Essentials Of Investments

11th Edition

ISBN: 9781260013924

Author: Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher: Mcgraw-hill Education,

expand_more

expand_more

format_list_bulleted

Related questions

Question

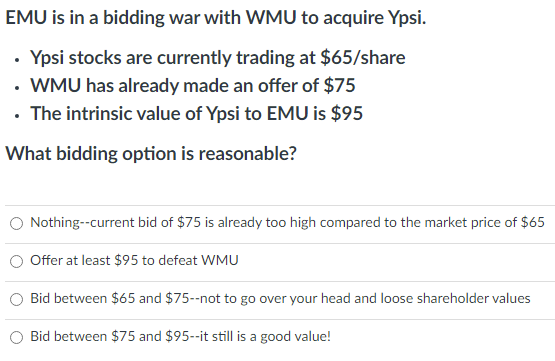

Transcribed Image Text:EMU is in a bidding war with WMU to acquire Ypsi.

Ypsi stocks are currently trading at $65/share

• WMU has already made an offer of $75

• The intrinsic value of Ypsi to EMU is $95

What bidding option is reasonable?

Nothing--current bid of $75 is already too high compared to the market price of $65

Offer at least $95 to defeat WMU

Bid between $65 and $75--not to go over your head and loose shareholder values

Bid between $75 and $95--it still is a good value!

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- The current market price for common shares of Getgo Company is $15. Put options on these shares currently trade at 0.75 and come with a $10 strike price. If the stock’s market price falls to $8.45 what would be the dollar return earned on these put options? Your answer should look like this 1.2 that is not the right answerarrow_forwardKT corporation has announced plans to acquire MJ corporation. KT is trading for $45 per share and MJ is trading for $25 per share, with a premerger value for MJ of $3 billion dollars. If the projected synergies from the merger are $750 million, what is the maximum exchange ratio that KT could offer in a stock swap and still generate a positive NPV? It is closest to: Answer choices: A) 0.75 B) 3.30 C) 2.25 D) 1.30arrow_forwardA speculator can choose between (i) buying 108 shares of a stock for $50.58 per share, and (ii) buying 1080 European call options on that stock with a strike price of $42 for $3.99 per option. At maturity, what is the stock price that would make the two alternatives equally profitable? a. 1.58 O b. 42.81 O c. 47.57 d. 45.96 e. 14.18arrow_forward

- Honeywell does not pay a dividend and its stock has a volatility of 28% and a current stock price of $67 per share. The risk-free interest is 4%. Determine the Black-Scholes value of a one-year, at-the-money call option on Honeywell's stock. (You must show me how you do this without an Excel-based option pricing model. That is, you must show your work with the formulas and Z-Tables. The value will likely be different than if you just plug into an Excel-based BSOPM). The call option's value is $. (Round to the nearest cent.)arrow_forward5 Construct payoff tables or payoff diagrams on expiration to show what position in IBM puts, calls and/or underlying stock best expresses the investor's objectives described below. Assume IBM currently sells for $100. Make appropriate assumptions about the strike prices of options in each case. Ignore the cost of options. a/ An investor wants the position to be at least worth $75. Further the investor believes that the IBM stock price will go up but will at most reach $140.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

- Essentials Of InvestmentsFinanceISBN:9781260013924Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.Publisher:Mcgraw-hill Education,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson,

Foundations Of FinanceFinanceISBN:9780134897264Author:KEOWN, Arthur J., Martin, John D., PETTY, J. WilliamPublisher:Pearson, Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning

Fundamentals of Financial Management (MindTap Cou...FinanceISBN:9781337395250Author:Eugene F. Brigham, Joel F. HoustonPublisher:Cengage Learning Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Corporate Finance (The Mcgraw-hill/Irwin Series i...FinanceISBN:9780077861759Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan ProfessorPublisher:McGraw-Hill Education

Essentials Of Investments

Finance

ISBN:9781260013924

Author:Bodie, Zvi, Kane, Alex, MARCUS, Alan J.

Publisher:Mcgraw-hill Education,

Foundations Of Finance

Finance

ISBN:9780134897264

Author:KEOWN, Arthur J., Martin, John D., PETTY, J. William

Publisher:Pearson,

Fundamentals of Financial Management (MindTap Cou...

Finance

ISBN:9781337395250

Author:Eugene F. Brigham, Joel F. Houston

Publisher:Cengage Learning

Corporate Finance (The Mcgraw-hill/Irwin Series i...

Finance

ISBN:9780077861759

Author:Stephen A. Ross Franco Modigliani Professor of Financial Economics Professor, Randolph W Westerfield Robert R. Dockson Deans Chair in Bus. Admin., Jeffrey Jaffe, Bradford D Jordan Professor

Publisher:McGraw-Hill Education