ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:K

possible

A

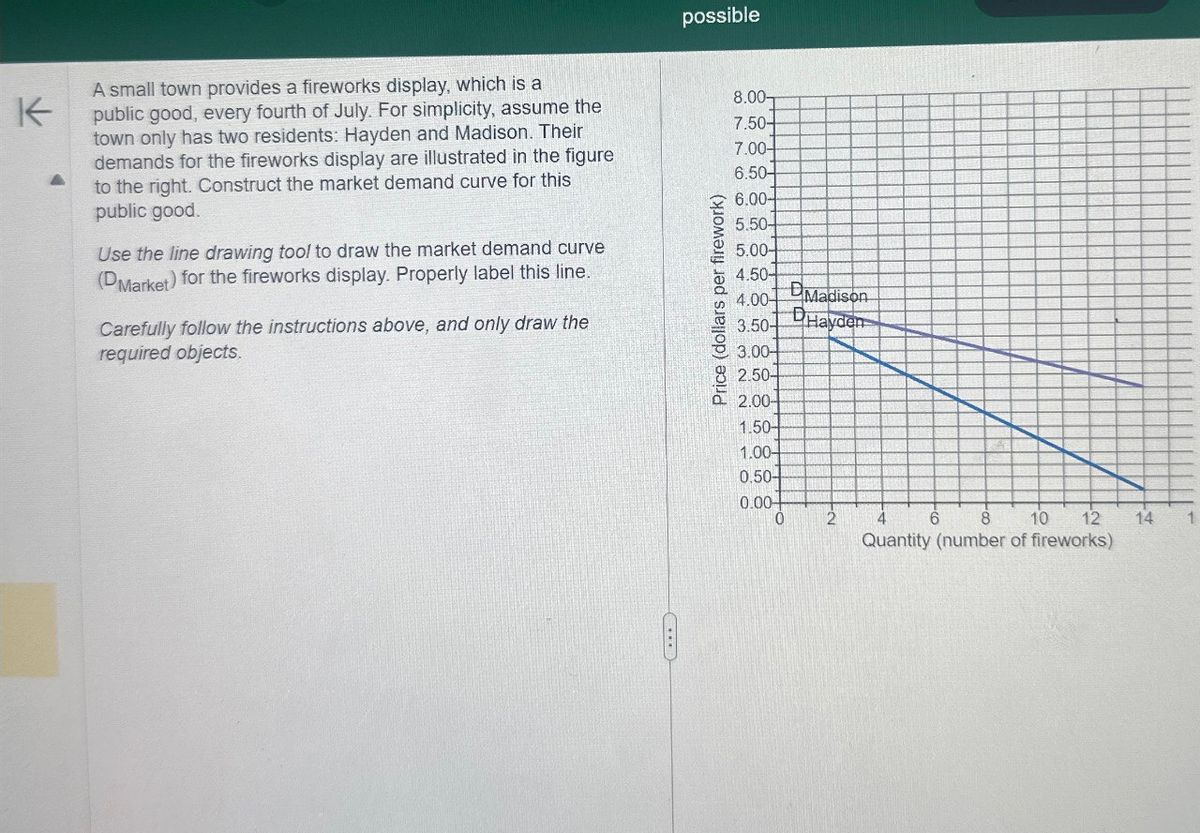

A small town provides a fireworks display, which is a

public good, every fourth of July. For simplicity, assume the

town only has two residents: Hayden and Madison. Their

demands for the fireworks display are illustrated in the figure

to the right. Construct the market demand curve for this

public good.

Use the line drawing tool to draw the market demand curve

(DMarket) for the fireworks display. Properly label this line.

Carefully follow the instructions above, and only draw the

required objects.

Price (dollars per firework)

8.00T

7.50-

7.00-

C

6.50-

6.00-

5.50-

5.00-

4.50-

4.00-

3.50-

Madison

Hayden

3.00-

2.50-

2.00-

1.50

1.00-

0.50-

0.00

0

2

4

6

8

10

12

14

1

Quantity (number of fireworks)

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Similar questions

- For each of the events described below, sketch a supply and demand graph that illustrates the event. Be sure to properly label all curves and relevant points in your graph. In the area to the left of your graph, explain why you think your graph is correct. In that area, also answer the questions asked. (a) E-cigarettes. Multiple credible reports are published detailing the adverse health effects of e-cigarettes (vaping). This is new information: the e-cig industry had been basing its advertising around alleged health benefits of e-cigarettes over tobacco products. What is the effect on the price of e-cigarettes? On the quantity of e-cigarettes sold per month?arrow_forward1. Which of the following variables does not directly impact the quantity of a good the firm is willing to produce? a. the price of the good b. the income level of the people who buy the good c. the number of firms producing the good d. the cost of a key input used to produce the goodarrow_forward11) Draw a supply and demand graph, properly label all curves and axes. Then draw the effect of a forest fire on the market for lumber. Clearly mark how quantity and price changearrow_forward

- Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardQ2 Solve in 5 minarrow_forward4: What are five fundamental questions (and answers) in economics? Five fundamental questions How do market system answer the question? 1. 2. 3. 4. 5. Chapter 3 starts here. Define "demand" and State the law of demand. Demand is a (s (w_ specified period of (t d ) or a curve which shows the various amounts of a product buyers are ) to purchase at each price in a series of possible prices during a ) and (a ). Demand portrays relationship between ), they are (positively, negatively) related either in the table or in the ( graph ). The law of demand states that, other things being equal, as price increases, the corresponding quantity demanded (rises, falls). Restated, there is a (an) ( direct, inverse ) relationship between price and ) and ( q. quantity demanded with everything else held constant.arrow_forward

- 1. Externalities - Definition and examples An externality arises when a firm or person engages in an activity that affects the wellbeing of a third party, yet neither pays nor receives any compensation for that effect. If the impact on the third party is adverse, it is called a externality. The following graph shows the demand and supply curves for a good with this type of externality. The dashed drop lines on the graph reflect the market equilibrium price and quantity for this good. Adjust one or both of the curves to reflect the presence of the externality. If the social cost of producing the good is not equal to the private cost, then you should drag the supply curve to reflect the social costs of producing the good; similarly, if the social value of producing the good is not equal to the private value, then you should drag the demand curve to reflect the social value of consuming the good. ? PRICE (Dollars per unit) QUANTITY (Units) Supply Demand Demand Supply With this type of…arrow_forwardPROBLEM (5) (tariff) The domestic (US) demand and supply for soy is p = 80 − QD and p = QS + 10 respectively. US market is very small relative to the world market, and the world (equilibrium) price is $20. Draw one graph for the market marking all intercepts and intersections to help you with (a) and (b) below. (a) If there is NO trade, what is the CS, PS, net domestic benefits, DWL?(b) If there is free trade, what is the CS, PS, net domestic benefits, DWL? How many units are imported? Now the state imposes a tariff of t dollars per unit.(c) What should be the tariff amount t to maximize tariff revenues? In this case, what is the DWL?(d) What should be the tariff amount t so that consumers and producers equally well off (CS equals PS)? (e) What should be the tariff amount t to maximize PS?(f) What is the most efficient tariff amount t? What is the least efficient tariff amount t? (i.e. that minimizes and maximizes DWL respectively.)arrow_forwardi will 10 upvotes.arrow_forward

- do fastarrow_forwardplease do it quick i need it as soon as possible.(3) Sketch a supply and demand model of the housing (home ownership) market. Label the equilibrium price and equilibrium quantity. Now sketch in TWO changes on the same graph: an increase in demand; a reduction in supply.arrow_forwardV surplus is the difference between the highest price a consumer is willing to and the price the consumer actually pays. This component of economic surplus is illustrated in the diagram to the right by area Do Quantity (per time period)arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education