FINANCIAL ACCOUNTING

10th Edition

ISBN: 9781259964947

Author: Libby

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Related questions

Question

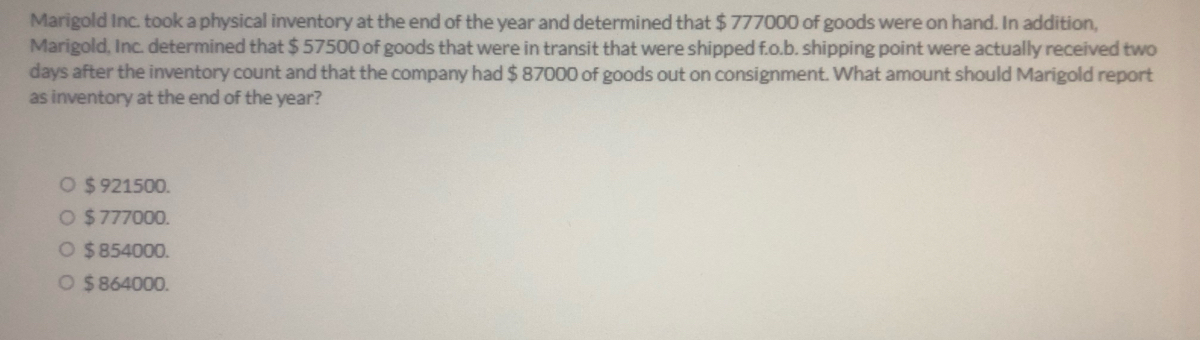

Transcribed Image Text:Marigold Inc. tookaphysical inventory at the end of the year and determined that $777000 of goods were on hand. In addition,

Marigold, Inc. determined that $ 57500 of goods that were in transit that were shipped f.o.b. shipping point were actually received two

days after the inventory count and that the company had $ 87000 of goods out on consignment. What amount should Marigold report

as inventory at the end of the year?

O $ 921500.

O $777000.

O $854000.

O $864000.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Jones Company started the year with no inventory. During the year, it purchased two identical inventory items at different times. The first purchase cost $1,170 and the other, $1,550. Jones sold one of the items during the year. Required Based on this information, how much product cost would be allocated to cost of goods sold and ending inventory on the year-end financial statements, assuming use of a. FIFO? b. LIFO? c. Weighted average? Cost of goods sold Ending inventory $ FIFO 1,170 LIFO $ 1.170 Weighted Averagearrow_forwardWhispering Winds Corporation uses a perpetual inventory system and had inventory worth $88,500 at the beginning of the year. Purchases were made during the year for $393,000; however, 10% of these goods were returned to the supplier, and a 3% discount was taken on the remaining balance owing. Whispering Winds paid $3,500 cash for freight to ship the inventory to its location during the year. Whispering Winds reported cost of goods sold for the year of $295,000. Whispering Winds has a calendar year end. What is the balance in the inventory account at the end of the year? Balance If Whispering Winds counted its actual inventory balance as $118,000 at the end of the year, what adjusting entry, if any, would be made? (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. List all debit entries before credit entries.) Date Account Titles and…arrow_forwardBonita Inc. took a physical inventory at the end of the year and determined that $845000 of goods were on hand. In addition, the following items were not included in the physical count. Bonita, Inc. determined that $98000 of goods purchased were in transit that were shipped f.o.b. destination (goods were actually received by the company three days after the inventory count). The company sold $39000 worth of inventory f.o.b. destination that did not reach the destination yet. What amount should Bonita report as inventory at the end of the year? $982000. $943000. $845000. $884000.arrow_forward

- TS Quilts Inc. took a physical inventory at the end of the year and determined that $414,000 of goods were on hand. TS Inc. determined that $12,000 of goods held and included in the court were being held on consignment from PDJ outlet. Additionally, because of high rates of return on some products, TS has established an estimate of items that will be returned of $17,000. What amount should TS report in their year-end balance sheet for the inventory account?arrow_forwardVibrant Company had $970,000 of sales in each of Year 1, Year 2, and Year 3, and it purchased merchandise costing $535,000 in each of those years. It also maintained a $270,000 physical inventory from the beginning to the end of that three-year period. In accounting for inventory, it made an error at the end of Year 1 that caused its Year 1 ending inventory to appear on its statements as $250,000 rather than the correct $270,000. 1. Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3. 2. Prepare comparative income statements to show the effect of this error on the company's cost of goods sold and gross profit for each of Year 1, Year 2, and Year 3. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3. VIBRANT COMPANY Comparative Income Statements Year 2 Cost of goods sold Cost of goods sold Gross profit Year 1…arrow_forwardThe following is an independent error made by a company that uses the periodic inventory system: Equipment with a book value of $70,000 and a fair value of $100,000 was sold at the beginning of the year. A 2-year, non-interest-bearing note for $129,960 was received and recorded at its face value, and a gain of $59,960 was recognized. No interest revenue was recorded and 14% is a fair rate of interest. What is the journal entry needed to correct the sale of equipment? Ignore income taxesWhat is the journal entry adjustment needed to correct interest related to the note?arrow_forward

- S Vibrant Company had $1,050,000 of sales in each of Year 1, Year 2, and Year 3, and it purchased merchandise costing $575,000 in each of those years. It also maintained a $350,000 physical inventory from the beginning to the end of that three-year period. In accounting for inventory, it made an error at the end of Year 1 that caused its Year 1 ending inventory to appear on its statements as $330,000 rather than the correct $350,000. 1. Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3. 2. Prepare comparative income statements to show the effect of this error on the company's cost of goods sold and gross profit for each of Year 1, Year 2, and Year 3. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Prepare comparative income statements to show the effect of this error on the company's cost of goods sold and gross profit for each of Year 1, Year 2 Year 3. Cost of goods sold Cost of goods sold Gross…arrow_forwardWildhorse Company took a physical inventory on December 31 and determined that goods costing $676,000 were on hand. Not included in the physical count were $9,000 of goods purchased from Sandhill Corporation, f.o.b. shipping point, and $29,000 of goods sold to Ro-Ro Company for $37,000, f.o.b. destination. Both the Sandhill purchase and the Ro-Ro sale were in transit at year-end. What amount should Wildhorse report as its December 31 inventory? December 31 Inventory $ %24arrow_forwardManjiarrow_forward

- Vibrant Company had $1,040,000 of sales in each of Year 1, Year 2, and Year 3, and it purchased merchandise costing $570,000 in each of those years. It also maintained a $340,000 physical inventory from the beginning to the end of that three-year period. In accounting for inventory, it made an error at the end of Year 1 that caused its Year 1 ending inventory to appear on its statements as $320,000 rather than the correct $340,000. 1. Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3. 2. Prepare comparative income statements to show the effect of this error on the company's cost of goods sold and gross profit for each of Year 1, Year 2, and Year 3. Complete this question by entering your answers in the tabs below. Required 1 Required 2 Determine the correct amount of the company's gross profit in each of Year 1, Year 2, and Year 3. Cost of goods sold Cost of goods sold Gross profit Year 1 0 $ VIBRANT COMPANY Comparative Income Statements…arrow_forwardDengerarrow_forwardDelta Apparel Inc. uses a perpetual inventory system. At the beginning of the year inventory amounted to $ 50,000. During the year, the company purchased merchandise for $ 230,000 and sold merchandise costing $ 245,000. A physical inventory taken at year-end indicated shrinkage losses of $4,000. Prior to the recording of these shrinkage losses, the year-end balance in the companys Inventory account was :- a. $ 31,000 b. $ 35,000 c. $ 50,000 d. $ 55,00arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Accounting Information Systems

Accounting

ISBN:9781337619202

Author:Hall, James A.

Publisher:Cengage Learning,

Horngren's Cost Accounting: A Managerial Emphasis...

Accounting

ISBN:9780134475585

Author:Srikant M. Datar, Madhav V. Rajan

Publisher:PEARSON

Intermediate Accounting

Accounting

ISBN:9781259722660

Author:J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher:McGraw-Hill Education

Financial and Managerial Accounting

Accounting

ISBN:9781259726705

Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting Principles

Publisher:McGraw-Hill Education