ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

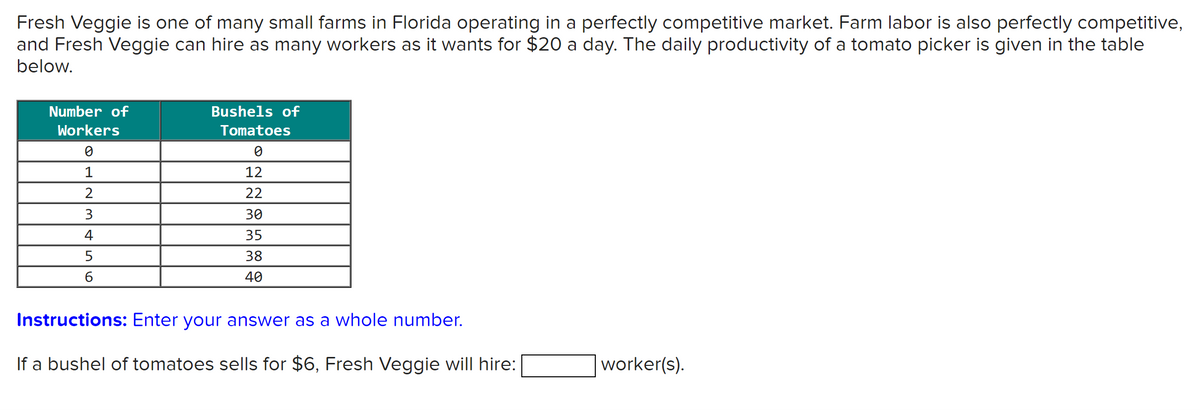

Transcribed Image Text:Fresh Veggie is one of many small farms in Florida operating in a perfectly competitive market. Farm labor is also perfectly competitive,

and Fresh Veggie can hire as many workers as it wants for $20 a day. The daily productivity of a tomato picker is given in the table

below.

Number of

Workers

0

1

2

3

4

5

6

Bushels of

Tomatoes

0

12

22

30

35

38

40

Instructions: Enter your answer as a whole number.

If a bushel of tomatoes sells for $6, Fresh Veggie will hire:

worker(s).

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Only typed answerarrow_forwardNote: The answer should be typed.arrow_forwardComplete the following statement about the marginal productivity theory. For a firm that is a factor price taker, _____ , And firms hire the factor quantity at which _____. Thus, it follows that _____. Suppose that Manuel works for Clear Drop Co, a perfectly competitive firm producing water filters. Manuel was paid $3,000 but found a better job and quit Clear Drop. Since nothing else changed, Clear Drop's total revenue _____. Blank 1: a. MFC = P b. MFC = 0 c. MFC < P d. MFC > P Blank 2: a. MRP = MFC b. MRP = 0 c. MRP < MFC d. MRP > MFC Blank 3: a. W = MRP b. W < MRP c. W > MRP Blank 4: a. does not change as well b. falls by $1,500 c. falls by $3,000 d. rises by $1,500 e. rises by $3,000arrow_forward

- (This is a single question with five parts to the answer. I would appreciate help with all five parts if possible. Image screenshot of the original question with the formulas more easily readable than can be identified here is attached) Tech firms produce goods and services from labor and energy. The total cost in dollars to produce y amount of goods and services for each firm j is cj(yj) = yi2. There are 100 identical tech firms which all behave competitively. What is the individual supply of technological goods and services? What is the market supply of technological goods and services? Suppose the demand curve for these goods is D(p)=200-50p. What is the equilibrium price and quantity sold? How much is the total surplus of this economy? Now suppose that the industry makes a one-time investment for $K amount of dollars to innovate in a new technology of production that allows every firm to reduce its cost of production to a 1/4 fraction of the previous cost. What is the new total…arrow_forwardGM cuts jobs at its Australian manufacturing unit GM will cut 500 jobs, or about 12% of its workforce, at its Australian plant because of a sharp fall in demand for its locally-made "Cruze" small car. Source: The Wall Street Journal, April 8, 2013 As GM cuts its workforce, how will the marginal product and average product of a worker change in the short run? Suppose that before the cuts the marginal product of GM workers is below their average product. As the number of workers decreases, the marginal product of a GM worker and the average product of a GM worker in the short run. increases; decreases does not change; does not change decreases; decreases increases; increases decreases; increasesarrow_forwardSolve all questions compulsory..arrow_forward

- ONLY answer question b. relative to question a.arrow_forwardpshotic 166& 5. Profit maximization and shutting down in the short run Suppose that the market for microwave ovens is a competitive market. The following graph shows the daily cost curves of a firm operating in this market. 100 90 80 ATC 70 60 40 30 AVC 20 10 MC 5 10 15 20 25 30 35 40 45 50 QUANTITY (Thousands of ovens) Σ 50 PRICE (Dollars per oven)arrow_forwardConsider the same firm from the Monday assignment but now let's call that cost schedule total variable cost. Q 1 2 3 4 5 6 7 8 9 TVC 12 20 24 28 34 42 52 64 78 And let's imagine that there is fixed costs of 18 which is sunk in the short run. a. Show this firm's average total cost, average variable cost and marginal cost on a graph. Indicate the efficient scale (I don't think the book uses the words "efficient scale" but it's the quantity where profit would be zero when P=MC. We will discuss what I mean by "efficient scale but probably not before Thursday. By "indicate" I mean give the quantity and MC. I don't need every point to be exactly to scale, I just care about the general shape of the curves, where things cross and the location and…arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education