Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

thumb_up100%

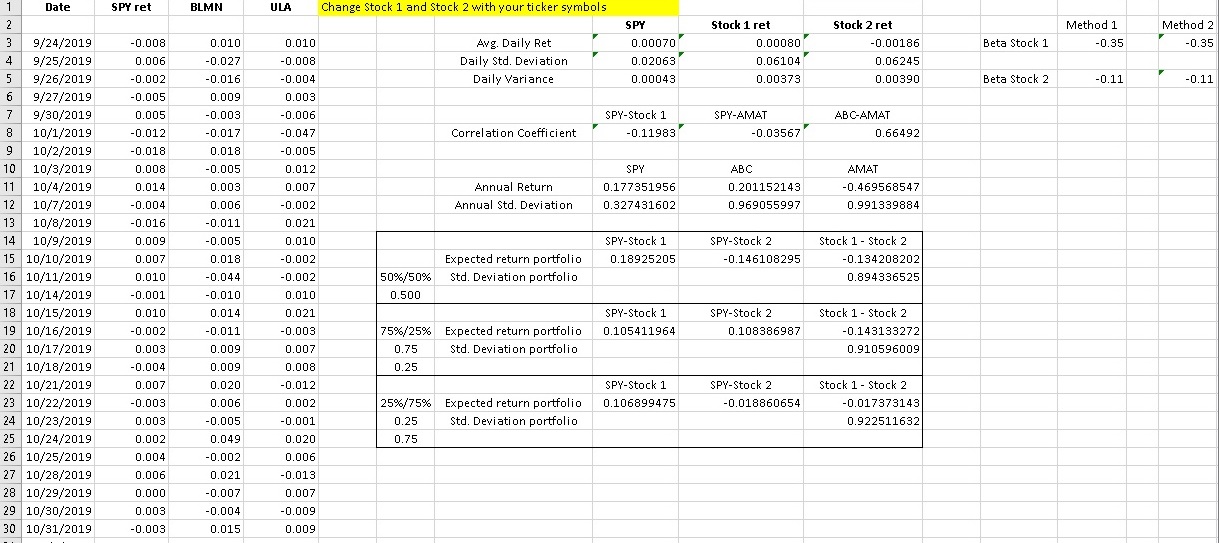

What are the the key concepts (e.g., the standard deviation of the portfolio is less than the weighted average of the standard deviations of the stocks in the portfolio)

Expert Solution

arrow_forward

Step 1

The question is based on the explanation of key concept behind creating a portfolio with different combinations of stocks.

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The risk associated with the overall market is referred to as _____ risk. a. unsystematic b. diversified c. portfolio d. systematicarrow_forwardAccording to modern financial theory, the correct measure of risk is O Idiosyncratic Risk Variance Beta Standard Deviation Volatilityarrow_forwardHow is the standard deviation of returns calculated?arrow_forward

- Assume I am holding a portfolio of two risky assets with standard deviations of 1. Assume also that I am holding the minimum variance portfolio of these two assets. I do not know the correlation of these assets but I do know that it's not equal to one. Which of the below statements is true based on the information above? O Portfolio's standard deviation is equal to 1/2. Portfolio's return is equal to 1/2. O Portfolio weights of the two assets are equal to 1/2. None of the above statements is true. Portfolio's Sharpe ratio is equal to 1/2.arrow_forwardWhen comparing investments that have different means, the measures the relative riskiness of each investment and is a better indicator of risk than the standard deviation.arrow_forwardPortfolio Beta is the average of the Betas of the investments included in the portfolio.arrow_forward

- Which of the following stocks have the highest systematic risk? A. A stock with a high correlation to the market and a low return volatility. B. A stock with a low correlation to the market and a high return volatility. C. A stock with a high correlation to the market and high return volatility. D. A stock with a low correlation to the market and a low return volatility.arrow_forwardIs the portfolio risk the weighted average of the variance or covariance?arrow_forwardAccording to modern portfolio theory, pair-wise covariance is more important to total portfolio risk than individual security variance. True or Falsearrow_forward

- How does standard deviation and variance affect portfolio risk, more so than expected return?arrow_forwardThe Capital Asset Pricing Model (CAPM) describes a relationship between the expected return of,,, a)An individual share and its variance risk b)An individual share and its standard deviation risk c)An individual share and its undiversifiable risk d)An individual share and its diversifiable riskarrow_forwardInvestors can use certain metrics to assess a stock or stock portfolio's risk. One of them is the Sortino ratio. What is this ratio and what is unique in its measurement?arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education