ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

|

(Figure:

|

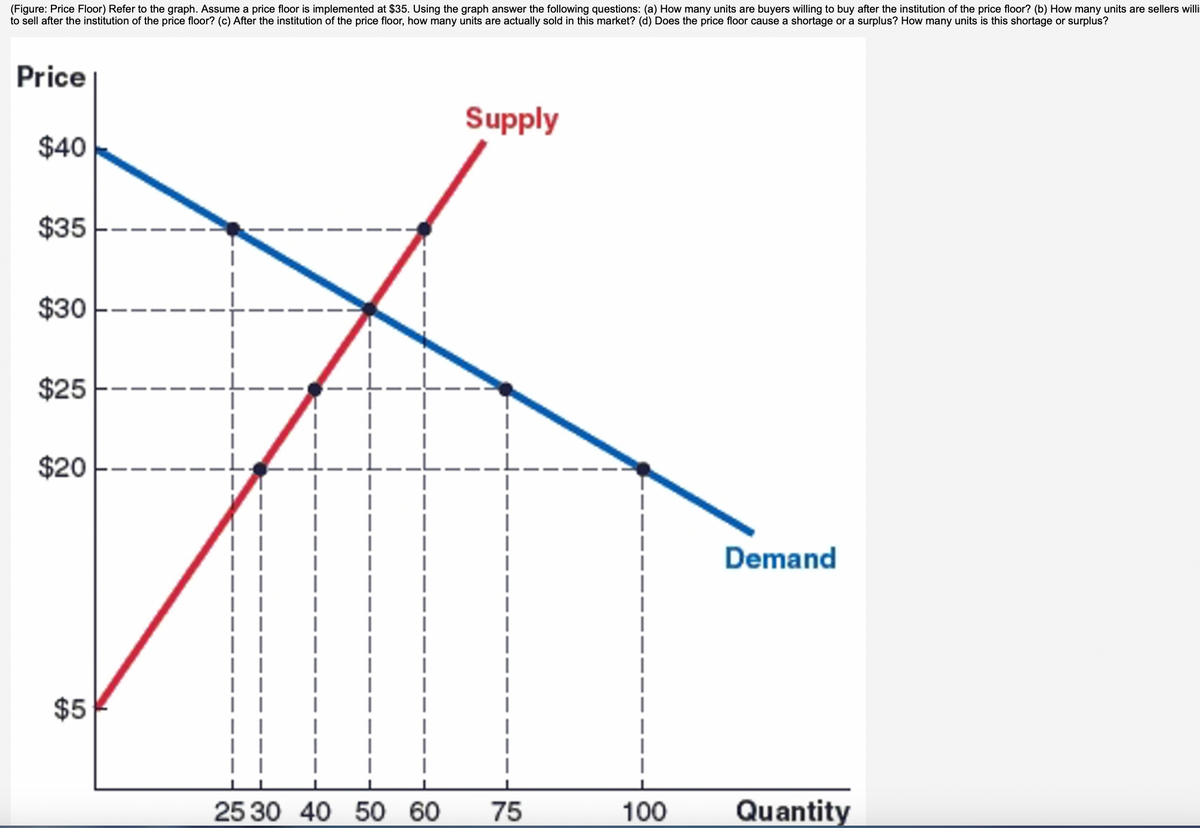

Transcribed Image Text:(Figure: Price Floor) Refer to the graph. Assume a price floor is implemented at $35. Using the graph answer the following questions: (a) How many units are buyers willing to buy after the institution of the price floor? (b) How many units are sellers willi

to sell after the institution of the price floor? (c) After the institution of the price floor, how many units are actually sold in this market? (d) Does the price floor cause a shortage or a surplus? How many units is this shortage or surplus?

Price

$40

$35

$30

$25

$20

$5

|

I

I

Supply

25 30 40 50 60 75

Demand

100 Quantity

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

This is a popular solution

Trending nowThis is a popular solution!

Step by stepSolved in 2 steps

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Question 12 Cecilia usually bought several pairs of designer shoes each year, but she lost her job this year. Which graph below shows what happens to her demand for designer shoes? P₁ Price Price P₂ P₁ D₂ Q₂ I I Q2 D₁ Q₁ S Q₁ Quantity Quantityarrow_forward10. Market equilibrium The following table shows the monthly demand and supply in the market for shoes in San Francisco. Price Quantity Demanded Quantity Supplied (Dollars per pair of shoes) (Pairs of shoes) (Pairs of shoes) 20 1,650 300 40 1,200 750 60 600 1,050 80 300 1,350 100 150 1,500 On the following graph, plot the demand for shoes using the blue point (circle symbol). Next, plot the supply of shoes using the orange point (square symbol). Finally, use the black point (plus symbol) to indicate the equilibrium price and quantity in the market for shoes. Note: Plot your points in the order in which you would like them connected. Line segments will connect the points automatically. 120 100 Demand 80 Supply 60 Equilibrium 40 20 300 600 900 1200 1500 1800 QUANTITY (Pairs of shoes) PRICE (Dollars per pair of shoes)arrow_forwardPRICE (Dollars per gallon) Price (Dollars per gallon) 10 12 11 a 10 0 8 D 6 a 4 2 Use the data in the preceding table to plot the demand and supply curves for milk on the following graph. Use the blue points (circle symbol) to plot the demand curve. Then use the orange points (square symbol) to plot the supply curve. Line segments will automatically connect the points. ? 100 The equilibrium market price is $ The new quantity supplied is Quantity Demanded (Millions of gallons) 100 of 200 300 400 200 300 400 QUANTITY (Millions of gallons) 500 The new quantity supplied is of Quantity Supplied (Millions of gallons) 500 500 400 600 Suppose the government enacts a milk price support of $7.00 per gallon. 300 200 100 -O Demand Use the green line (triangle symbol) to plot the new price line on the preceding graph. ***]* Supply Government Price 1 Government Price 2 and the equilibrium quantity is Suppose now that the government decides to set a price ceiling of $4.00 per gallon. Use the purple…arrow_forward

- How would [1] a decrease in the price of flour and [2] an improvement in technology of pizza making would affect the market price and quantity of pizza, other things remaining constant? The price of pizza would drop and the equilibrium quantity would rise. The price of pizza would drop but the impact on the equilibrium quantity is uncertain. The equilibrium quantity of pizza would rise but the impact on price is uncertain. Both the price as well as the equilibrium quantity of pizza would rise.arrow_forwardthe combination of generous stimulus payments and the extremely successful Covid vaccination campaign should lead to a significant increase in the number of drivers getting back on the road. Using a graph, depict and explain the impact of the change. Which of the curve(s), if any, would shift, and why? Graphically indicate the new equilibrium, labeling it as P2 and Q2. What has happened to price? What has happened to quantity?arrow_forwardTable 4-16 The following table shows the supply and demand schedules in a market. |Quantity Supplied (units) |Quantity Demanded (units) 50 40 30 20 10 Price (S) 15 30 45 60 75 14 6 10 1. Refer to Table 4-16. Draw the supply & demand curves. 2. Refer to Table 4-16. What is the equilibrium price in this market? 3. Refer to Table 4-16. What is the equilibrium quantity in this market? 4. Refer to Table 4-16. At a price of $2, will there be a surplus or shortage of units in this market? 5. Refer to Table 4-16. At a price of $8, how large of a surplus will there be in this market? 6. Refer to Table 4-16. If the supply curve shifts to the right, will the price in this market rise or fall?arrow_forward

- Price (dollars per pound) 6. 1o Quantity (millions of pounds per day) 14 The graph illustrates the market for British pounds, the currency of the United Kingdom. As the number of buyers of pounds decreases and the number of sellers of pounds increases, the equilibrium price of a pound A) will remain the same. B) will fall. C) will rie. D) might rise, fall, or remain the same but more information is needed. will rise if the magnitude of the effect on the buyers is larger than the E) magnitude of the effect on the sellers.arrow_forward21. Supply: Basic concepts Complete the following table by selecting the term that matches each definition. Quantity Supplied Supply Curve Supply Schedule Law of Definition Supply The amount of a good that sellers are willing and able to supply at a given price The claim that, other things being equal, the quantity supplied of a good increases when the price of that good rises A graphical object showing the relationship between the price of a good and the amount that sellers are willing and able to supply at various prices A table showing the relationship between the price of a good and the amount of it that sellers are willing and able to supply at various prices Apply your understanding of the previous key terms by completing the following scenario with the appropriate terminology. Your coworker Musashi is really concerned about a project that he has just been assigned. He is in charge of analyzing and determining conditions in the market for televisions from an extensive sales…arrow_forwardNote:- Do not provide handwritten solution. Maintain accuracy and quality in your answer. Take care of plagiarism. Answer completely. You will get up vote for sure.arrow_forward

- 10. Market equilibrium The following table presents the annual demand and supply in the market for boots in Chicago. Price (Dollars per pair of boots) 20 40 60 80 100 of boots) 120 Quantity Demanded (Pairs of boots) 2,200 1,600 1,200 800 400 100 Quantity Supplied (Pairs of boots) 400 On the following graph, plot the demand for boots using the blue point (circle symbol). Next, plot the supply of boots using the orange point (square symbol), Finally, use the black point (plus symbol) to indicate the equilibrium price and quantity in the market for boots. Note: Plot your points in the order in which you would like them connected, Line segments will connect the points automatically. 1,000 1,800 2,000 2,400 Demand 9 0arrow_forwardA publisher has established the supply equation of one of their textbooks to be p =q² and is show in blue on the graph. They also found the demand equation to be p = -9² +20 and is shown in red. Where p is in tens of dollars and q is the quantity in hundreds of textbooks. 20 Find the equilibrium price. $ p Find the equilibrium quantity. 16- Find the amount demanded when the price is $1800. 12- Find the amount supplied when the price is $20. Quantity 12arrow_forward13. Suppose over the next several years the level of income and wealth rises in the state of Florida. For the housing market this would mean: An increase in the quantity of houses demanded, rising prices and an increase in supply. An increase in the demand for houses, rising prices and an increase in quantity supplied. An increase in the quantity of houses demanded shortages and higher prices. A decrease in the quantity of houses supplied as demand increases. Price gouging in this market would be rampant.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education