Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Concept explainers

Question

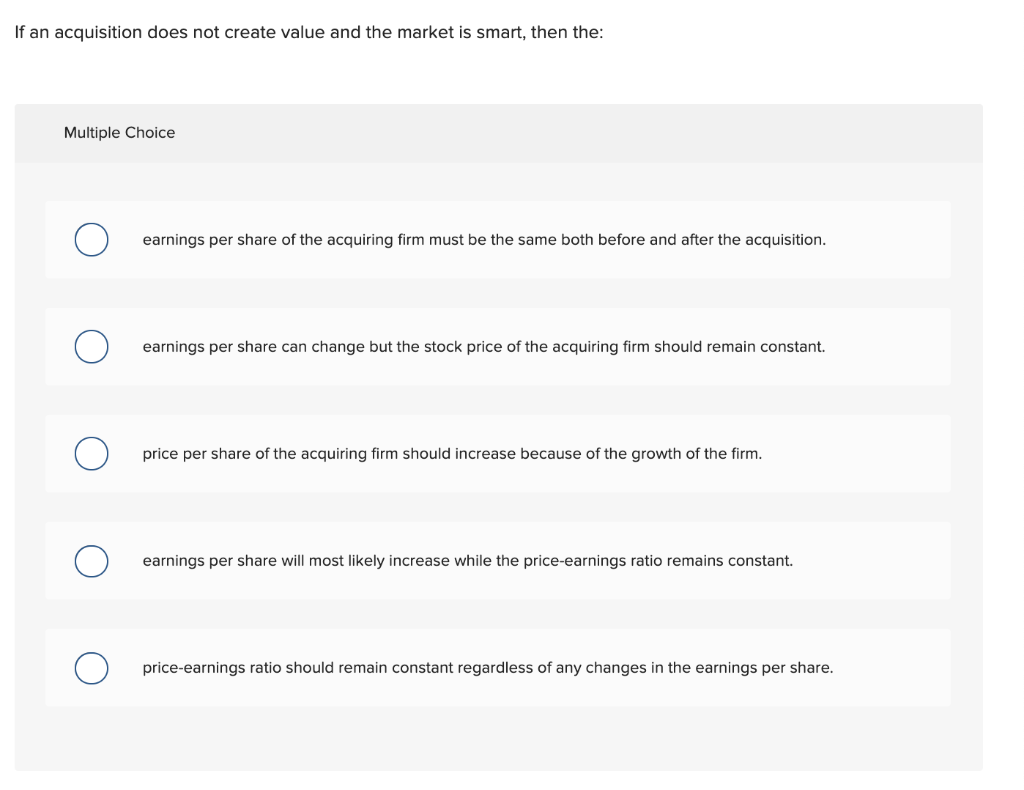

Transcribed Image Text:If an acquisition does not create value and the market is smart, then the:

Multiple Choice

earnings per share of the acquiring firm must be the same both before and after the acquisition.

earnings per share can change but the stock price of the acquiring firm should remain constant.

price per share of the acquiring firm should increase because of the growth of the firm.

earnings per share will most likely increase while the price-earnings ratio remains constant.

price-earnings ratio should remain constant regardless of any changes in the earnings per share.

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- Which statement below is incorrect? Select one: A. Compared to interview, survey is more suitable to ask standardised questions. B. If a firm has more intangible assets, according to the trade-off theory, it is more likely to have a higher leverage. C. If a firm is more profitable, according to the pecking order theory, it should use less debt for financing. D. The CAPM model implies that a stock with a higher beta has a higher return on average.arrow_forwardIf the Modigliani and Miller hypothesis about dividends is correct, and if one found a group of companies which differed only with respect to dividend policy, which of the following statements would be most correct? Group of answer choices None of these statements is true. All of these statements are true. The total expected return, which in equilibrium is also equal to the required return, would be higher for those companies with lower payout ratios because of the greater risk associated with capital gains versus dividends. If the expected total return of each of the sample companies were divided into a dividend yield and a growth rate, and then a scatter diagram (or regression) analysis were undertaken, then the slope of the regression line (or b in the equation D1/P0 = a + b(g)) would be equal to +1.0. The residual dividend model should not be used, because it is inconsistent with the MM dividend hypothesis.arrow_forwardSolve this onearrow_forward

- "Address the limitations of traditional methods such as CAPM (Capital Asset Pricing Model) andDiscounted Cash Flow Analysis in valuing a company's stock price in non - stationary marketconditions. Particularly, discuss the consistency of the beta coefficient in determining the cost ofcapital and the selection of the risk - free rate. Also, evaluate how these traditional models can orcannot integrate non-financial factors (e. g., company management, brand value, industry trends).Lastly, discuss the alternative models used in stock valuation and the advantages and disadvantagesof these models compared to traditional methods."arrow_forwardWhat are the conditions for stock market efficiency? Is it possible that market for individual stocks could be highly efficient but market for whole companies could be less efficient? Explainarrow_forwardTrue or False: The following statement accurately describes how firms make decisions related to issuing new common stock. Taking flotation costs into account will reduce the cost of new common stock. False: Flotation costs are additional costs associated with raising new common stock. True: Taking flotation costs into account will reduce the cost of new common stock, because you will multiply the cost of new common stock by 1 minus the flotation cost-similar to how the after-tax cost of debt is calculated Alpha Moose Transporters is considering investing in a one-year project that requires an initial investment of $475,000. To do so, it will have issue new common stock and will incur a flotation cost of 2.00%. At the end of the year, the project is expected to produce a cash inflow of $550,000. The rate of return that Alpha Moose expects to earn on its project (net of its flotation costs) is (rounded to two decimal places) Sunny Day Manufacturing Company has a current stock price of…arrow_forward

- 5. Nonconstant growth stock As companies evolve, certain factors can drive sudden growth. This may lead to a period of nonconstant, or variable, growth. This would cause the expected growth rate to increase or decrease, thereby affecting the valuation model. For companies in such situations, you would refer to the variable, or nonconstant, growth model for the valuation of the company's stock. Consider the case of Portman Industries: Portman Industries just paid a dividend of $2.88 per share. The company expects the coming year to be very profitable, and its dividend is expected to grow by 20.00% over the next year. After the next year, though, Portman's dividend is expected to grow at a constant rate of 4.00% per year. Assuming that the market is in equilibrium, use the information just given to complete the table. Term Value Dividends one year from now (D1) $3.46 Horizon value (P) $29.32 Intrinsic value of Portman's stock $29.34 ▼ The risk-free rate (rRF) is 5.00%, the market risk…arrow_forwardIf a firm plans to issue new stock, flotation costs (investment bankers' fees) should not be ignored. There are two approaches to use to account for flotation costs. The first approach is to add the sum of flotation costs for the debt, preferred, and common stock and add them to the initial investment cost. Because the investment cost is increased, the project's expected rate of return is reduced so it may not meet the firm's hurdle rate for acceptance of the project. The second approach involves adjusting the cost of common equity as follows: Cost of equity from new stock = r, D1 +8 Po(1-F) The difference between the flotation-adjusted cost of equity and the cost of equity calculated without the flotation adjustment represents the flotation cost adjustment. Quantitative Problem: Barton Industries expects next year's annual dividend, D1, to be $1.90 and it expects dividends to grow at a constant rate g = 4.3%. The firm's current common stock price, Po, is $25.00. If it needs to issue…arrow_forwardGive your thoughts on the prompts below Firms use market capitalization when considering the market value added. We have seen that a number of things can affect capitalization values, so is this really the best method to use? A well known company recently had a 20-1 stock split that drew a lot of attention...how does this affect their market value added? Administrative errors can have a big impact in receivables turnover and payment delay ratios, so companies should include administrative and other indirect costs in the calculations of those ratios. Agree or Disagree and defend your answer.arrow_forward

- M-M theroy with perfect market suggests that divident payment: A.It dependes on the company's capital structure and retained earnings B.Has a positive impact on the value of a firm C.Has a negative impact on the value of a firm D.Has no impact on the value of a firmarrow_forwardWhen an acquirer assesses a potential target, the price the acquirer is willing to pay should be based on the value of: The target firm’s total corporate value (debt and equity) The target firm’s equity The target firm’s debt Consider the following scenario: Ziffy Corp. is considering an acquisition of Keedsler Motors Co., and estimates that acquiring Keedsler will result in incremental after-tax net cash flows in years 1–3 of $14.00 million, $21.00 million, and $25.20 million, respectively. After the first three years, the incremental cash flows contributed by the Keedsler acquisition are expected to grow at a constant rate of 6% per year. Ziffy’s current beta is 1.60, but its post-merger beta is expected to be 2.08. The risk-free rate is 5%, and the market risk premium is 7.10%. Based on this information, complete the following table by selecting the appropriate values (Note: Do not round intermediate calculations, but round your answers to two decimal places): Value…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education