Related questions

Randolph Company reported pretax net income from continuing operations of $959,000 and taxable income of $590,000. The book–tax difference of $369,000 was due to a $205,000 favorable temporary difference relating to

b. Compute Randolph Company’s

c. Compute Randolph Company’s effective tax rate.

Deferred income tax is a liability to the company which arises due to differences in tax laws and accounting methods, the total tax expense is not equal to tax reported.

Trending nowThis is a popular solution!

Step by stepSolved in 3 steps

- Livia Company’s pretax income was $72,000. To compute taxable income, the following information is provided: Excess of estimated bad debts over write-offs $26,000 Penalty for late filing of income taxes 21,000 Excess of tax depreciation over accounting depreciation 36,000 Tax rate 20% What is the current portion of income tax? $12,400 $6200 $16,600 $22,600arrow_forwardam.115.arrow_forwardSol Limited. reported earnings of $510,000 in 20X8. The company has $91,000 of depreciation expense this year, and claimed CCA of $142,000. The tax rate was 25%. At the end of 20X7, there was a $122,000 loss carryforward that was not recorded because use was considered less than probable. The company also reported a deferred tax liability of $71,000 caused by capital assets with a net book value of $1,310,000 and UCC of $1,010,000. The tax rate had been 20% in 20X7. Required:What is the amount of income tax expense in 20X8? Prepare the income tax entry or entries. - Record the entry income tax expense. - Record the entry loss carryforward.arrow_forward

- For its first year of operations, Tringali Corporation's reconciliation of pretax accounting income to taxable income is as follows: Pretax accounting income $ 300,000 Permanent difference (15,000 ) 285,000 Temporary difference-depreciation (20,000 ) Taxable income $ 265,000 Tringali's tax rate is 25%. Assume that no estimated taxes have been paid. What should Tringali report as its deferred income tax liability as of the end of its first year of operations?arrow_forward11. Ace Company had a pretax accounting income of P5,000,000 for its first year of operations. The following differences are noted between accounting income and taxable income: 1) Nondeductible expenses - 200,000; 2) Nontaxable revenue - 500,000; 3) Gross income on installment sales reported in accounting income but not in taxable income - 1,000,000; 4) Provision for doubtful accounts - 100,000; and 5) Income tax rate - 30%. COMPUTE THE FOLLOWING: 1. Accounting income subject to tax; 2) Taxable income; 3) Total income tax expense; and 4) Current tax expense.arrow_forwardStone Company reported pre-tax book income of $700,000 in 20X1, the first year of operation. The tax depreciation exceeded the book depreciation by $90,000. The tax rate for 20X1 and all future years was 21%. What amount of deferred tax liability should Stone report in its December 31, 20X1, balance sheet? Select one: a. $6,300 b. $14,000 c. $18,900 d. $3,500arrow_forward

- Hopkins Co. at the end of 2010, its first year of operations, prepared a reconciliation between pretar financial income and taxable income as follows: Pretax financial income S 750.000 Estimated litigation expense 1,000,000 Extra depreciation for taxes (1.500.000) Taxable income 5.250.000 The estimated litigation expense of $1,000,000 will be deductible in 2011 when it is expected to be paid. Use of the depreciable assets will result in taxable amounts of $500,000 in each of the next three years. The income tax rate is 30% for all years. Income tax payable is Select one: a. $75,000. b. S0. C $150,000. d. $225,000.arrow_forwardQ.11.arrow_forwardRequired information [The following information applies to the questions displayed below.] Hafnaoui Company reported pretax net income from continuing operations of $903,500 and taxable income of $712,500. The book-tax difference of $191,000 was due to a $242,000 favorable temporary difference relating to depreciation, an unfavorable temporary difference of $117,000 due to an increase in the reserve for bad debts, and a $66,000 favorable permanent difference from the receipt of life insurance proceeds. b. Compute Hafnaoui Company's deferred income tax expense or (benefit). Note: Enter all numbers as a positive number and indicate whether a deferred tax expense or a deferred tax benefit. X Answer is complete but not entirely correct. Deferred income tax expense $ 712,500arrow_forward

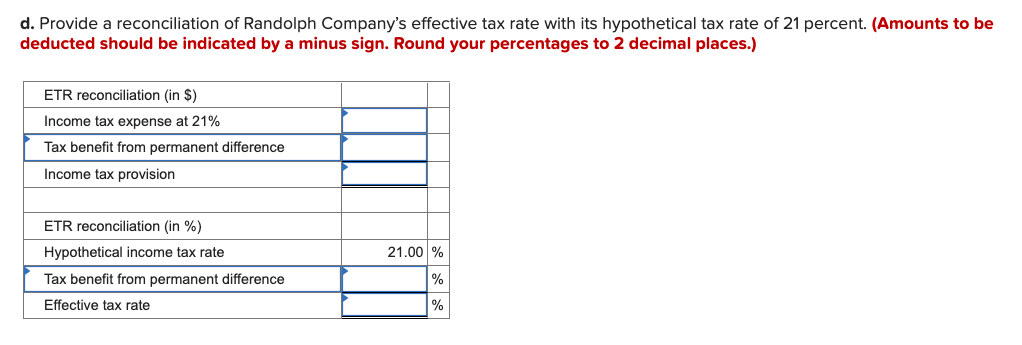

- Book income of $1,900,000 Included in the computation were favorable temporary differences of $230,000, unfavorable temporary differences of $226,000 and favorable permanent differences of $168,000. What is the company's deferred income tax expense or benefit?arrow_forwardHafnaoui Company reported pretax net income from continuing operations of $912,000 and taxable income of $587,500. The book–tax difference of $352,500 was due to a $235,000 favorable temporary difference relating to depreciation, an unfavorable temporary difference of $94,000 due to an increase in the reserve for bad debts, and a $211,500 favorable permanent difference from the receipt of life insurance proceeds. At the end of the year, the reserve for bad debts had a balance of $117,500; the beginning balance in the account was $23,500. Hafnaoui's beginning book (tax) basis in its fixed assets was $1,014,000 ($821,000) and its ending book (tax) basis is $1,535,000 ($1,107,000). a. Compute Hafnaoui Company's current income tax expense. b. Compute Hafnaoui Company's deferred income tax expense or benefit. c. Compute Hafnaoui Company's effective tax rate. d. Provide a reconciliation of Hafnaoui Company's effective tax rate with its hypothetical tax rate of 21 percent.arrow_forwardDEF Co. reported taxable income of P8M in its income tax return for the 1st year of operations. The entity revealed the following temporary differences between financial income and taxable income for the year:Tax depreciation in excess of book depreciation, P800,000Accrual for product liability claim in excess of actual claim, P1,200,000Reported installment sales income in excess of taxable installment sales income, P2,600,000Income tax rate, 30%Compute for the deferred tax expense for the 1st yeararrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education