Related questions

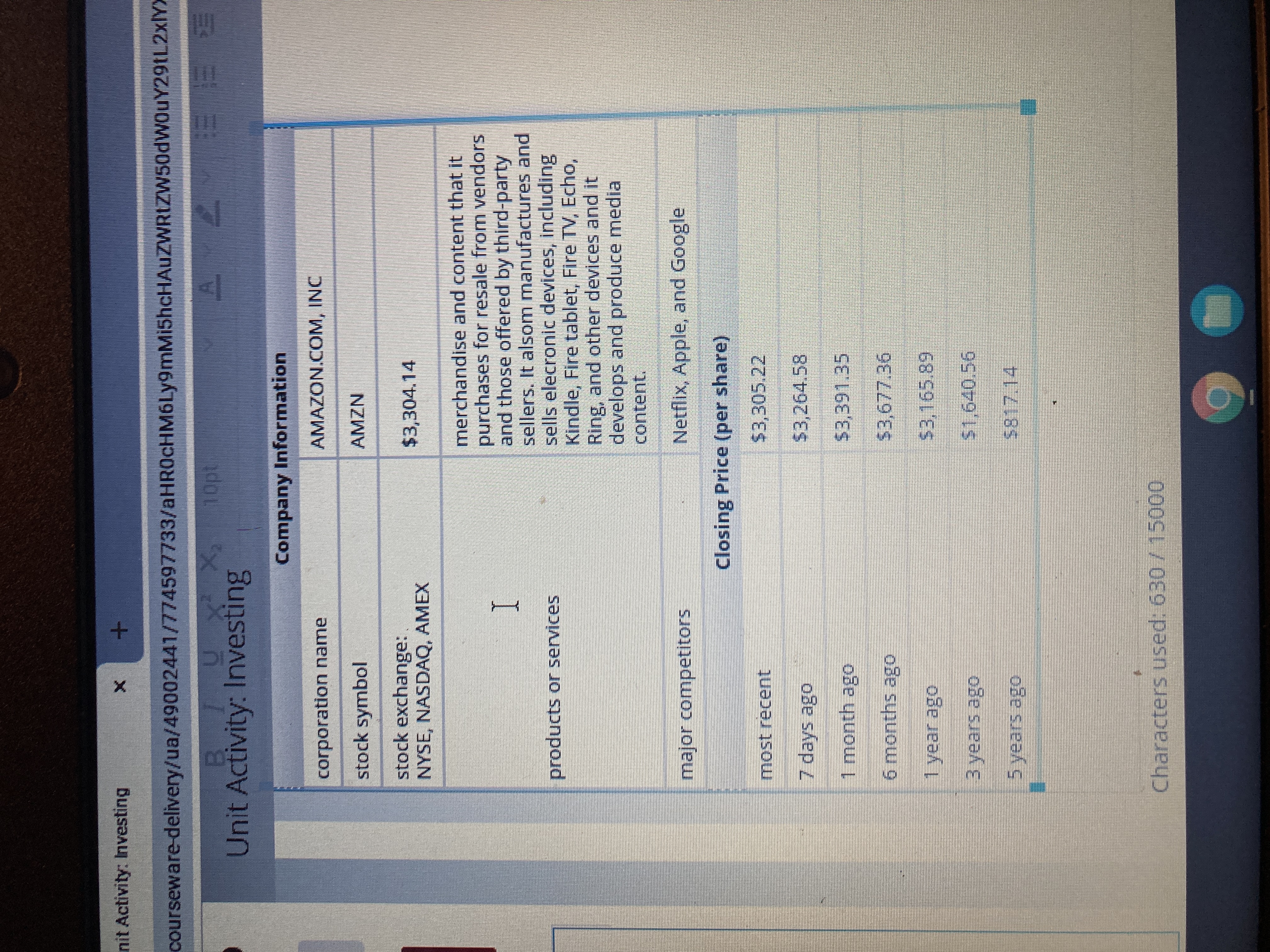

Use the times and corresponding closing prices of the stock to create coordinate pairs. Let x represent the number of weeks since the first data point, and let y represent the closing price at each time. So, x=0 represents the data point from 5 years ago. There are 52 weeks in a year, and you can write the time for each closing price recorded in terms of weeks that have passed since 5 years ago, when x=0. Fill in the table to represent your data as coordinate pairs.

x (weeks since 5 yrs ago)

most recent 260

7days ago 259

1 month ago 256

6 months ago 234

1 year ago 208

3 years ago 104

5 years ago 0

y (closing price, in $)

most recent

7 days ago

1 month ago

6 months ago

1 year ago

3 years ago

5 years ago

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps with 1 images

- Look up the daily trading volume for the following stocks during a recent five-day period: • Merck • Caterpillar • Intel • McDonald’s • General Electric Randomly select five stocks from the NYSE, and examine their daily trading volume for the same five days. a. What are the average volumes for the two samples? b. Would you expect this difference to have an impact on the efficiency of the markets for the two samples? Why or why not?arrow_forwardYou plan to simulate a portfolio of investments over a multiyear period, so for each investment (which could be a particular stock or bond, for example), you need to simulate the change in its value for each of the years. How would you simulate these changes in a realistic way? Would you base it on historical data? What about correlations? Do you think the changes for different investments in a particular year would be correlated? Do you think changes for a particular investment in different years would be correlated? Do you think correlations would play a significant role in your simulation in terms of realism?arrow_forward(Computing rates of return) From the following price data, compute the annual rates of return for Asman and Salinas. Time 1 2 3 12 4 14 (Click on the icon in order to copy its contents into a spreadsheet.) How would you interpret the meaning of the annual rates of return? Asman $9 11 Salinas $30 27 32 36 The rate of return you would have earned on Asman stock from time 1 to time 2 is %. (Round to two decimal places.)arrow_forward

- Suppose the average return on Asset A is 6.6 percent and the standard deviation is 8.6 percent and the average return and standard deviation on Asset B are 3.8 percent and 3.2 percent, respectively. Further assume that the returns are normally distributed. Use the NORMDIST function in Excel® to answer the following questions. a. What is the probability that in any given year, the return on Asset A will be greater than 11 percent? Less than 0 percent? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) b. What is the probability that in any given year, the return on Asset B will be greater than 11 percent? Less than 0 percent? (Do not round intermediate calculations and enter your answers as a percent rounded to 2 decimal places, e.g., 32.16.) c-1. In a particular year, the return on Asset A was −4.25 percent. How likely is it that such a low return will recur at some point in the future? (Do…arrow_forwardhe last four years of returns for a stock are as shown here: LOADING... . a. What is the average annual return? b. What is the variance of the stock's returns? c. What is the standard deviation of the stock's returns? Note: Notice that the average return and standard deviation must be entered in percentage format. The variance must be entered in decimal format. Question content area bottom Part 1 a. What is the average annual return? The average return is enter your response here%. (Round to two decimal places.) Part 2 b. What is the variance of the stock's returns? The variance of the returns is enter your response here. (Round to five decimal places.) Part 3 c. What is the standard deviation of the stock's returns? The standard deviation is enter your response here%. (Round to two decimal places.) Time Remaining: 00:26:16 pop-up content starts Data table (Click on the following icon in order…arrow_forwardThe market and Stock J have the following probability distributions: Probability rM rJ 0.3 15.00 % 19.00 % 0.4 10.00 6.00 0.3 18.00 10.00 The data has been collected in the Microsoft Excel Online file below. Open the spreadsheet and perform the required analysis to answer the questions below. Open spreadsheet Calculate the expected rate of return for the market. Do not round intermediate calculations. Round your answer to two decimal places.fill in the blank %Calculate the expected rate of return for Stock J. Do not round intermediate calculations. Round your answer to two decimal places.fill in the blank % Calculate the standard deviation for the market. Do not round intermediate calculations. Round your answer to two decimal places.fill in the blank %Calculate the standard deviation for Stock J. Do not round intermediate calculations. Round your answer to two decimal places.fill in the blank %arrow_forward

- You are given the following returns on "the market" and Stock F during the last three years. We could calculate beta using data for Years 1 and 2 and then, after Year 3, calculate a new beta for Years 2 and 3. How different are those two betas, i.e., what's the value of beta 2 - beta 1? (Hint: You can find betas using the Rise-Over-Run method, or using your calculator's regression function.) Year Market Stock F 1 6.10% 19.50% 2 12.90% −3.70% 3 16.20% 21.71% A. 10.96 B. 10.91 C. 11.06 D. 11.01 E. 11.11 Note:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forwardEach month for the past several years, you have collected the monthly returns to an index of large-cap value stocks and an index of large-cap growth stocks. For the last two years, for both of the indexes you have converted these monthly returns into a series of rolling average annualized returns by taking an average of the previous 12 monthly returns and multiplying that average by 12. These rolling average annualized returns are shown below for each index over the past 24 months. Month value Index AnnualizedReturn (%) growth index annualized returns (%) 1 9.36 % 9.14 % 2 17.14 16.72 3 25.40 28.15 4 17.66 13.46 5 18.19 14.79 6 18.35 15.09 7 18.68 13.20 8 17.21 9.91 9 18.21 11.23 10 21.32 15.61 11 28.84 21.93 12 22.55 18.79 13 25.67 24.21 14 21.84 16.74 15 22.65 19.34 16 24.98 25.11 17 28.11 26.08 18 28.99 28.09 19 18.77 21.52 20 22.10 24.20 21 24.15 22.37…arrow_forwardThe last four years of returns for a stock are as shown here: a. What is the average annual return? b. What is the variance of the stock's returns? c. What is the standard deviation of the stock's returns? Note: Notice that the average return and standard deviation must be entered in percentage format. The variance must be entered in decimal format.arrow_forward

- This is a three-part question. Answer to part one is 2.4%; please help me solve for parts two and three. Thank you.arrow_forward4. Expected dividends as a basis for stock values The following graph shows the value of a stock's dividends over time. The stock's current dividend is $1.00 per share, and dividends are expected to grow at a constant rate of 3.50% per year. The intrinsic value of a stock should equal the sum of the present value (PV) of all of the dividends that a stock is supposed to pay in the future, but many people find it difficult to imagine adding up an infinite number of dividends, Calculate the present value (PV) of the dividend paid today (De) and the discounted value of the dividends expected to be paid 10, 20, and 50 years from now (Dio, Dao, Duo). Assume that the stock's required return (r.) is 10.40%. Note: Carry and round the calculations to four decimal places. Time Period Now End of Year 10 End of Year 20 End of Year 50 Dividend's Expected Future Value Dividend's Expected Present Value Using the orange curve (square symbols), plot the present value of each of the expected future…arrow_forwardYou find a certain stock that had returns of 16 percent, −23 percent, 24 percent, and 9 percent for four of the last five years. The average return of the stock over this period was 10.2 percent. a. What was the stock’s return for the missing year? (Do not round intermediate calculations and enter your answer as a percent rounded to 1 decimal place, e.g., 32.1.) b. What is the standard deviation of the stock’s returns? (Do not round intermediate calculations and enter your answer as a percent rounded to 2 decimal places, e.g., 32.16.)arrow_forward

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education