic loss. D) Economic profit is the vertical distance between the total revenue curve and the total cost curve. E) At an output greater than Q3 units a day, the firm incurs an economic loss. Main Contentarrow_forwardA firm producing ice pop in a perfectly competitive market with an equilibrium price of $1.50 has the following Quantity of ice Total Cost pops 0 $3 10 $8.00 20 20 $10.50 30 $15.50 59 40 $30.50 50 $50.50 60 60 $75.50 70 70 $105.50 What is this firm's marginal revenue from the 50th unit? MR(50) = $ What is this firm's marginal revenue from the 60th unit? MR(60) = $arrow_forwardurgentarrow_forward

- Question 5 Let's suppose that a perfectly competitive firm has the following revenue and cost data. How many products should the firm produce in order to maximize its profits? You can assume that the firm's price is greater than its average variable cost. Quantity Marginal Revenue Marginal Cost 40 $4 $7.70 41 $4 $5.10 42 $4 $3.30 43 $4 $2.10 44 $4 $2.50 45 $4 $3.70 46 $4 $4.10 47 $4 $5.20 48 $4 $10 Question 6 What is the profit maximizing (or loss minimizing) rule for a firm in perfect competition? Be sure to list all of the conditions.arrow_forwardQUESTION 11 Consider the following setup for a perfectly competitive market: Suppose that for the firm, TC=625+ Q² and MC=20, and for the industry, demand is given by P= 100-Q and supply is given by S=Q. Solve for the market output and corresponding price. O Q=50, P-50 O Q=25, P=75 O Q=75, P=25 O Q=50, P=25arrow_forward3. Consider the perfectly competitive markets for bottled water in two cities, A and B. Both have a downward-sloping demand curve and upward-sloping supply curve, and each market is currently in long run equilibrium at the same price. The demand curves are similar, but in city A the supply curve is more price elastic than in city B. a) There's a shock: an accident causes the tap water in the area to become undrinkable. In two diagrams, one for each city, compare the effect on price and quantity traded in the two cities, assuming that a new equilibrium is reached. Explain your diagrams. b) Following on from your answer to a), explain what would happen in the model to the number of suppliers and their profitability, in each of the short run and the long run.arrow_forward

- Assume that a firm in a perfectly competitive industry has the following total cost schedule: Calculate a marginal cost and an average cost schedule for the firm to complete the following table. Output Total Cost Marginal Cost Average Cost (units) ($) ($) ($) 10 440 15 600 20 720 25 900 30 1,200 35 1,540 40 1,920 If the prevailing market price is $68 per unit, units will be produced. Profits per unit will be and total profits will be . Is the industry in long-run equilibrium at this price? No Yesarrow_forward3arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education