ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

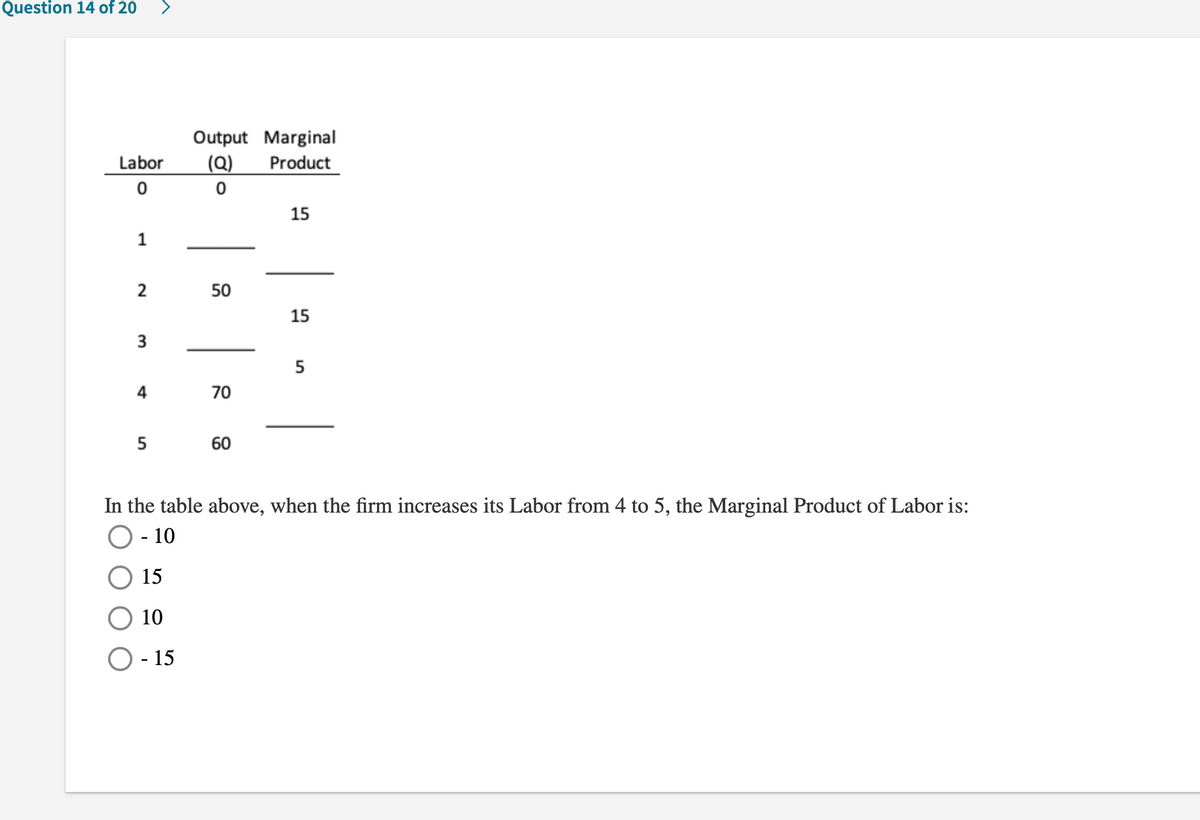

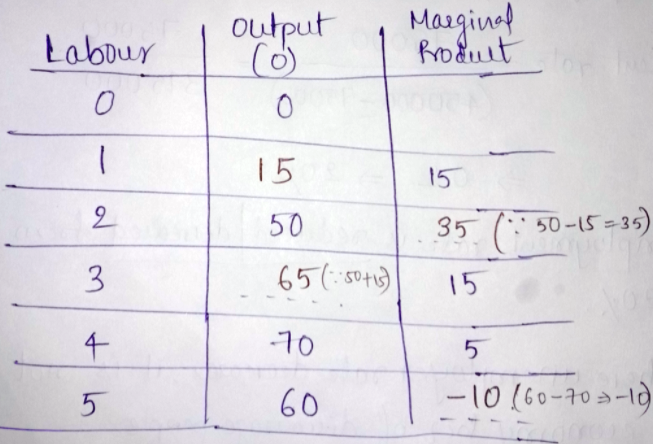

Transcribed Image Text:Question 14 of 20

Output Marginal

Labor

(Q)

Product

15

1

2

50

15

4

70

5

60

In the table above, when the firm increases its Labor from 4 to 5, the Marginal Product of Labor is:

O - 10

15

10

O - 15

Expert Solution

arrow_forward

Step 1

Step by stepSolved in 2 steps with 2 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- QUESTION 4 When Total Product of labors (TPL) is maximized then: O Average product (APL) equals zero Marginal product (MPL) equals zero O Marginal product (MPL) is maximized O Average product (APL) is maximizedarrow_forwardThe next 3 questions refer to the following: Labour Output 0 0 of 2 10 4 stion 26 6 46 8 65 10 72 12 80 14 86 Marginal Product when the number of workers increases from 2 to 4 workers is Marginal Product is maximized when the firm hires workers. Average Product is maximized when the firm hires workers. units.arrow_forwardCalculate the Average Total Cost for points A & B. Input (Labor) Output TFC TVC TC MC ATC AVC 4. 50 $125 $15 85 $125 $30 O A-S35 -525.83 O 4:52.80 B-5182 OA-S0.36 B-50.s OAS250 BS147 Question 4 Calculate the Average Variable Cost for points A &B Input (Labor) Output TFC TVC TC MC ATC AVC 4. 50 $125 $15 85 $125 $30 OA52.50 -4147 OAS030 -5035arrow_forward

- If the Marginal Product of Labor(MPL) for the 2nd worker is 500 units. What is the firms average Fixed Cost (FC) of producing 1,500 gadgets?arrow_forward3. (14 points) Let the production function be Q(K,L)=2K L. The cost of one unit of labor is w, the cost of one unit of capital is r, and the quanitity to produce is y. (a) (4 points) Set up the firm's cost-minimization problem, and clearly write down the con- Page 6 straint the firm faces. The cost minimization problem of the firm is min(KL) WL+rK. The constraint: y=2K!L!. anscribed Text (b) (5 points) What are two conditions that the optimal bundle L and K need to satisfy? Write down their expressions. Tangency: -=-; production: y = 2(K)! (L)!. (c) (5 points) Solve for the optimal bundle of L. and K that minimizes the firm's cost at y=144 by finding L and K", assuming that w $16 and r $81. By solving the system of two conditions in Part (b), it should be not that hard to get L = 162 and K* = 32.arrow_forwardBozo is a clown. He wants to start a clowning business where he sends other clowns out to birthday parties. Use the graph to Birthday parties answer the questions. 20 19 18 17 16 15 14 13 12 What is the marginal product of the third worker? O 2 11 10 6. 8. 7. 3.0 9. 3. 2. I 2 3 9 10 4 56 8. This production function demonstrates Workers diminishing marginal costs. a negative marginal product of labor. diminishing marginal returns to labor. diminishing output.arrow_forward

- A company has the following production function for its product, f(k, I) = k"/2/1/2. It faces input prices v = 5 for capital and w = 20 for labor. How much does the firm use of each input if it wants to produce 10 units of its product? O a. I= 4, k = 25 O b. / = 5, k = 20 O c. 1= 20, k = 5 O d. 1= 25, k = 4 Clear my choice Suppose the market demand for a good is Qº = 2000 – 8p and market supply is QS = 5p + 700. There are 10 %3D firms with exactly the same cost function. How much does each firm produce? O a. 100 O b. 120 O c. 140 O d. 200 Clear my choicearrow_forwardTable 3 Gallo Cork Factory Number of Workers 1 2 3 4 5 6 7 Number of Machines 2 2 2 2 2 2 2 Output (corks produced per hour) 5 10 20 35 55 70 80 Select one: O a. the fifth worker O b. the fourth worker O c. the third worker O d. the sixth worker Marginal Product of Labor Cost of Cost of Workers Machines Total Cost Refer to Table 3. Gallo's cork factory experiences diminishing marginal product of labor with the addition of which worker?arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education