ENGR.ECONOMIC ANALYSIS

14th Edition

ISBN: 9780190931919

Author: NEWNAN

Publisher: Oxford University Press

expand_more

expand_more

format_list_bulleted

Related questions

Question

Transcribed Image Text:-----

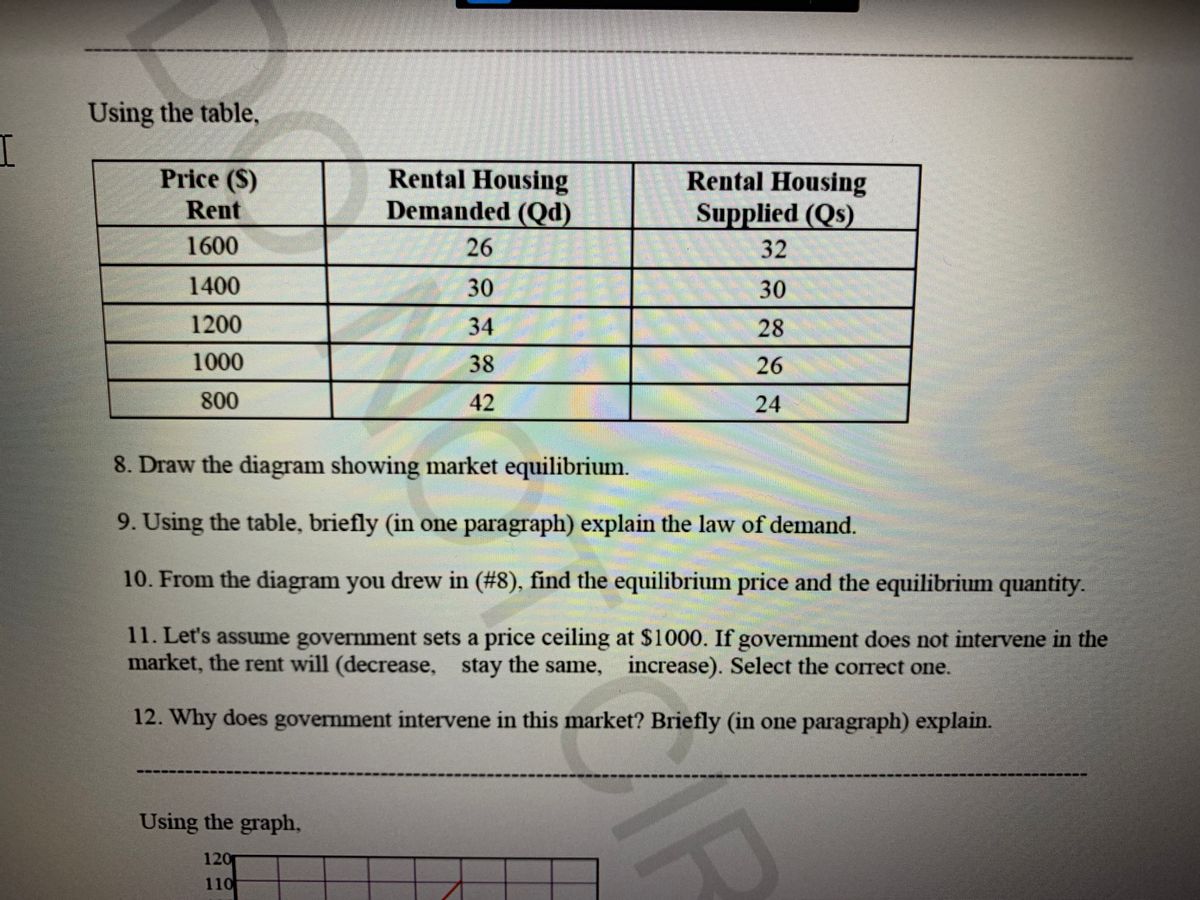

Using the table.,

Price (S)

Rent

Rental Housing

Demanded (Qd)

L26

Rental Housing

Supplied (Qs)

32

1600

1400

30

30

1200

34

28

1000

38

26

800

42

24

8. Draw the diagram showing market equilibrium.

9. Using the table, briefly (in one paragraph) explain the law of demand.

10. From the diagram you drew in (#8), find the equilibrium price and the equilibrium quantity.

11. Let's assume government sets a price ceiling at $1000. If government does not intervene in the

market, the rent will (decrease, stay the same, increase). Select the correct one.

12. Why does government intervene in this market? Briefly (in one paragraph) explain.

Using the graph,

120

110

Expert Solution

This question has been solved!

Explore an expertly crafted, step-by-step solution for a thorough understanding of key concepts.

Step by stepSolved in 4 steps with 1 images

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Use the accompanying graph to answer these questions. 20 S sº Price of X ($) 18 16 14 12 10 8 6 4 2 0 1 2 3 4 Quantity of Good X units 5 6 D a. Suppose demand is D and supply is SO. If a price ceiling of $6 is imposed, what are the resulting shortage and full economic price? Shortage: Full economic price: $ b. Suppose demand is D and supply is SO. If a price floor of $12 is imposed, what is the resulting surplus? What is the cost to the government of purchasing any and all unsold units? Surplus: Cost to government: $ c. Suppose demand is D and supply is so so that equilibrium price is $10. If an excise tax of $6 is imposed on this product, what happens to the equilibrium price paid by consumers? The price received by producers? The number of units sold? Fauilibrium price paid by consumers $1arrow_forwardPRICE (Dollars per gallon) Price (Dollars per gallon) 10 12 11 a 10 0 8 D 6 a 4 2 Use the data in the preceding table to plot the demand and supply curves for milk on the following graph. Use the blue points (circle symbol) to plot the demand curve. Then use the orange points (square symbol) to plot the supply curve. Line segments will automatically connect the points. ? 100 The equilibrium market price is $ The new quantity supplied is Quantity Demanded (Millions of gallons) 100 of 200 300 400 200 300 400 QUANTITY (Millions of gallons) 500 The new quantity supplied is of Quantity Supplied (Millions of gallons) 500 500 400 600 Suppose the government enacts a milk price support of $7.00 per gallon. 300 200 100 -O Demand Use the green line (triangle symbol) to plot the new price line on the preceding graph. ***]* Supply Government Price 1 Government Price 2 and the equilibrium quantity is Suppose now that the government decides to set a price ceiling of $4.00 per gallon. Use the purple…arrow_forwardDemand Schedule Supply ScheduleP Q P Q10 30 10 809 35 9 748 40 8 687 45 7 626 50 6 565 55 5 504 60 4 443 65 3 382 70 2 321 75 1 261. Graph the demand and supply schedules (above). What are the (approximate) Price and Quantity in this market?arrow_forward

- In an effort to increase the amount of housing development in Los Angeles a new zoning ordinance has passed that allows homeowners to add small dwelling units to their existing residential lots. Explain what the expected result will be in terms of the market supply and demand for housing and the change in the market equilibrium. Provide graphs to illustrate this change.arrow_forwardG.237.arrow_forwardAbove is the supply and demand graph in a market. Answer the following questions based on the graph: 3.1. What are the equilibrium price and quantity in the market? 3.2. What are the quantity supplied, quantity demanded, and price at a shortage of 400 units? 3.3. Whar are the quantity supplied, quantity demanded, and price at a surplus of 200 units?arrow_forward

- Problem 4. From number 2, draw another graph and call equilibrium Point A. Illustrate on the graph what will happen to the Supply curve when producers enter the market? Does the question refer to an increase, need help understanding the question.arrow_forwardI need part E answered only, but please answer it from what the graphs gives only and not from any outside source. Someone already answered this but they used a different graph and not the one given in the picture. So please answer it accordingly with the given graph, thank you in advancedarrow_forwardIdentify the scenario which corresponds to the graph of a given market below: $10 $9 $8 $7 $6 $5 $4 $3 $2 $1 $- 20 40 60 80 100 120 140 160 Quantity The graph represents a decrease in supply and a decrease in equilibrium price and quantity. The graph represents a decrease in demand and a decrease in equilibrium price and quantity. The graph represents a decrease in equilibrium quantity demanded because of a price increase. The graph represents an increase in demand and a decrease in equilibrium price and quantity. Pricearrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON

Principles of Economics (12th Edition)EconomicsISBN:9780134078779Author:Karl E. Case, Ray C. Fair, Sharon E. OsterPublisher:PEARSON Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON

Engineering Economy (17th Edition)EconomicsISBN:9780134870069Author:William G. Sullivan, Elin M. Wicks, C. Patrick KoellingPublisher:PEARSON Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning

Principles of Economics (MindTap Course List)EconomicsISBN:9781305585126Author:N. Gregory MankiwPublisher:Cengage Learning Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Managerial Economics & Business Strategy (Mcgraw-...EconomicsISBN:9781259290619Author:Michael Baye, Jeff PrincePublisher:McGraw-Hill Education

Principles of Economics (12th Edition)

Economics

ISBN:9780134078779

Author:Karl E. Case, Ray C. Fair, Sharon E. Oster

Publisher:PEARSON

Engineering Economy (17th Edition)

Economics

ISBN:9780134870069

Author:William G. Sullivan, Elin M. Wicks, C. Patrick Koelling

Publisher:PEARSON

Principles of Economics (MindTap Course List)

Economics

ISBN:9781305585126

Author:N. Gregory Mankiw

Publisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Managerial Economics & Business Strategy (Mcgraw-...

Economics

ISBN:9781259290619

Author:Michael Baye, Jeff Prince

Publisher:McGraw-Hill Education